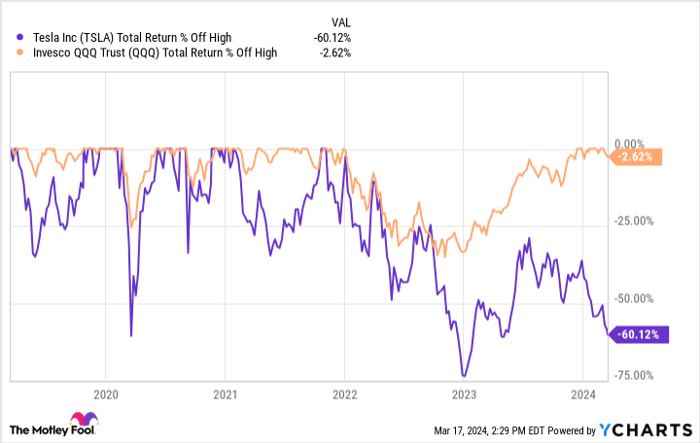

As the stock market veers on an upward trajectory, the spotlight has shifted away from the once-dominant Tesla. Despite the market’s robust performance, Tesla’s shares have taken a tumble, plummeting 34% year to date. The stark contrast between Tesla’s downturn and the Nasdaq-100’s ascent paints a vivid picture of the current landscape.

Investors find themselves at a critical juncture with Tesla stock. Optimists argue that the present represents a golden buying opportunity as the company gears up for its next growth spurt. On the flip side, pessimists contend that Tesla is finally converging towards a more conventional valuation befitting a manufacturing-oriented enterprise.

So, the big question looms – where will Tesla stock stand in three years?

TSLA Total Return Level data by YCharts

Riding the Waves of Volume and Margins

In 2023, Tesla continued its robust expansion in unit volumes, delivering a staggering 1.8 million vehicles worldwide. This marked a significant uptick from 2022’s 1.3 million and 2021’s 936,000 units. Such substantial growth at scale has firmly established Tesla as a premier player not just in electric vehicles but in the broader automotive industry. For context, the world’s largest automaker, Toyota, churns out slightly over 10 million cars annually.

However, achieving this volume growth has necessitated Tesla to slash prices. The company’s product lineup has pivoted towards the more budget-friendly Model 3 and Y models, priced lower than their predecessors, the X and S. Moreover, Tesla has resorted – whether by choice or coercion – to reducing prices on the Model 3 and Y to amplify unit sales. This pricing strategy is exemplified by the sharp decline in the resale value of used Teslas, plummeting by half since early 2022.

The resultant price reductions have translated into decelerating revenue growth and shrinking margins. In 2023, Tesla’s revenue surged by 19% to $97 billion, but tapered to a mere 3% growth in the fourth quarter. Gross margins dwindled from 25.6% in 2022 to 18.2% in 2023, with operating income plummeting by 35% for the year. As Tesla embarks on a quest for global expansion, its margins face erosion.

A New Vehicle to Steer the Ship?

In a bid to reach a broader customer base, Tesla seems poised to introduce a more affordable vehicle. The existing array of vehicles priced at $40,000 and above may hit a saturation point, even with continuous price slashes for the Model 3 and Y across the globe. The global populace with the financial means to purchase premium EVs is inherently limited.

To broaden its market reach, Tesla appears to be gearing up for the unveiling of a budget-friendly vehicle in the coming years. Speculation points towards a probable launch in 2025, with CEO Elon Musk hinting at a rough timeline during a recent earnings call. While Musk’s timelines are notoriously loose, it’s a safe bet to anticipate a new product rollout within the next few years.

Introducing a new vehicle could potentially fuel Tesla’s sales volumes. Yet, if this vehicle hits the market at a $25,000 price point, revenue growth might lag behind unit sales growth. The declining average selling price of Tesla’s vehicles underscores the importance for investors to weigh this factor when projecting Tesla’s revenue trajectory in the foreseeable future.

TSLA Operating Margin (TTM) data by YCharts

A Pricey Proposition

Seasoned investors understand that a stock’s present earnings are dwarfed by its future earning potential. When envisioning Tesla’s positioning several years ahead, a crucial aspect lies in forecasting its financial trajectory. Let’s entertain an optimistic scenario where Tesla triples its 2023 volumes within three years post-launch of the new budget vehicle. With volumes tripled, revenue could conceivably double owing to the dwindling average selling prices.

Assuming Tesla maintains its 2023 profit margins at 9.2%, akin to Toyota’s operating margins for reference, doubling the 2023 revenue to $194 billion and applying a 9.2% profit margin would project Tesla’s earnings to reach $17.8 billion in three years.

Presently, Tesla carries a market capitalization of $512 billion. Dividing this figure by the projected $17.8 billion earnings surfaces a price-to-earnings ratio (P/E) of 29, marginally surpassing the market average. From my vantage point, this hints that Tesla’s stock might stagnate in the coming years. Despite the recent downtrend, Tesla remains relatively overvalued and could potentially ensnare unwary investors in a value trap for an extended period.

If one opts to capitalize on the stock’s dip, a bullish outlook on the company’s future growth trajectory becomes imperative. Otherwise, Tesla’s stock might linger in a state of inertia.

Where to invest $1,000 right now

When our analyst team espouses a stock tip, it tends to pay dividends. The Motley Fool Stock Advisor newsletter, with an illustrious two-decade track record, has significantly outperformed the market.*

They’ve just unveiled their top picks for investors to consider buying right away, featuring Tesla among the elite selection – alongside nine other stocks that may be flying under your radar.

*Stock Advisor returns as of March 18, 2024