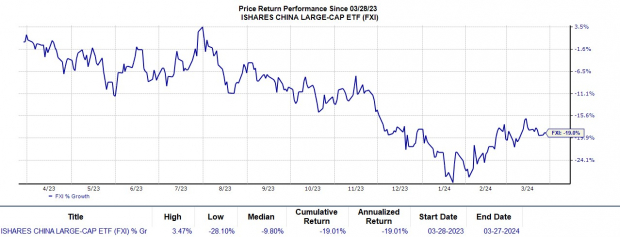

It’s no secret that the tumultuous pit of Chinese equities has left investors clutching their pearls as the iShares China Large-Cap ETF FXI plummeted by an alarming -19% in the past year. However, amidst the chaos, a silver lining emerges – beckoning wise investors to consider Chinese ADRs (American Depository Receipts) that may be on the cusp of a renaissance.

As concerns about China’s economic growth cast a shadow, some Chinese stocks float in the market like oversold relics. Yet, amidst the mist of uncertainty, there are internet-commerce innovators in China standing tall, maintaining their growth momentum in industries brimming with opportunity.

Not to mention, these companies currently trade at tantalizing valuations – providing a gateway to tap into the massive consumer base of China. Let’s not forget, China remains the second-largest economy globally in terms of nominal GDP and snags the title of the largest based on purchasing power.

Revolutionizing Internet Commerce

Dive into the Zacks Internet-Commerce Industry and discover a realm where powerhouses reign. JD.com JD and PDD Holdings PDD capture attention with a Zacks Rank #1 (Strong Buy), firmly planting their flags in the digital landscape.

While Alibaba BABA may reign supreme as China’s e-commerce titan akin to Amazon in the United States, the growth spectacle of JD.com and PDD Holdings signals a seismic market shift – hinting that their presence in your investment portfolio could be a stroke of genius.

JD.com’s revenue trajectory paints a promising future, with sales anticipated to surge by 5% in both fiscal 2024 and FY25, breaching the $160 billion milestone. Equally riveting is the prospect of JD.com’s earnings per share climbing by 12% in FY25, dancing to a tune of $3.53 per share.

The Rise of PDD Holdings

Enter PDD Holdings, a pioneer in the group buying niche, orchestrating a symphony of exponential growth. Predictions whisper of a 50% leap in fiscal 2024 sales to $51.89 billion, striding ahead from $34.64 billion in 2023. Eyes widen at the thought of FY25 sales ascending by 35% to $70.2 billion, while PDD Holdings’ EPS embarks on a journey of a 29% increase this year followed by a 26% surge next year, reaching $10.66 per share. And in a delightful twist, EPS estimates have soared by an astounding 18% for FY24 and 19% for FY25 in the past 30 days.

JD and PDD, though bruised by a 39% and 24% dip from their 52-week peaks respectively, now invite investors with P/E multiples below 20X – a delectable discount compared to the industry norm of 27.4X and the S&P 500’s 22.1X.

Embracing a New Era in Automotives

In a world where electrified vehicles and autonomous driving reign supreme, Li Auto emerges as a formidable player in China’s smart energy vehicle landscape. Sporting a Zacks Rank #2 (Buy), Li Auto strides confidently in the Automotive-Foreign Industry, basking in the glory of the top 36% of all Zacks industries. Despite a 21% rise in the last year, Li Auto’s recent -19% descent in 2022 suggests a ripe buying opportunity.

As the chant for autonomous features grows louder, Li Auto beckons with a forward earnings multiple of 15.7X, a meager offering for the profit surge on the horizon. EPS is poised to leap by 22% in FY24, orchestrating a resplendent 54% crescendo in FY25 to $3.05 per share. Not to be outshone, Li Auto’s top line forecasts glimmer with double-digit percentage growth projections.

A Glimpse into the Entertainment Realm

Completing the roster is Iqiyi – a luminary treading the path of glory, clutching a Zacks Rank #2 (Buy) and often christened as the Netflix NFLX of China. Though the Netflix comparisons may verge on the fanciful, Iqiyi’s stock shines as a beacon for risk-takers, adorned with a Zacks Film and Television Production and Distribution Industry badge in the top 16 percentile.

Having crossed the profitability threshold last year, Iqiyi’s shares beckon with a story of resilience and potential. The potential payoffs of investing in Iqiyi’s stock seem more alluring than ever, painted by the brush of risk and reward in the enigmatic world of entertainment.

Insightful Look at Chinese Equities for 2024 and Beyond

The Rise of Iqiyi’s Potential

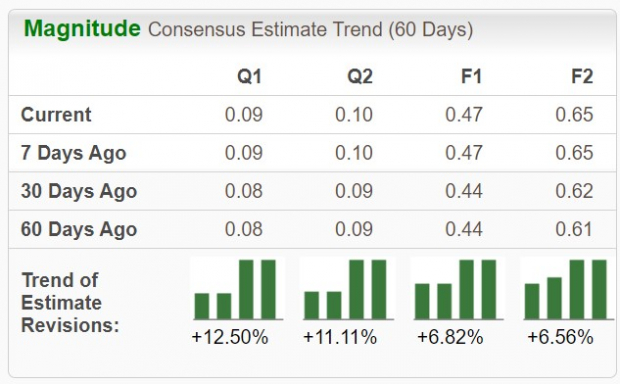

Iqiyi, standing at just $4 with 8.7x forward earnings, is on the cusp of a promising future. Projections indicate annual earnings may surge by 14% in FY24 and escalate further by 38% in FY25, reaching a share value of $0.65. The company’s top-line growth paints a consistent picture, with sales expected to climb by 7% this year and a further 5% in FY25, culminating in $4.91 billion. Analysts have nudged earnings estimate revisions upward modestly over the last 60 days for both FY24 and FY25.

Image Source: Zacks Investment Research

The Potential Bottom Line

With such optimistic outlooks, Chinese stocks are riding a wave of renewed interest, positioning themselves for a robust rebound. As the global economy faces its own ebbs and flows, the allure of these equities cannot be ignored. The timing seems ripe to start building positions, especially as market sentiment is projected to soar again for Chinese securities, once the clouds of economic uncertainty part.