The seasonal rollercoaster: evaluating past numbers and forecasting the future

History whispers a cautionary tale about September’s volatile nature.

Over nearly a century, the S&P has danced with September 42 times in gains, leaving 53 losing years to face a 4.7% average decline.

The recent trio of Septembers stands as a testament to the tumult:

- 2021: -4.8%

- 2022: -9.3%

- 2023: -4.9%

While bracing for potential market turbulence is wise, wisdom reminds us that sunny days often follow stormy nights in the market realm.

Delving Deeper: Beyond the Usual Suspects

The road ahead appears bifurcated.

Standard seasonal fluctuations notwithstanding, our current economic landscape deviates significantly from the norm.

Several market indicators are waving red flags at us, signaling potential instability lurking beneath the surface.

Should the stocks tumble, distinguishing between typical seasonal jitters and something more ominous would be our next mental acrobatics.

Let’s take a peek at this “instability” canvas before we dissect the present scenario further.

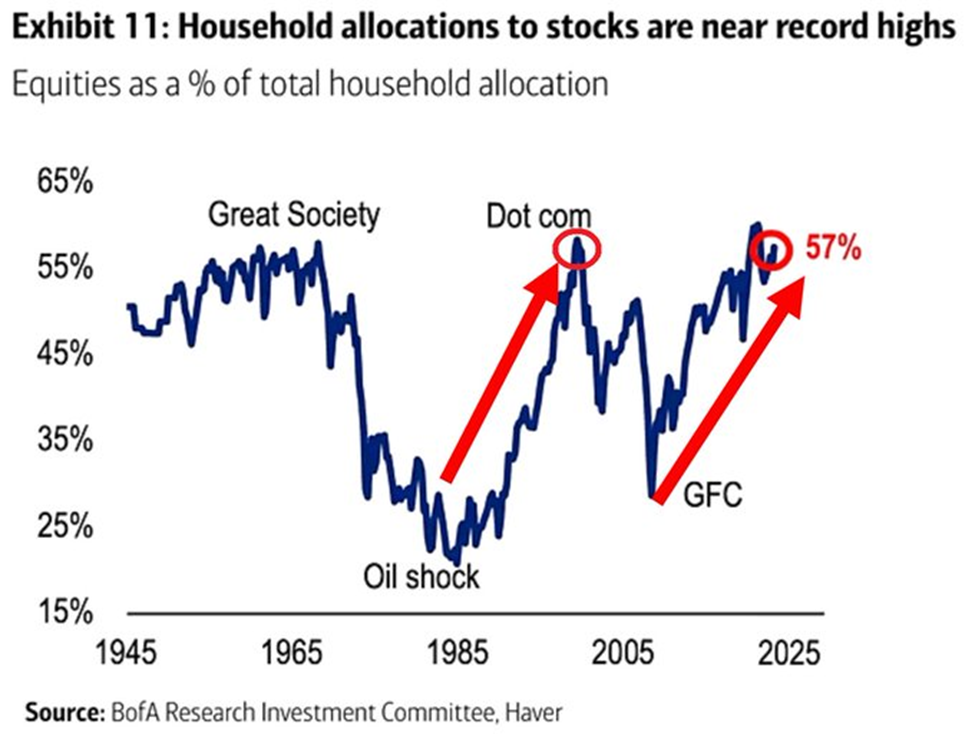

Approaching Peak: Household Stock Allocation Reaches Record Highs

Consulting Global Markets Investor provides a sobering revelation:

The proportion of stocks in US households recently hit 57%, nearing an all-time pinnacle.

The surge in stocks ownership by Americans rattles the investment sphere as it shadows the alarming figures witnessed during the 2000 Dot-Com bubble burst.

For the seasoned observer, such bloated stock ownership percentages often signal trouble ahead. The logic is simple: with more folks invested, the market’s ceiling lowers, hindering further price escalations.

As noted by Stéphane Renevier from Finimize – the single most influential factor tipping the stock scales is the proportion of assets parked in equities. This yardstick outperforms all others in predicting future returns.

The statistics might allow for optimistic interpretations due to the incessant rise in stock ownership. However, statistically, the outlook is dim. The discussion shall resume shortly.

Market Secrets Exposed: Unprecedented Concentration Surpasses Dot-Com Era

According to the recent findings outlined in The Kobeissi Letter, the dominance of tech, telecom, and healthcare sectors in global stocks has hit an all-time high of 45% in July 2024.

This staggering figure, ballooning by 10 percentage points in just four years, eclipses the former peak of 44% achieved during the Dot-Com era in 2000.

Conversely, the weight of financial, energy, and materials sectors relative to global stocks has dwindled to 25%, swiftly approaching the 24% benchmark set during the Dot-Com peak.

While not indicative of an imminent market crash, this anomaly underscores the precarious tightrope the market is treading on.

Housing Highs: Bubble Trouble or Price Peaks?

As per Nick Gerli, the head of Re:venture Consulting, inflation-adjusted home prices have reached unprecedented levels, sitting close to double their historical average over the last 130 years.

The figures paint a vivid picture:

The Housing Market Conundrum: A Deeper Dive

Reframing the Housing Bubble Narrative

In discussions about the current state of the housing market, the term “bubble” is thrown around with alarming frequency. Nick Gerli, CEO of Re:venture Consulting, has raised concerns about inflation-adjusted home prices skyrocketing to nearly double their 130-year average, indicating a precarious scenario that mirrors historical precedents – namely, 2006. However, a closer inspection reveals a different narrative.

Government Intervention and Monetary Impact

Contrary to traditional bubble dynamics where excessive funds flow into a single market, the recent surge in housing prices can be partly attributed to an influx of government stimulus. Visualizing the M2 Money Supply trend alongside the Median Sales Price of Houses Sold delineates a tale of money cascading into the economy and subsequently trickling into the housing sector, amplifying property values.

Redefining the “New Normal”

With money infused into the economy and housing market, the concept of a catastrophic crash seems less probable. Rather, a “new normal” baseline may emerge, elevating home prices to unprecedented levels. Unless a severe deflationary period ensues, the trajectory of the housing market appears destined for sustained elevation.

The Disparity Dilemma

As the housing market climbs to new heights, a divergence between the “haves” and “have nots” becomes increasingly evident. The surge in 401(k) millionaires reflects the prosperity of some, yet it starkly contrasts with the financial strains faced by others. This widening wealth gap intensifies the instability plaguing the housing market.

The Current Financial Landscape Unveiled

Credit card debt is soaring to new heights while the savings rate plunges to a record low, painting a contrasting picture of the financial health of the nation. The juxtaposition of these two extremes underscores a deeper societal divide in wealth distribution as Americans grapple with preparing for retirement amidst economic uncertainties.

The Retirement Conundrum: Millionaires and the Masses

Despite the surge in the number of 401(k) millionaires, a stark reality emerges as most Americans face a retirement savings shortfall. The average 401(k) balance of approximately $127,000 may appear promising, having increased by 13% within a year. However, this pales in comparison to the nearly $1.5 million estimated as necessary for a comfortable retirement.

Research unveils a disheartening trend, with only a fraction of 55-year-olds having saved $447,000 or more, indicating widespread unpreparedness for retirement. The retirement dreams of many seem like a distant mirage, with half of Gen X respondents believing a miracle is needed to retire.

Renowned economist Teresa Ghilarducci sheds light on the disparity in retirement readiness, emphasizing the challenge faced by lower-income individuals against a backdrop of elongated retirements for the wealthy.

The Stock Market Odyssey: Peaks and Valleys

While stock ownership nears all-time highs, a fundamental question arises — will individuals grappling with multiple jobs and financial strain have the capacity to invest in stocks? The disparity between the wealthy stock owners and the financially strained workforce hints at an impending dilemma in market sustainability.

Amidst record stock ownership, the optimism surrounding a potential influx of cash into the market is met with skepticism, highlighting uncertainties in market dynamics. As gold purchases by central banks surge and global debt skyrockets, signs of economic fragility tinge the financial horizon.

The Ticking Time Bomb: Inverted Yield Curve

The recently flattened yield curve, characterized as a precursor to recession, looms ominously in the financial sphere. With mounting unrealized losses on bank balance sheets and global debt reaching unprecedented levels, signs of economic turbulence intensify.

Despite the market exuberance, underlying destabilization hints at caution. While staying invested is pivotal, meticulous portfolio evaluation and stop-loss strategies are imperative to navigate potential market volatility without succumbing to fear-induced decisions.

A Call to Vigilance and Preparation

Striking a balance between maintaining steadfast core investments and safeguarding speculative holdings becomes paramount in navigating the evolving market landscape. Establishing a resilient trading framework, such as stage analysis, can fortify investment strategies amidst market fluctuations.

Embracing preparedness shields against the tempestuous seas of market instability and ensures the safeguarding of investment objectives. As uncertainties loom, preemptive measures can insulate against the storm and uphold financial resilience.

Jeff Remsburg