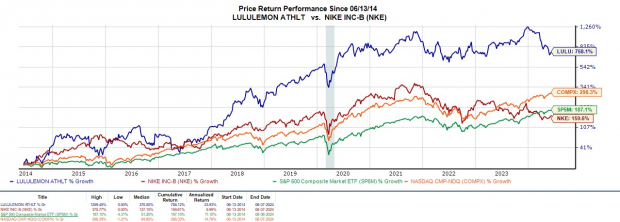

Lululemon’s Q1 Performance in the Limelight

Amidst concerns of a slowdown in consumer spending, Lululemon (LULU) emerged victorious by surpassing both top and bottom-line expectations in Q1. The company saw its sales soar to $2.2 billion, marking a 10% increase from the same quarter last year, beating estimates marginally. On the earnings front, Lululemon posted an EPS of $2.54, exceeding expectations by 7% and demonstrating an impressive 11% growth from the previous year. Remarkably, Lululemon has now surpassed earnings expectations for 16 consecutive quarters, showcasing its unwavering brand loyalty.

Looking Ahead: Revenue Projections and Growth Outlook

For the upcoming quarter, Lululemon anticipates a revenue growth of 9%-10%, slightly outperforming the current Zacks Consensus of 8.23%. The company maintains its full-year revenue growth outlook in the range of 10%-11%, with expectations pointing towards 11.53% growth for the current year. Zacks estimates project a robust 11% increase in Lululemon’s annual earnings for fiscal year 2025, reaching $14.14 per share compared to $12.77 in FY24. Furthermore, FY26 EPS is forecasted to rise by 11% to $15.68.

Analyzing the Takeaway: Is Lululemon a Buy?

Despite the prevailing concerns regarding consumer spending, particularly on premium apparel items, Lululemon’s stock holds a Zacks Rank #3 (Hold). The Q1 results of Lululemon have reinforced its promising earnings outlook. Additionally, trading at a relatively discounted P/E ratio of 22.9X since its IPO, long-term investors could potentially benefit from the current levels, although future buying opportunities might still be on the horizon.