The Q3 cycle is over, with the bulk of companies already revealing their quarterly results. The period was again another of positivity, with earnings growth remaining positive and seeing a nice boost from technology.

But one late reporter, lululemon LULU, posted results that positively shocked investors. Let’s take a closer look at the results.

Lulu Enjoys Profitability Boost

Concerningheadline figures in its release, LULU posted a 7% beat relative to the Zacks Consensus EPS estimate and reported sales 2% ahead of expectations, with both items higher than the year-ago period.

Still, the biggest highlight of the release was margin expansion, with the company’s gross margin improving 150 basis points to 20.5%. Gross profit totaled $1.4 billion, climbing a solid 12% year-over-year.

In addition, comparable store sales increased 4% year-over-year, reflecting that their existing location are still experiencing modest growth. And lululemon added 28 new stores throughout the period, expanding its footprint nicely.

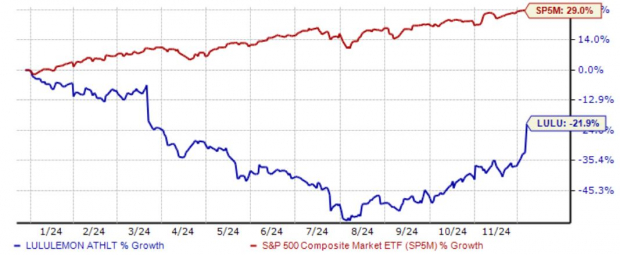

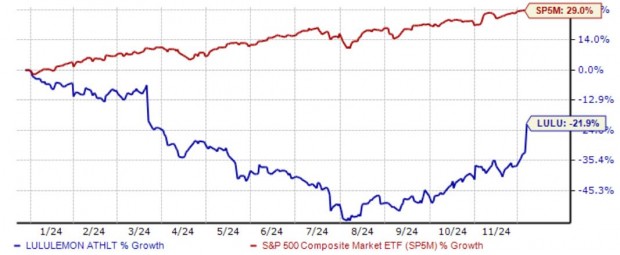

The results perked up shares in a big way, a welcomed development among investors following a rough start to 2024. Up 60% in three months, the stock has bounced back in a big way following a tough start, widely outperforming over the time period. Below is a chart illustrating the year-to-date performance of shares.

Image Source: Zacks Investment Research

Lululemon wrapped up the strong print by announcing a $1 billion increase to its existing buyback program, which can help put in a floor for shares.

Bottom Line

Lululemon LULU helped send the Q3 earnings cycle off in positivity, with the company’s results pleasing investors and causing shares to melt higher following the print.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers “Most Likely for Early Price Pops.”

Since 1988, the full list has beaten the market more than 2X over with an average gain of +24.1% per year. So be sure to give these hand picked 7 your immediate attention.

lululemon athletica inc. (LULU) : Free Stock Analysis Report

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.