Toll Brothers, after surpassing top and bottom line projections for its fiscal third quarter, finds itself riding a wave of success that could carry it even further. The stock, boasting an impressive over +80% gain year to date, has outshone not only the broader market but also its home builder competitors like KB Home and Lennar Corporation, which have seen increases of more than +50% each.

Image Source: Zacks Investment Research

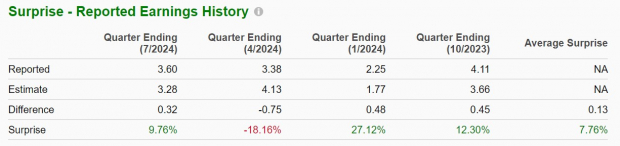

Toll Brothers Q3 Results

In its third quarter, Toll Brothers delivered 2,814 homes at an average price of $968,000, setting a new sales record of $2.72 billion, slightly above the $2.68 billion in the same period last year. Although Q3 EPS dipped to $3.60 from $3.73 the previous year, it still surpassed expectations by 10%. Impressively, Toll Brothers has exceeded earnings estimates in three of its last four quarters with an average EPS surprise of 7.76%.

Image Source: Zacks Investment Research

Revenue Guidance & Growth Trajectory

Toll Brothers now anticipates revenue for the year to be between $10.4 billion and $10.5 billion, an increase of over $200 million relative to previous guidance midpoints. While this falls slightly short of Zacks estimates, with a projected 5% growth, the company is expected to see another 4% increase in its top line in fiscal 2025, reaching $10.98 billion.

Image Source: Zacks Investment Research

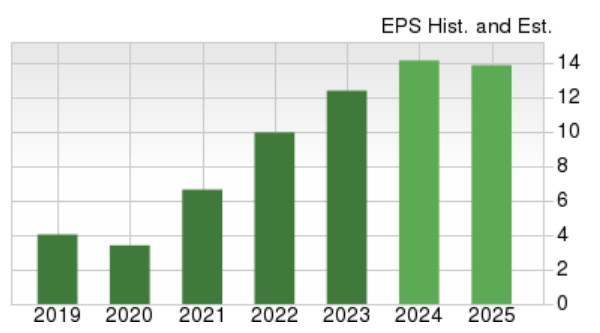

Toll Brothers’ annual earnings are predicted to rise by 14% in FY24 to $14.11 per share from last year’s $12.36. Although there may be a slight -1% dip in fiscal 2025 EPS, estimated at $13.91 per share, this still represents a remarkable 109% growth over the past five years, leaping from $6.63 a share in 2021.

Image Source: Zacks Investment Research

Valuation Comparison

Despite its substantial year-to-date surge, Toll Brothers trades at just 10 times forward earnings, offering a compelling valuation. This remains significantly below the S&P 500’s 23.7 times forward earnings, as well as the Zacks Building Products-Home Builders Industry average of 11.8 times. Comparatively, KB Home trades at 9.8 times and Lennar at 12.6 times forward earnings, continuing to highlight Toll Brothers’ advantageous position.

Image Source: Zacks Investment Research

Bottom Line

Following the Q3 report, Toll Brothers holds a Zacks Rank #2 (Buy), indicating a positive outlook. With a track record of exceeding quarterly expectations, it is likely that earnings estimates will see an upward trend for this homebuilder, sustaining the formidable rally in TOL stock.