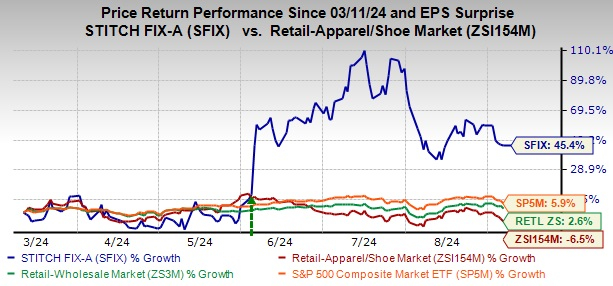

Stitch Fix, Inc. SFIX has undergone a remarkable 45.4% surge in its stock price over the last six months, surpassing the Zacks Retail-Apparel and Shoes industry’s 6.5% decline. This transformative growth trajectory stems from the company’s strategic endeavors, including AI-powered inventory management, pricing optimizations, margin expansions, enhanced client engagement, and improved cost efficiency.

These measures have propelled Stitch Fix to outshine both the broader Retail-Wholesale sector and the S&P 500 Index, which experienced growth of 2.6% and 5.9%, respectively, during the same period. This remarkable surge has left investors pondering whether they have missed a golden chance or if there is still room for further growth. At a closing price of $3.46 as of Sept. 6, SFIX stock is approaching its 52-week high of $5.05 achieved on July 16, 2024.

Technical analyses support Stitch Fix’s robust performance. The stock is trading above both its 100-day and 200-day moving averages, underscoring strong upward momentum and price stability. This technical strength portrays positive market sentiment and a vote of confidence in SFIX’s financial well-being and future prospects.

From a valuation viewpoint, the stock presents an enticing opportunity, trading at a discount compared to historical and industry standards. With a forward 12-month price-to-sales ratio of 0.33, below the five-year median of 0.54 and the industry average of 1.04, the stock offers compelling value for investors seeking exposure to the sector. Additionally, with a Value Score of A, the stock further proves its attractiveness.

Image Source: Zacks Investment Research

Driving Growth Through Strategic Initiatives

Stitch Fix continues its growth trajectory by harnessing AI and data analytics, which have become integral to the company’s operations. Central to this success is the implementation of an AI-driven inventory buying tool, now influencing nearly half of all inventory decisions, significantly enhancing efficiency compared to traditional methods. This strategic deployment of AI underscores Stitch Fix’s dedication to innovating business procedures and maintaining a competitive edge.

The rollout of Quick Fixes, a feature enabling clients to schedule an additional fix immediately after checkout, has led to a 25% surge in average order value within three weeks, showcasing the company’s agility in meeting client demands. Furthermore, a comprehensive review of pricing structures has resulted in adjustments anticipated to yield over $20 million in annualized contribution profit, aligning prices with perceived value and amplifying profitability.

Stitch Fix has made substantial advancements in margin expansion and operational efficiency. In the third quarter of fiscal 2024, the company reported a 280-basis-point year-over-year increase in gross margin, reaching 45.5%. This enhancement stemmed from robust product margins and enhanced transportation leverage, reflecting the company’s strategic emphasis on optimizing pricing and inventory management.

Enhancing the overall client experience remains a top priority for Stitch Fix. The company has introduced more dynamic and personalized interactions, such as increasing the number of items in each fix, refining discount strategies, and enhancing the onboarding process. These initiatives have yielded promising results, with higher average order values and improved retention metrics, indicating robust client satisfaction and loyalty.

The introduction of Stitch Fix Freestyle has ushered in a distinctive shopping experience, allowing customers to explore and purchase curated items based on their style preferences, fit, and size, without the prerequisite of a Fix first. This initiative aligns with the company’s broader strategy to expand its client base and achieve sustained profitability.

On the marketing front, Stitch Fix is recalibrating its strategy to prioritize liquidity preservation and profitability by focusing on high-lifetime-value clients. The company is also streamlining its operations by consolidating U.S. warehouse locations from five to three and successfully divesting its U.K. operations, further aligning SFIX’s business for enduring growth.

Challenges of a Declining Active Client Base for SFIX

The dwindling active client base over the past eight quarters has raised significant concerns and is the primary factor behind the company’s revenue decline. In the third quarter of fiscal 2024, the number of active clients engaged in ongoing operations plummeted to 2,633,000, marking a 20% year-over-year decrease.

Consequently, the company witnessed a 15.8% revenue dip in the fiscal third quarter. This persistent revenue decline signals ongoing struggles in client retention and acquisition, potentially pointing to deeper issues related to product appeal or intensified market competition.

Final Thoughts

Investors may find SFIX stock appealing due to its robust recovery trajectory, fueled by innovative AI-driven inventory management and pricing strategies that have significantly bolstered efficiency, margins, and client engagement.

Despite challenges in the active client base, the stock’s value proposition shines through its low price-to-sales ratio, outperforming industry benchmarks, and displaying robust price stability according to technical indicators. This positions SFIX as an attractive choice for those interested in a company leveraging advanced analytics for growth. Stitch Fix’s emphasis on operational efficiency and profitability further enhances its investment allure. The company currently carries a Zacks Rank #3 (Hold).

Highlighted Stock Picks

Some noteworthy alternatives include Boot Barn Holdings, Inc. BOOT, Abercrombie & Fitch Co. ANF, and Steven

Madden, Ltd. SHOO.

Boot Barn operates as a lifestyle retail chain specializing in western and work-related footwear, apparel, and accessories. It currently boasts a Zacks Rank #1 (Strong Buy).

The Zacks Consensus Estimate for Boot Barn’s fiscal 2025 earnings and sales indicates growth of 8.9% and 10.7%, respectively, from the fiscal 2023 figures. BOOT has a trailing four-quarter average earnings surprise of 7.1%.

Abercrombie is a specialty retailer of premium, high-quality casual apparel. It currently holds a Zacks Rank of 1. ANF delivered a 16.8% earnings surprise in the latest reported quarter. Consensus estimates for Abercrombie’s fiscal 2025 earnings and sales point to growth of 61% and 12.6%, respectively, from the fiscal 2024 levels. ANF has a trailing four-quarter average earnings surprise of 28%.

Steven Madden designs, sources, markets, and sells fashion-forward name-brand and private-label footwear. It presently carries a Zacks Rank of 2 (Buy). The Zacks Consensus Estimate for Steven Madden’s 2024 earnings and sales indicates growth of 6.9% and 12.6%, respectively, from the year-ago actuals. SHOO has a trailing four-quarter average earnings surprise of 9.5%.