Dave & Buster’s Entertainment, Inc. PLAY used its first-quarter fiscal 2026 call to acknowledge a weak start while arguing that the bigger story is a business reset built around games, value, food and beverage, and remodels.

Management’s message was clear: Q1 disappointed, but the company believes the pieces are now in place to improve same-store sales through the rest of fiscal 2026 and deliver more than $100 million in free cash flow.

PLAY Confronts a Soft Quarter

CEO Tarun Lal said first-quarter results came in below both internal expectations and the outlook management had set previously. He pointed to a softer macro backdrop in April, including pressure on consumer sentiment, but also said the company was not using that as an excuse.

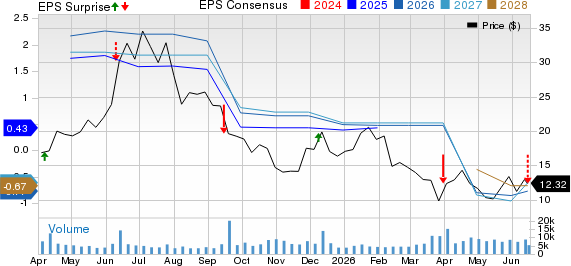

The reported numbers were weak enough to keep the pressure on management. Adjusted earnings per share came in at $0.22, below the Zacks Consensus Estimate of $0.37, resulting in a negative earnings surprise of 40.5%. Revenues of $559.2 million missed the Zacks Consensus Estimate of $571.1 million by 2.1%.

Dave & Buster’s Entertainment, Inc. Price, Consensus and EPS Surprise

Dave & Buster’s Entertainment, Inc. price-consensus-eps-surprise-chart | Dave & Buster’s Entertainment, Inc. Quote

Comparable store sales fell 5.4% in the first quarter, revenues declined 1.5% year over year, and adjusted EBITDA slipped to $123.2 million from $136.1 million a year earlier. Adjusted EBITDA margin also narrowed to 22% from 24%.

Dave & Buster’s Reworks Its Value Message

Lal said one of the clearest lessons from the quarter was that the company’s dollar-per-day messaging did not resonate as expected. He said the company has since pivoted to promotions that are proving more compelling with customers.

Management described the marketing reset as broader than a single campaign. Lal said Dave & Buster’s is simplifying its promotional calendar, leaning more heavily on data-driven media mix decisions, and trying to strike a better balance between television and digital rather than swinging too far in either direction.

In Q&A, a BMO Capital Markets analyst pressed for more detail on what changed. Lal stated that the current message hierarchy is more disciplined, with 10 new games now serving as the primary message and the World Cup watch experience as a secondary one.

PLAY Sees Traction in Food and Games

While entertainment remained soft, management highlighted food and beverage as an early proof point. Lal said comparable food and beverage sales rose about 5% in Q1, extending a run of nine straight months of positive same-store sales in that part of the business.

Lal credited the return to a historically proven menu and stronger execution of the Eat & Play Combo. CFO Darin Harper added that attach trends have improved, helping the company target value-conscious guests without overdiscounting the broader business.

Games are the bigger strategic swing. Lal said the company rolled out 10 new games, the most since 2017, and expects at least five more over the rest of fiscal 2026. He framed that as a direct response to guest feedback that the arcade floor had lacked enough newness.

Dave & Buster’s Pins Hopes on Traffic Drivers

Management repeatedly returned to the idea that new games are meant to drive visits first and spending second. In response to a Texas Capital Securities analyst, Harper said the refresh should be viewed mainly as a way to restore relevance, reengage lapsed guests, and support traffic rather than simply lift in-store game spend.

Lal also tied the second-half outlook to still-unannounced intellectual property partnerships, saying those deals should help put the brand back into consumer conversation. That confidence sounded firmer in Q&A than in the prepared remarks.

The World Cup is another near-term catalyst. Management said the company launched a full activation around watch parties, themed food and drinks, soccer-inspired games, and promotional ticket giveaways tied to marquee matches.

PLAY Stays Focused on Cash and Capex

Despite the weak quarter, Harper said the company generated $25.3 million of adjusted free cash flow compared with a negative $58.8 million a year earlier. Available liquidity ended the quarter at $499.1 million.

Management is pairing that cash focus with stricter capital discipline. Lal reiterated that net capital expenditures should not exceed $200 million in fiscal 2026, down from about $270 million in fiscal 2025, while free cash flow should still top $100 million this year.

The call also made clear that capital allocation is shifting. Lal and Harper said the core store base now takes priority, with remodels, deleveraging and shareholder returns all competing for dollars that might otherwise have gone to faster unit growth.

Dave & Buster’s Narrows Its Priorities

Prepared remarks and Q&A both pointed to a tighter operating playbook. Management emphasized speed of service, more disciplined marketing, better value architecture, and a remodel program that costs about half as much as prior versions while still producing about a 7% comp uplift.

Harper said six remodels have already been completed, with two more expected in fiscal 2026. He also said the company could open about half as many new units in fiscal 2027 as it refocuses spending on the existing base.

Coming out of the call, management’s stance was not celebratory. It was more a case that the quarter exposed what was not working, and that the company now wants investors to judge it on execution against a narrower set of priorities over the balance of the year.

Zacks Signals on PLAY

PLAY carries a Zacks Rank #4 (Sell), alongside Value Score A, Growth Score B, Momentum Score A and VGM Score A. Zacks says a Style Score is meant to complement, not override, the Zacks Rank, with the rank remaining the first screen because earnings estimate revisions are the most important driver in the system.

That leaves PLAY with a mixed signal. The style profile points to favorable value, growth and momentum characteristics, but Zacks’ framework says investors should not buy stocks rated Zacks Rank #4 or 5 (Strong Sell) even when each Style Score is strong. That ranking can still change as estimate revisions move following the latest results.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Dave & Buster’s Entertainment, Inc. (PLAY) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.