In the current financial landscape, artificial intelligence (AI) stocks are captivating investors’ attention with their relentless market dominance. The incredible surge continues for the AI sector as we near the end of February 2024. Among the leaders in this realm, shares of chip behemoth Nvidia (NVDA) have soared by a remarkable 17% since February 21, bolstered by yet another stellar quarterly report.

While Nvidia steadfastly holds its position as the prime selection for AI investors, several other companies are emerging as significant players in the AI domain. Prior to the AI boom, tech giants like Microsoft (MSFT) and Alphabet (GOOGL) diligently fortified their core operations with a diverse array of offerings. Over the past decade, Microsoft’s stock has yielded an impressive 963% return, while Alphabet’s stock has surged by an impressive 352%.

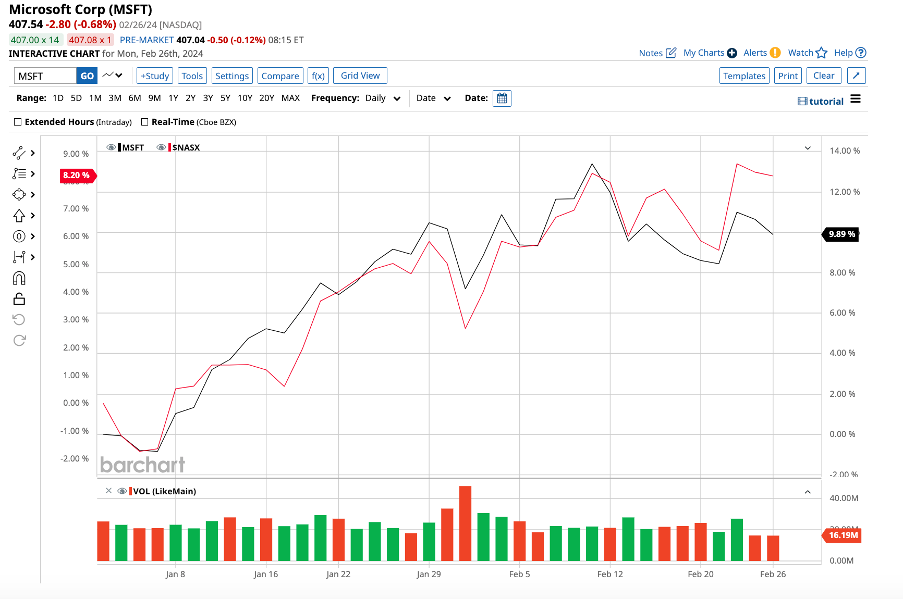

Microsoft’s AI Advancements

Microsoft’s financial performance in 2023 demonstrated exceptional growth fueled by its AI-centric cloud capabilities. With a stock appreciation of 56.8% last year, Microsoft outpaced the tech-heavy Nasdaq Composite, which grew by 44.5%. Currently valued at over $3 trillion, MSFT stock has surged by 8.2% year-to-date, aligning closely with the Nasdaq’s trajectory.

Emerging as an early adopter of AI, Microsoft gained a strategic advantage post a significant investment in OpenAI back in 2019. Subsequently, AI integration became a cornerstone across all its flagship products. Microsoft’s cloud computing platform, Azure, is swiftly encroaching on the territory of the frontrunner, Amazon’s (AMZN) AWS (Amazon Web Services). Azure now commands a 24% market share, narrowing the gap with AWS’s 31% share.

The AI-propelled expansion in the cloud space led to Microsoft recently posting impressive quarterly results. With 53,000 customers, Azure AI witnessed a notable 30% year-over-year growth in the second quarter of fiscal 2024. The Intelligent Cloud segment contributed 42% to Microsoft’s total revenue of $62 billion. While the overall revenue marked an 18% surge, adjusted earnings exhibited a robust 26% increase from the same quarter in the previous year.

Microsoft’s management is optimistic that the new and extended long-term contracts for Azure will elevate the revenue of the Productivity and Business Processes segment by 10% to 12%, projecting a range of $19.3 billion to $19.6 billion in fiscal Q3. Simultaneously, the Intelligent Cloud segment is forecasted to expand by 18% to 19% in the ongoing quarter. The Personal Computing segment is on a recovery trajectory and is anticipated to grow by 11% to 14% in Q3.

Moreover, Microsoft anticipates that around 45% of the remaining performance obligation (RPO) from commercial enterprises, which witnessed a 17% increase in the quarter, could translate into revenue over the upcoming year.

Following its acquisition of Activision Blizzard, Microsoft has unlocked substantial prospects within the gaming sphere. With a robust cash reserve of $81 billion and counting, Microsoft is strategically positioned to further enhance its AI footprint.

Analysts are eyeing an earnings growth of 19.3% in fiscal 2024, coupled with a revenue surge of 15.3%. Looking ahead to fiscal 2025, the earnings growth is estimated at 13.7% alongside a revenue uptick of 14.2%.

Market Sentiment on MSFT Stock

In the panorama of Wall Street evaluations, Microsoft stands tall as a “strong buy.” Out of the 36 analysts tracking the stock, 32 have accorded it a “strong buy” rating, while three have bestowed a “moderate buy” status, with one suggesting a “hold.”

The average target price for MSFT stock stands at $438.97, reflecting a 7.8% upside potential from current levels. With the high estimate pegged at $600, investors could potentially benefit from a substantial 47% surge in the upcoming 12 months.

The Resilience of Alphabet: Weathering the Storm of AI Mishaps

Alphabet experienced a sharp decline in its stock value recently due to complications with Gemini AI. At present, the stock registers a minor decrement on a year-to-date basis, contrasting the Nasdaq’s impressive growth of over 8%.

Following a 4% plunge in GOOGL’s shares on February 26, analyst Daniel Ives from Wedbush expressed his belief that the market reaction may have been exaggerated. Ives remarked that the sell-off was excessive, emphasizing Google’s substantial potential in AI.

Alphabet is set to relaunch its Gemini AI tool in a few weeks, according to reports from Reuters. Despite this setback, I am confident that Alphabet, with its diverse portfolio and market positioning, stands ready to seize opportunities in the AI sector.

Alphabet has been integrating AI into its products since 2017, heightening its focus following Microsoft’s substantial investment in OpenAI. While Microsoft leads the cloud computing market, Google Search maintains supremacy in search engines with a market share of 91.5%, far outpacing Microsoft’s Bing.

In the fourth quarter of 2023, Google Search’s revenue skyrocketed by 12.6% to $42.0 billion. Over the year, Search yielded $175 billion in revenue, marking an 8% annual increase.

Additionally, Google Cloud ranks third in the market behind Amazon and Microsoft, generating $33 billion in revenue for the full year, reflecting a noteworthy 26% upsurge year-over-year. The company’s AI-infused Search and Cloud services are pivotal drivers of growth.

Fueled by its substantial resources, rich industry expertise, and robust balance sheet, Alphabet is primed to take the lead in the AI realm. With a cash balance of $110.9 billion, long-term debt of $13.2 billion, and a $69.5 billion free cash flow in the quarter, the company is well-primed for future success.

Analysts forecast a 16.6% earnings growth and an 11.4% revenue increase for Alphabet in fiscal 2024, with similar projected growth rates in fiscal 2025, underscoring a positive trajectory.

Perspective from Wall Street on GOOGL Stock

Overall, Wall Street views GOOGL stock as a “strong buy,” with 35 out of 44 analysts issuing this recommendation. Price target averages suggest a potential 16% upside in the next 12 months, with high estimates projecting even more substantial gains.

Final Thoughts on AI Stocks

As Microsoft and Alphabet intensify their AI initiatives, they solidify their positions as industry giants. While Microsoft trades at a higher forward earnings multiple than Alphabet, both companies present compelling high-risk/high-reward investment opportunities fueled by long-term AI prospects.

The merger of their traditional portfolios with AI, accompanied by their extensive experience and adept leadership, underpins their remarkable growth and signals probable continued success. The potential for both companies to surpass their high target prices this year and soar even higher is evident, making Microsoft and Alphabet standout choices for long-term AI investments.