The Nasdaq’s Battle Cry

The Nasdaq market stood its ground this week, firmly supported by the bulls at the 21-day moving average, carrying the torch through Thursday morning. The march of 2024 displays a rhythm preventing overheating, with periodic pullbacks for respite.

The Tempered Tech Bubble

In the midst of murmurs surrounding a tech bubble and AI enthusiasm, some tech stocks have faced recent turmoil while others struggle to recover from setbacks in 2022. Savvy investors may see this as an opportunity to seize impressive tech stocks at a bargain, especially as market leaders like Nvidia hit overbought territory in the short term.

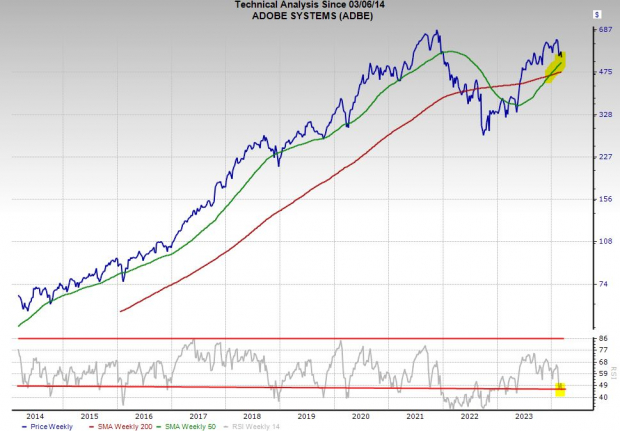

Adobe: Unveiling the Canvas

Adobe stands almost 20% shy of its peak ahead of the Q1 FY24 earnings release on March 14. Concerns linger over its slowing revenue growth and competitive strategy in an era where platforms like OpenAI empower users with creative tools even without prior expertise. Disappointment arose following regulatory obstacles that scuttled Adobe’s Figma acquisition plans.

Apple: Orchestrating Innovation

Apple’s stock has dipped 12% year-to-date, paling against the Tech sector’s ascent and Nvidia’s stellar 85% surge, settling 15% below mid-December’s zenith. Worries loom over decelerating growth in China and geopolitical tensions, alongside concerns about Apple trailing in AI adoption.

Block Inc.: Cracking the Code

Formerly Square, Block slumbers over 70% beneath its pinnacle, mirroring a meandering course over the past year against Tech’s uptrend. Trading near early 2020 levels, pre-Covid rollercoaster, Wall Street abandoned this tech luminary amidst escalating interest rates, stalling consumer outlays, fierce market competition, and a mistimed acquisition.

The Rollercoaster Ride of Block, Inc.: A Deep Dive Analysis

A Costly Gamble on Afterpay

Block’s acquisition of the buy now pay later firm Afterpay raised eyebrows as it occurred during the pinnacle of tech valuations. Critics argue that Block overpaid for the firm, leading to questions about the wisdom of the move. Compounded with this risky acquisition, Block faced the repercussions of its sudden Covid-induced meteoric rise. Sales surged by a staggering 86% in 2021 and 102% in 2020, catapulting from $4.7 billion in FY19 to $17.66 billion in 2021, a stark contrast from its pre-Covid growth rate of approximately 40%.

Resilience Amidst Chaos

Despite facing challenges brought on by the turbulent market, Block has managed to retain its standing as a futuristic digital banking and financial services entity for both consumers and businesses. In 2023, Block recorded a 25% revenue growth following a period of relatively stagnant sales in 2022. Projections suggest a 13% revenue expansion in FY24 and a further 12% increase in 2025. Moreover, its adjusted earnings are forecasted to spike by 64% this year and an additional 31% in the subsequent year.

A Bright Spot in the Forecast

Block’s positive EPS revisions have positioned the company as a Zacks Rank #1 (Strong Buy) currently. Impressively, out of the 40 brokerage recommendations from Zacks, 29 are categorized as “Strong Buys,” with only one listed as a “Strong Sell.” As Block navigates the market landscape, its stock’s PEG ratio, a metric incorporating long-term growth prospects, stands at 2.2 compared to the Tech sector’s 1.9 and its own one-year highs exceeding 200. Notably, Block’s current trading position represents a 60% discount to the Tech sector at 1.9X forward 12-month sales and sits 84% below its peak valuations.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.