Alibaba Group BABA closed its fiscal 2026 with a sobering message for investors — the cost of staying relevant in the artificial intelligence (AI) era is steep, and shareholders are footing the bill. The Chinese Internet major reported its fourth-quarter and full-year results on May 13, 2026, revealing that non-GAAP net income for the March quarter collapsed to RMB 86 million from RMB 29,847 million a year earlier, while the company swung to its first operating loss since 2021. Quick commerce subsidies and a relentless AI capital-spending cycle have hollowed out near-term profitability.

With management explicitly signaling that the heavy spending cycle will continue, the case for selling the stock is hard to ignore as 2026 progresses. The Zacks Consensus Estimate for fiscal 2027 earnings is pegged at $7.46 per share, down by 4.2% over the past 30 days.

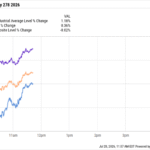

Alibaba Group Holding Limited Price and Consensus

Alibaba Group Holding Limited price-consensus-chart | Alibaba Group Holding Limited Quote

Profit Collapse Exposes the Real Cost of Alibaba’s AI Pivot

The headline numbers from the March quarter make the strain visible. Revenues rose 3% year over year to RMB 243.38 billion, or 11% on a like-for-like basis after excluding the disposed Sun Art and Intime businesses, but profitability cratered.

Non-GAAP earnings per ADS fell 95% to RMB 0.62, and the company posted an operating loss of RMB 848 million against an RMB 28.5 billion operating profit a year earlier. The damage came from two fronts. Alibaba China E-commerce Group’s adjusted EBITA tumbled 40% to RMB 24.01 billion as the company funneled cash into Taobao Instant Commerce, where quick-commerce revenues jumped 57% but margins remained pressured. Simultaneously, Cloud Intelligence Group capex weighed on consolidated earnings even as its revenues climbed 38% to RMB 41.6 billion. Net cash from operating activities for the full fiscal year fell 53% to RMB 76.2 billion, and free cash flow turned deeply negative. The underlying margin story is unambiguously deteriorating.

Guidance Cements a Prolonged Margin Compression

The forward outlook offered no relief. On the fiscal fourth-quarterearnings call management indicated that Alibaba intends to remain equally resolute in continuing aggressive AI infrastructure investment over the next two years, viewing this as a critical window.

The company is targeting AI-related products to exceed 50% of external cloud revenues within roughly one year, and is reaching for an external cloud-and-AI revenue base of over $100 billion within five years. On the consumption side, the company indicated its Taobao Instant Commerce push will not reach the RMB 1 trillion scale or profitability until fiscal 2029.

April 2026 reinforced the spending narrative, as the Qwen team rolled out Qwen3.6-Plus on April 2, Qwen3.6-35B-A3B on April 16, Qwen3.6-Max-Preview on April 20, and Qwen3.6-27B on April 22, alongside Accio Work for cross-border merchants. This pace of model releases requires sustained capex, with management noting server replacement costs have more than doubled year over year. With $38 billion in net cash fueling the spree, BABA has the firepower to keep spending well into fiscal 2027, but with no clear timeline for a return to peak profitability.

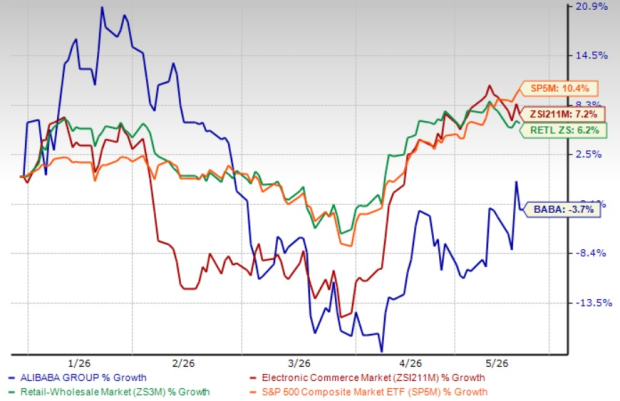

Share Price Movement and Competitive Landscape

BABA shares have declined 3.7% in the year-to-date period, underperforming the Zacks Internet – Commerce industry and the Zacks Retail-Wholesale sector’s growth of 7.2% and 6.2%, respectively.

BABA’s YTD Price Performance

Image Source: Zacks Investment Research

Alibaba’s primary cloud competitors are Amazon AMZN, Microsoft MSFT and Alphabet GOOGL-owned Google, and the comparison is unflattering. Amazon’s AWS continues to dominate global cloud market share, while Amazon’s massive profit machine funds AI at only a fraction of its overall revenue impact. Microsoft has aggressively embedded its AI stack across Azure and Microsoft 365, deepening enterprise stickiness across its installed base. Google leverages its in-house TPUs and Google’s Gemini ecosystem to compete head-on for inference workloads worldwide. Against this trio of much better-capitalized rivals, BABA’s heavy margin sacrifice in fiscal 2026 looks costlier, riskier and far less defensible heading into 2026.

From a valuation standpoint, BABA stock is currently trading at a trailing 12-month EV/EBITDA ratio of 19.03X compared with the industry’s 24.98X. BABA has a Value Score of F.

BABA’s Valuation

Image Source: Zacks Investment Research

What Should Investors Do Now?

With group operating profit erased, free cash flow negative, capex commitments extended through 2029 on the quick-commerce side and two more years of aggressive AI spending ahead, the risk-reward skews unfavorably. Investors holding BABA into 2026 face the prospect of compounding earnings drag without a near-term catalyst for margin recovery. Offloading the stock appears to be the prudent course of action. Alibaba currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Microsoft Corporation (MSFT) : Free Stock Analysis Report

Alphabet Inc. (GOOGL) : Free Stock Analysis Report

Alibaba Group Holding Limited (BABA) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.