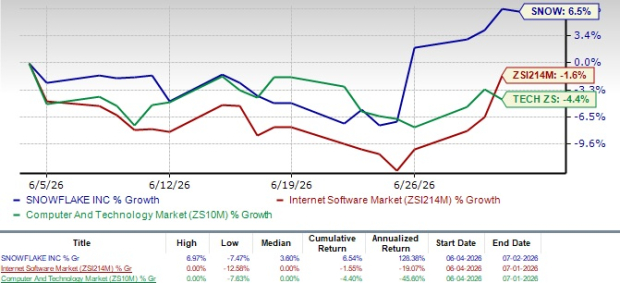

Snowflake SNOW shares have risen 6.5% in a month, outperforming the broader Zacks Computer & Technology sector’s decline of 4.4% and the Internet Software industry’s decline of 1.6%.

The outperformance can be attributed to SNOW’s strong adoption and increasing usage of its platform, as reflected by the net revenue retention rate of 126% in the first quarter of fiscal 2027.

In the first quarter of fiscal 2027, Snowflake reported 13,912 total customers and added 616 net new customers, up 38% year over year, including 13 new Forbes Global 2000 customers. The company now has 779 customers spending more than $1 million annually, up 29% year over year, and the number of customers spending more than $10 million annually increased to 64.

SNOW Stock Performance

Image Source: Zacks Investment Research

Snowflake Benefits From Strong AI Platform Demand

SNOW is benefiting from a strategic expansion of its AI reach through deepening partnerships and innovative product launches. In the first quarter of fiscal 2027, new customers such as Holiday Inn Club Vacations and Houzz selected Snowflake as the foundation for their data and AI transformation initiatives. The adoption of Snowflake AI capabilities continued to expand, with more than 13,600 accounts now leveraging these solutions.

Building on this momentum, in June 2026, Snowflake announced that Sanofi SNY had launched Concierge for Field, an AI agent created with Snowflake Cortex AI. The tool launched by Sanofi helps global sales representatives prepare for physician visits in seconds. It generates pre-call plans, prioritizes physicians based on specialty and prescribing history, reviews past engagements and emails meeting summaries. This replaces hours of manual research.

Beyond field sales, Sanofi is also expanding AI agents into R&D, procurement, IT and HR as part of its overall AI strategy. Built on Snowflake’s unified data platform, with Elementum’s AI applications and supported by Snowflake’s Forward Deployed Engineers, the initiative aims to accelerate drug development and improve efficiency across the biopharmaceutical company.

SNOW Offers Positive Guidance

Snowflake’s rich partner base and innovative AI portfolio are expected to drive the company’s top-line growth.

The Zacks Consensus Estimate for the fiscal second-quarter revenues is currently pegged at $1.47 billion, indicating 28.39% year-over-year growth.

The consensus mark for earnings is currently pegged at 45 cents per share, which has remained unchanged over the past 30 days. This suggests an increase of 28.57% year over year.

Snowflake Inc. Price and Consensus

Snowflake Inc. price-consensus-chart | Snowflake Inc. Quote

SNOW Grapples With AI Competition and Margin Drag

Despite Snowflake’s expanding AI portfolio and partner base, the company competes with large cloud platforms and other data platforms that bundle data warehousing, analytics and AI capabilities.

The company is facing stiff competition from the likes of major players like Oracle ORCL and Amazon AMZN, which are also expanding their footprint in the AI space.

Amazon’s AI initiatives gained significant momentum during the first quarter of 2026. Amazon’s cloud computing platform, Amazon Web Services’ chips business, including Graviton, Trainium, and Nitro, exceeded a $20 billion annual revenue run rate and is growing triple-digit percentages year over year.

Oracle’s expanding portfolio has been noteworthy. In June 2026, Oracle introduced Oracle OPERA Cloud Assistant, a suite of AI-powered capabilities built into OPERA Cloud that automates guest room assignments, generates AI-driven rate descriptions, supports multilingual operations across 230 countries and territories and gives hotel staff real-time operational guidance.

Snowflake suffers from the variability of consumption as customers optimize spend and AI products that carry lower gross margins than the core platform. Integration and hiring tied to acquisitions also weigh on free cash flow margins. Snowflake expects a 150-basis-point drag to its non-GAAP adjusted free cash flow margin from the Observe acquisition, and management reiterated this impact in its fiscal 2027 outlook.

SNOW Trades at a Premium

Snowflake shares are currently overvalued, as suggested by its Value Score of F.

SNOW stock is trading at a premium with a forward 12-month Price/Sales of 13.48X compared with the Internet Software industry’s 3.82X.

SNOW’s Valuation

Image Source: Zacks Investment Research

What Should Investors Do With SNOW Stock?

Despite SNOW’s robust portfolio, the company suffers from challenging macroeconomic uncertainties and variability of consumption as customers optimize spending on AI products that carry lower gross margins than the core platform. Stiff competition and stretched valuation also remain concerns.

SNOW currently carries a Zacks Rank #3 (Hold), suggesting that it may be wise to wait for a more favorable entry point in the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI’s Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren’t likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

Snowflake Inc. (SNOW) : Free Stock Analysis Report

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Sanofi (SNY) : Free Stock Analysis Report

Oracle Corporation (ORCL) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.