AMD’s stock surged by 3% following its $4.9 billion acquisition announcement of ZT Systems. This strategic move is expected to enhance AMD’s position against Nvidia in the AI market, leveraging ZT Systems’ expertise in data center infrastructure, a pivotal component in the AI ecosystem dominated by Nvidia.

ZT Systems Overview

Established in 1994, ZT Systems, based in New Jersey, specializes in computing and storage solutions for hyperscale cloud computing and internet infrastructure providers. The company also excels in AI and machine-to-machine transactions, boasting $10 billion in revenue last year. AMD envisions incorporating ZT Systems’ talent pool to accelerate the development and deployment of its latest AI GPUs on a scale demanded by tech giants like Microsoft.

Monitoring AMD’s Balance Sheet

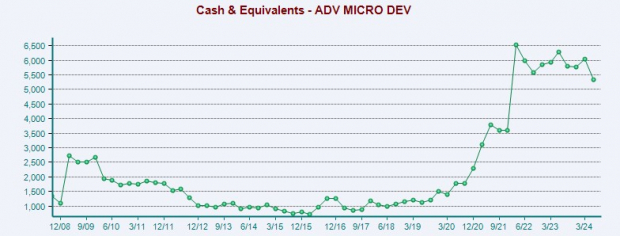

AMD’s acquisition of ZT Systems, with 75% payment in cash, demonstrates the company’s robust financial position, backed by $5.34 billion in cash reserves. The remainder of the acquisition will be financed through stock offerings, aligning well with AMD’s healthy balance sheet that exhibits total assets of $67.88 billion significantly outweighing total liabilities of $11.34 billion.

AMD’s Growth Trajectory

AMD’s growth path continues upwards with anticipated sales growth of 12% in 2024, expected to rise further by 26% in 2025 to reach $32.18 billion. Moreover, earnings for the current year are forecasted to surge by 26% to $3.35 per share, with a projected increase of 54% to $5.17 per share in 2025.

AMD Performance Comparison

Despite a recent rally driving a modest 3% gain this year, AMD lags the broader market, with a significant gap compared to the soaring performance of Nvidia’s stock which rose over 150%. However, over the past two years, AMD has delivered commendable 64% gains, surpassing broader indexes but trailing Nvidia’s remarkable 643% surge.

AMD Valuation Comparison

Currently trading at 44.3X forward earnings, AMD commands a premium over the S&P 500 but remains similar to Nvidia’s valuation of 46.3X and below its five-year high. Trading under this high and below the median valuation during this period signifies a potential price discount, offering promise for value-seeking investors.

Bottom Line

Despite AMD’s current Zacks Rank #3 and a premium valuation, the company’s growth trajectory indicates the likelihood of upward momentum. With a strong balance sheet and the potential amplification of its business through the ZT Systems acquisition, long-term investors may reap significant rewards, bolstering AMD’s position in the competitive tech landscape.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.