Amidst a deluge of market euphoria, the S&P 500 Index catapulted an impressive 24.7% last year. Miraculously, the upward surge has persisted into this year, with the SPX already boasting an 8% growth on a Year-to-Date basis. This jubilation seems slightly dampened this week, amidst concerns over imminent Fed rate cuts.

While the broader market celebrates, not all S&P 500 constituents have partaken in the festivities. The Boeing Company (BA) and Tesla, Inc. (TSLA), two industry titans in their own right, have faced turbulent stock price drops this year, ranking among the weakest performers within the SPX.

If investors seek to capitalize on the decline, which of these underperformers holds greater favor among analysts? Let’s embark on an exploration.

Unpacking Tesla’s Stock Standing

Based in Texas, Tesla, Inc. (TSLA), boasting a market capitalization of $556 billion, is renowned for its pioneering designs and manufacturing of electric vehicles (EVs), solar energy solutions, and energy storage devices. Additionally, Tesla has pivoted towards a future rooted in artificial intelligence (AI), robotics, and automation.

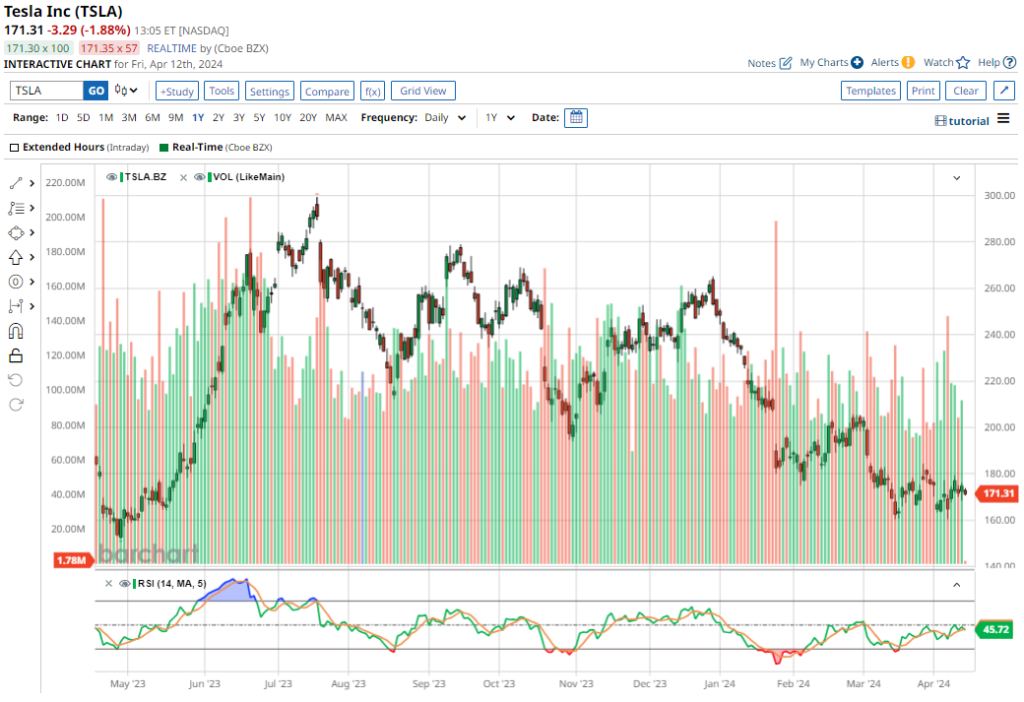

Historically, Tesla has yielded astronomical returns for its shareholders post its 2010 IPO, with the stock surging a remarkable 1,159% over the past decade. Nonetheless, after a staggering performance in 2023, Tesla’s shares have faced immense pressure in the current year.

With a Year-to-Date plummet of 31%, Tesla’s stock lags significantly behind the S&P 500 Index in the same timeframe. Moreover, Tesla’s value has plummeted over 42% from its 52-week zenith of $299.29.

The current stock valuation stands at 77.92 times forward earnings and 5.65 times sales, both exceeding industry averages of 15.31x and 0.92x, respectively. However, these metrics fall below Tesla’s own 5-year averages of 117.53x and 10.86x, respectively.

Tesla’s Struggle with Deliveries Persists

Aside from a fleeting resurgence this week, Tesla’s investors have little cause for celebration, especially in light of the company’s underwhelming Q1 delivery figures, precipitating a 4.9% slide in TSLA stock on Apr. 2. Tesla’s deliveries slogged to 387,000 vehicles, marking its initial yearly decline since the COVID-19 outbreak in 2020.

In the realm of earnings, Tesla reported Q4 earnings of $0.71 per share on Jan. 24, below Wall Street estimates by 5%, amidst sales of $25.2 billion – a mere 3% yearly increase but a miss compared to the forecasted $25.8 billion. As fiscal 2023 drew to a close, Tesla amassed $29.1 billion in cash, cash equivalents, and short-term investments, marking a 31% annual climb. Earnings for the fiscal quarter concluding in Mar. 2024 are anticipated post-market closure on Apr. 23.

Analysts anticipate Tesla to announce a profit of $2.20 per share for fiscal 2024, representing a 15.4% downturn from the prior year, with a subsequent surge to $2.98 in fiscal 2025, marking a 35.5% upswing.

Alas, analysts have begun to exercise prudence with Tesla stock. Last month, Wells Fargo’s Colin Langan downgraded Tesla to “Underweight” from “Equal Weight,” in conjunction with hacking the price target to $125 per share from $200.

Currently holding a consensus “Hold” rating, Tesla garnered a “Moderate Buy” standing three months prior. Among the 29 analysts tracking Tesla, six advocate “Strong Buy,” two propose “Moderate Buy,” 16 lean towards a “Hold,” while five recommend “Strong Sell.”

The average price target of $195.26 signifies a modest upside potential of around 13.8% from existing levels. Conversely, the lofty price target of $310, freshly trimmed by analysts at Morgan Stanley (MS) this April, signals a possible 80% upsurge from current valuations.

Evaluating Boeing’s Stock Scenario

Boeing (BA), commanding a market value of $105.7 billion, stands as an aviation stalwart headquartered in Arlington, Virginia. Boasting iconic aircraft such as the 737, 747, and 787 Dreamliner, Boeing’s market dominance bequeaths it a formidable presence in the global aerospace domain.

Boeing’s stock has toppled by 34.5% on a Year-to-Date basis, woefully trailing the SPX’s trajectory.

Boeing Exceeds Q4 Revenue Estimates and Mitigates Losses

Boeing unveiled its Q4 outcomes on Jan. 31, with revenue climbing 10% to $22 billion, triumphing over Wall Street predictions by 4.5%. The company curtailed its net loss to a mere $30 million, featuring a core loss per share of $0.47 – eclipsing analysts’ forecasts by a substantial 34.7%. Relatively, there was a marginal uptick in new jetliner deliveries to 157, coupled with 611 net orders for commercial airplanes.

In light of an episode on Jan. 5, where an Alaska Airlines-operated 737 Max 9 encountered a midflight panel blowout, Boeing refrained from furnishing a 2024 forecast, citing ensuing uncertainties.

Boeing: Navigating Turbulent Skies Amidst Analyst Revisions

A Political Twist: Rep. Bill Keating’s Sale of Boeing Shares

In an interesting turn of events, Rep. Bill Keating recently offloaded Boeing shares worth up to $15,000, as per Quiver Quantitative data. Keating, a member of the Armed Services and Foreign Affairs Committees, made this move on Feb. 28. This sale adds an intriguing political dimension to Boeing’s stock movements.

Analyst Projections: From Losses to Future Gains

Analysts closely monitoring Boeing expect a significant turnaround for the company. Forecasts predict a shift from a fiscal 2023 loss of $3.67 per share to a profit of $0.75 in fiscal 2024. These projections indicate further growth, with earnings per share (EPS) estimated to reach $6.12 in fiscal 2025. The future seems promising for the aviation giant.

Analyst Revisions and Market Sentiment

Despite ongoing challenges, including whistleblower reports and a recent CEO shakeup, analysts have revised their outlook on Boeing’s share price. Bank of America recently lowered the stock’s target price to $190 from $210, maintaining a “Neutral” rating. Additionally, Bernstein’s Douglas Harned slashed Boeing’s price target by 11.8% to $240 on Apr. 8 while continuing to endorse a “Buy” stance.

Current Ratings and Price Targets

Boeing retains a consensus “Moderate Buy” rating, a slight downgrade from the previous “Strong Buy” status. Out of 21 analysts covering Boeing, 14 recommend a “Strong Buy,” one suggests a “Moderate Buy,” and six advise to “Hold.” The average price target of $247.95 indicates a potential upside of over 45% from current levels. Moreover, the high target of $300 implies a potential rally of up to 76.3%.

Boeing vs. Tesla: Analyst Preferences

Amidst contrasting views, Boeing seems to have an edge over Tesla according to analyst sentiment. While Tesla holds a consensus “Hold” rating with moderate upside potential, Boeing’s positive outlook stems from sustained demand in aviation and space exploration. Despite recent setbacks affecting Boeing, including the 737 Max grounding and manufacturing issues, analysts believe in the firm’s resilience. This preference is highlighted by Boeing’s “Moderate Buy” rating and promising upside potential over Tesla at the current juncture.