TEGNA shares have taken a beating, dropping a substantial 9% year to date (YTD), a stark contrast to the 2.4% uptick in the broader Zacks Consumer Discretionary Sector. Racing behind industry stalwarts like Netflix, Fox, and Nexstar Media Group, TEGNA finds itself in turbulent waters, lagging behind competitors who have seen their shares soar by double-digit percentages.

What has brought about this tumultuous decline in TEGNA’s fortunes, you may ask? Well, a cocktail of factors – dwindling subscription revenues, service interruptions with distribution partners, and lackluster performance in Advertising and Marketing Services (AMS) have all conspired to dent TEGNA’s bottom line.

However, all hope is not lost. The first half of 2024 saw a glimmer of light in the form of a surge in political revenues and the promise of increased top-line growth in the upcoming months. TEGNA has also shown prowess in keeping its expenses in check, a move that bodes well for the jittery investors.

So, will the impending surge in political revenues coupled with prudent cost management be enough to steer TEGNA’s ship through the stormy seas? Let’s delve deeper into this conundrum.

Revolutionizing Advertising with Premion: A Silver Lining for TEGNA?

Integrating Octillion into its arsenal, TEGNA has bolstered its flagship CTV/OTT advertising platform, Premion. This strategic move has widened Premion’s reach to 210 markets, amplifying its local revenue streams while battling headwinds in national Premion revenues.

Optimism looms large as TEGNA anticipates a surge in political advertising revenue, fueling Premion’s growth trajectory in the coming year. With the addition of Octillion, the future looks promising for TEGNA’s advertising endeavors.

Weathering the Earnings Storm: What Lies Ahead for TEGNA?

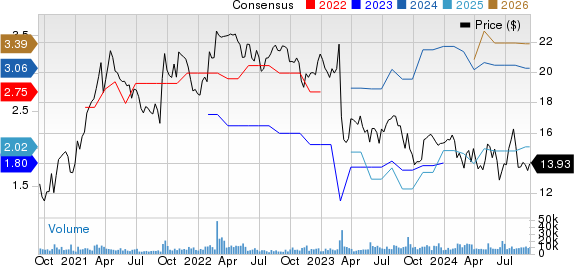

While TEGNA puts up a brave front, the Zacks Consensus Estimate paints a slightly grim picture. The downward trend in earnings estimates for the third quarter and the full year of 2024 raises concerns about the company’s profitability.

Despite the cloudy forecast, there’s a glimmer of hope with year-over-year revenue growth in the offing, albeit at a moderate pace. TEGNA’s ability to navigate through these choppy waters remains to be seen.

Strategic Choices Ahead: Buy, Hold, or Sell?

As TEGNA shares find themselves undervalued, signaling a potential opportunity for bargain hunters, caution is advised in light of the challenges in subscription and AMS revenues. With a Zacks Rank #3 (Hold), investors are advised to bide their time for a more auspicious entry point.

Amidst this financial tempest, the fate of TEGNA hangs in the balance. Will it emerge unscathed from the storm or succumb to the pressures brewing beneath the surface? Only time will tell as investors tread cautiously in these uncertain times.