Buyback announcements have taken a breather amid the AI arms race and increasing equity issuance

Capital market trends point to possibly smaller net buyback yields in the quarters to come, prompting asset allocators to rethink strategy

Record-breaking IPOs and ambitious tech capex plans put the onus on the corporate world to absorb new equity hitting the market

Equity issuance is all the rage. The SpaceX () IPO on Friday, Alphabet’s () up-sized secondary announced last week, and a slew of other major go-public names over the remainder of 2026 (Anthropic, OpenAI) buck the years-long trend of intense buybacks and shareholder-friendly activities by the world’s most valuable companies.

Before 2022’s rate rise, the standard C-suite procedure was to simply issue debt at very low interest rates, invest some in moderate-ROI projects, then repurchase a boatload of common shares. Chastised by some politicians, the strategy made sense.

Recall Corporate Finance 101 class: increasing debt percentage in a firm’s capital structure effectively reduces the weighted-average cost of capital (as it crowds out higher-cost equity financing). The cherry on top was the positive signaling mechanism to investors and the street.

The Profit Boom Masks a Cash Flow Shift

All that was in the ZIRP era and pre-AI. Today, multinational corporations print profits like never before. The is set to grow non-GAAP EPS by more than 20% in 2026, according to FactSet data. Per-share earnings also scale new heights on the global stage, with both current- and out-year bottom line estimates soaring to records.

But not all profit indicators appear so pristine. Tech free cash flow (often viewed as a more reliable equity valuation metric) has declined, particularly among the AI hyperscalers. Sticking with the classroom theme, FCF is operating cash flow minus capex. Indeed, companies like Alphabet and NVIDIA () invest heavily in what they consider to be extremely profitable AI-related endeavors.

Such projects don’t come cheap. They also require immediate cash. Operating cash flow is being directed toward them, and buybacks may be the biggest victim.

AI Is Winning the Capital Allocation Battle

To be clear, share repurchases are not in freefall. In fact, as J.P. Morgan Asset Management’s David Kelly penned this week, absolute buyback value ticked to a record level in 2026. Growth slowed, though, while tech hyperscaler repurchase activity is down 64% YoY, per Kelly.

As a share of market cap, however, buybacks have slimmed. Bank of America Global Research noted that the aggregate amount of S&P 500 buybacks as a percentage of market cap slid to its lowest level since late 2023 in the most recent week. Tech is the primary culprit, while repurchases picked up in non-growth sectors such as Financials and Energy.

Big picture: capital is increasingly directed toward capex, R&D, and M&A, while dividend growth is steady, at least away from cyclical sectors.

Peak Buybacks?

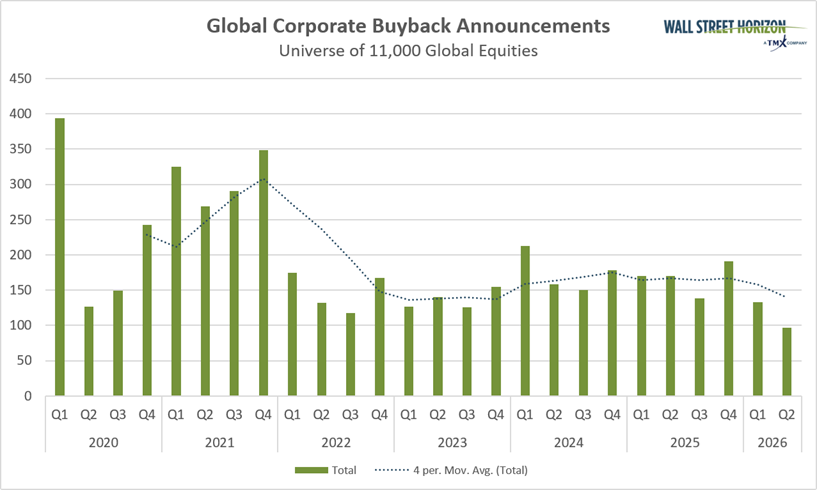

What does Wall Street Horizon’s data reveal? Share repurchase announcements might have put in their high. Total corporate buyback disclosures, spanning more than 11,000 global firms, are close to the weakest nominal amount since we began tracking data pre-pandemic. And that’s arguably a low bar, considering the Great Bond Bear Market of 2022 and the related financing scare.

The chart below illustrates how late 2020 through 2021 was (in retrospect) the golden age of buybacks, given extremely low borrowing costs. Companies that didn’t lock in cheap, long-term debt missed what could end up being a multi-generational opportunity.

Global Buyback Announcements Dip Toward a Multi-Year Low

Source: Wall Street Horizon

Then, after Treasury rates surged, ChatGPT hit the scene in November 2022. NVIDIA’s blowout Q1 (reported in May 2023) marked the dawn of the AI-capex era. Now, amid the AI arms race and optimism about growth projections, CEOs and CFOs are less wont to announce hefty buybacks.

A New Market Test Emerges

But what does it mean for portfolio managers and traders? Well, it’s all about market reactions to both slimmer share repurchase events and debt-issuance announcements.

For now, it’s party on, Garth. GOOGL hardly budged when its $80 billion-plus debt-offering news hit the tape. We’ll be on the lookout for steeper stock-price drops in the months ahead. Capital markets have a way of checking companies; look no further than Oracle’s (ORCL) credit default swap pricing last fall.

The Opportunity in ‘Buyback Scarcity’

Buyback scarcity has another, potentially more bullish, impact.

Consider companies that remain capital disciplined and keep churning out hefty free cash flow. They could stand out among their higher-capex peers by hiking repurchase facilities. Investors focused on the total shareholder yield factor (buyback yield plus dividend yield) may allocate capital accordingly.

As it stands, the Invesco BuyBack Achievers ETF () lags the S&P 500 ETF () by more than six percentage points on the year.

Will Corporate America Still Be the Buyer?

As more equity supply comes on the market through secondaries and IPOs in 2026, it’s a question mark whether the rest of the corporate world will be there as a major buyer, as they have in past cycles. The buyback bid could be in jeopardy.

We think that may be an emerging earnings-season story in upcoming quarters.

The Bottom Line

Companies are announcing fewer buyback plans, while the total value of share repurchases has dropped to a multi-year low on a relative basis. Tech and the AI theme clearly drive executives to ramp up capex spending at the expense of (at least partially) stock buybacks. It’s a risk-on sign, putting even more pressure on AI projects to deliver big profits.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.