SpaceX is about to go public and the space economy just changed forever.

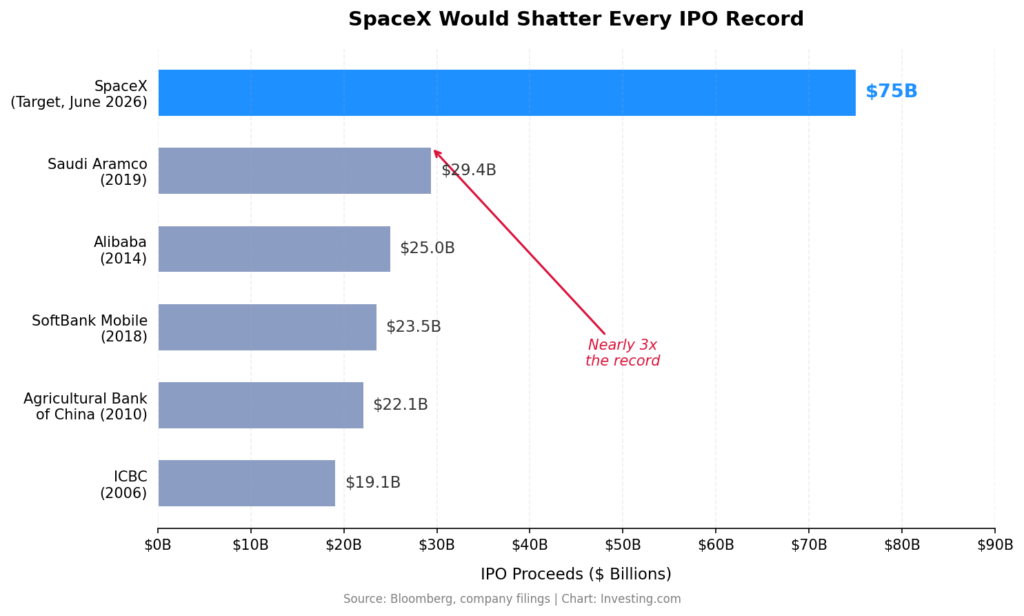

Bloomberg reported Tuesday that Elon Musk’s rocket and satellite company is preparing to file its S-1 prospectus as early as this week, targeting roughly $75 billion in proceeds. That would make it the largest initial public offering in history and nearly three times the $29.4 billion Saudi Aramco raised in 2019. The combined entity, which now includes Musk’s xAI artificial intelligence venture after a February all-stock merger, is expected to seek a valuation of $1.5 trillion to $1.75 trillion when it lists, likely in June.

The market’s reaction was immediate. surged 10%. jumped 12%. Firefly Aerospace (FLY) rocketed 16%. climbed nearly 15%. The message from the market was clear: when the biggest player in an industry goes public, it lifts the entire sector.

Why This IPO Changes the Math

Let’s be specific about what SpaceX actually is in 2026, because it’s not the same company most investors still picture. Starlink, the satellite internet division, now has over 9.2 million active subscribers and generated more than $16 billion in revenue last year. Analysts project that figure will reach $20 billion to $24 billion in 2026. Those aren’t aerospace margins, they’re software-like margins on a global telecom utility. That’s the business that justifies a trillion-dollar-plus valuation.

The launch business remains dominant. SpaceX controls roughly 80% of global commercial launch mass. Starship, the most powerful rocket ever built, has successfully delivered payloads to orbit and is now the backbone of the Starlink V3 constellation buildout. The xAI integration adds another dimension entirely — Musk’s vision of space-based AI computing through orbital data centers is speculative, sure, but it’s the kind of narrative that drives IPO premiums.

The confidential SEC filing allows SpaceX to address regulatory complexities privately before the public roadshow begins. If timelines hold, institutional investors will be pricing allocations by April.

Here’s what matters for public market investors: you can’t buy SpaceX stock today. But you can position in the companies that will benefit most from the tsunami of capital about to flood into the space sector.

How to Play It

- Rocket Lab (RKLB) — The closest public-market proxy to SpaceX. At around $71, Rocket Lab is the second-most-active launch provider in the world, having completed 84 Electron missions. The company reported 38% year-over-year revenue growth in Q4 2025, with total revenue reaching $602 million. But the real story is what’s coming: the Neutron rocket, designed to compete directly with SpaceX’s Falcon 9, is scheduled for its inaugural launch in late 2026. Rocket Lab’s backlog now exceeds $2 billion, including a $190 million hypersonic test contract with the Department of Defense announced earlier this month. Cash and marketable securities hit $977 million, up 121% year-over-year. Bank of America has a $120 price target — implying roughly 69% upside from current levels. The median consensus sits around $90, suggesting 27% upside even on conservative estimates. When SpaceX goes public at $1.5 trillion, every analyst on Wall Street will be re-rating its publicly traded competitors.

- AST SpaceMobile (ASTS) — The direct-to-device satellite play. At around $93, ASTS is building something that didn’t exist three years ago: a cellular broadband network in space that works with standard, unmodified smartphones. The company now has 25 satellites in orbit, is on track for “intermittent nationwide” U.S. service by the end of this quarter, and holds over $1 billion in contracted revenue commitments from more than 50 mobile network operators globally. Q4 2025 revenue hit $54.3 million, beating estimates by 38%. Full-year revenue surged 641% to $70.9 million with a 69% gross margin. The company just secured a $30 million U.S. government tactical demonstration contract. Here’s my read: if SpaceX’s Starlink Direct-to-Cell service validates the market, ASTS — which has a head start on the technology and carrier partnerships with AT&T and Verizon — becomes the purest way to play the “connectivity everywhere” thesis. Canaccord Genuity has a $139 target.

- Firefly Aerospace (FLY) — The small-cap launch disruptor. At around $27, Firefly is the highest-beta name on this list and arguably the most undervalued relative to its trajectory. The company reported record Q4 revenue of $57.7 million, beating estimates by 10%. Full-year 2025 revenue hit $159.9 million, up 163%, with 80% of projected 2026 revenue of $435 million already booked. The backlog stands at $1.4 billion, up 22% year-over-year. Firefly’s Alpha rocket has completed successful orbital missions, and the company is developing the larger Beta vehicle to capture medium-lift market share. Goldman Sachs initiated with a Buy rating and a $29 target, while the consensus average of $37 implies roughly 37% upside. At a $3.8 billion market cap, Firefly is trading at less than 9 times forward revenue — a fraction of Rocket Lab’s multiple.

- Intuitive Machines (LUNR) — NASA’s moon partner. At around $19, Intuitive Machines is the only company on this list with a contract to build permanent infrastructure on another world. The $4.8 billion Near Space Network contract, awarded in 2024, makes LUNR the linchpin of NASA’s communications architecture between Earth and the Moon through 2034. Revenue guidance for 2026 is $900 million to $1 billion — a massive step-up from the $210 million reported in 2025. NASA Administrator Jared Isaacman’s “Ignition” announcement this week committed $20 billion to building a permanent American moon base by 2032, and LUNR’s Nova-C and Nova-D landers are central to that vision. The company also secured a $180.4 million lunar payload delivery contract this week, sending shares up 15% in a single session. Stifel’s $22 target implies 13% near-term upside, but the multi-year contract pipeline suggests significantly more if execution holds.

- — For investors who want broad exposure without betting on a single name, UFO tracks the S-Network Space Index and holds positions across the entire aerospace and satellite value chain. The ETF has returned over 100% in the past year, reflecting the sector-wide re-rating driven by SpaceX momentum, defense spending, and satellite demand. The 0.75% expense ratio is higher than broad market ETFs, but you’re paying for targeted access to a sector that most index funds barely touch. UFO’s top holdings include both satellite operators and defense contractors, providing a natural hedge between commercial space optimism and government spending stability.

The Bear Case You Need to Hear

Here’s where I have to pump the brakes. The SpaceX IPO hype is real, but so are the risks.

First, valuation. RKLB trades at roughly 59 times trailing revenue. ASTS trades at over 500 times. These are momentum multiples, not fundamental ones. If SpaceX’s IPO disappoints — a botched Starship test, regulatory delays, a valuation haircut to $1 trillion — the entire sector gives back weeks of gains in a single session. History isn’t kind to mega-IPOs: Saudi Aramco, Alibaba, and Meta all traded below their IPO price within months of listing.

Second, profitability remains elusive. RKLB lost $198 million in 2025. ASTS lost $236 million. FLY and LUNR are both deeply unprofitable. The bull case requires continued access to capital markets, and with oil above $100 and the OECD projecting U.S. inflation at 4.2%, funding windows could narrow.

Third, SpaceX itself is the competition. Starlink’s Direct-to-Cell service directly threatens ASTS’s addressable market. Falcon 9 and Starship dominate the launch market that RKLB and FLY are trying to crack. Going public gives SpaceX even more capital to press those advantages.

My read: the structural tailwinds are real. Government space spending is accelerating. Commercial satellite demand is surging. The “Golden Dome” missile defense system alone represents $151 billion in contracts. But pick your spots carefully, and don’t chase 16% single-day pops at the open.

What to Watch

Three catalysts in the next 30 days. First, the SpaceX S-1 filing itself — expected any day now. When the prospectus drops, every data point on Starlink revenue, subscriber growth, and xAI integration will be parsed by thousands of analysts. The numbers will either confirm the $1.75 trillion thesis or force a reset. Either way, it moves the entire sector.

Second, ASTS nationwide service launch — expected by the end of Q1 2026. If AST SpaceMobile successfully demonstrates intermittent direct-to-device coverage across the continental U.S. this month, it validates the technology thesis and triggers the next wave of carrier partnerships.

Third, Rocket Lab earnings on May 13 — the first quarter that will reflect the $190 million HASTE hypersonic contract and updated Neutron development timeline. Revenue guidance above the $870 million consensus for 2026 would confirm that Rocket Lab’s transition from small-launch specialist to medium-lift competitor is real, not aspirational.

The space economy isn’t a bet on the future anymore. It’s a $600 billion industry growing at 9% annually, and SpaceX going public is about to pour rocket fuel on the fire. Position accordingly.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.