With a year-to-date gain of just over 12%, Alphabet (GOOG) (GOOGL) finds itself as an underwhelming member of the “Magnificent 7” cohort, failing to keep pace with the S&P 500 Index. A recent court ruling suggesting a monopoly in the online search market has cast a shadow over the company’s outlook, fueling speculative chatter about potential breakup scenarios in tech giant discussions. Is now the moment to embrace that recklessly seductive inclination and plunge into Alphabet shares for the fourth quarter? Allow us to dissect this tantalizing inquiry within the confines of this exposition.

GOOG Stock Projection

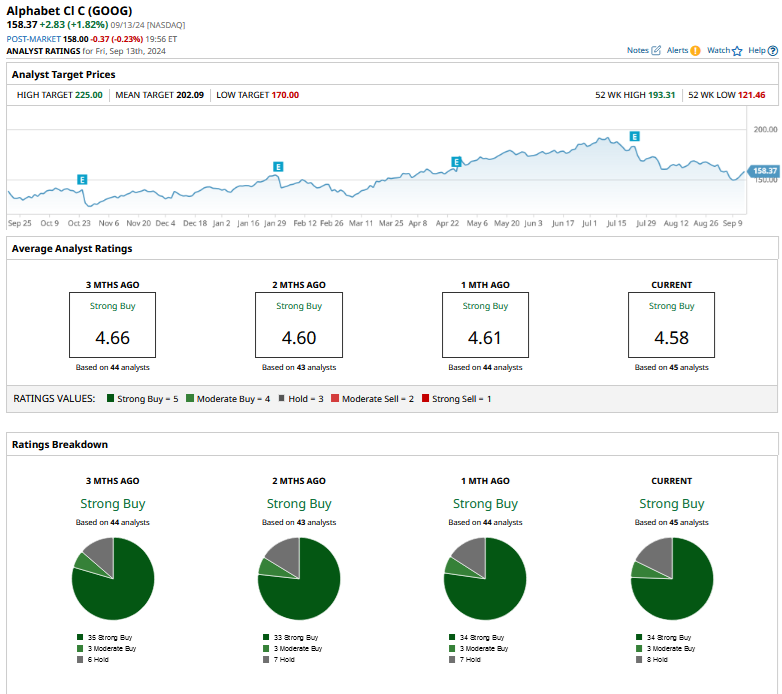

Though GOOG retains a “Strong Buy” consensus rating from analysts, boasting a mean target price of $202.09 that stands 27.1% above Monday’s closing figures, a sense of caution pervades certain corners of the analytical domain.

Presently, 82% of analysts maintain either a “Strong Buy” or “Moderate Buy” stance on Alphabet, a slight retreat from the 86% consensus three months prior. Notably, Rosenblatt, Bernstein, and Loop Capital have recently demoted GOOG from a “buy” to a “neutral” status, with Phillip Securities favoring a “buy” label in recent quarterly evaluations. Reflecting the prevailing sentiments, Evercore ISI adjusted Alphabet’s target price to a diminished $200 from $225 at the week’s inception, despite reaffirming its “overweight” endorsement.

The Crucial Hurdles Before Alphabet

Undoubtedly, Alphabet finds itself trailing market benchmarks for valid reasons, grappling with a myriad of challenges.

Foremost, the specter of regulatory perils looms ominously, with Bernstein projecting potential litigations amounting to $100 billion from aggrieved advertisers. In the current climate of heightened oversight, Bernstein’s Mark Shmulik suggests a constrained trajectory for Google’s future strategies.

Moreover, the looming possibility of a structural disassembly at the hands of regulators threatens Alphabet’s operational integrity, while formidable competition from the likes of Amazon (AMZN) poses a grave threat to its core advertising domain. As entities such as Uber (UBER), Disney (DIS), and Netflix (NFLX) increasingly pivot towards advertisement ventures, Alphabet faces an increasingly crowded arena for advertising revenue.

Lastly, the disruptive force of artificial intelligence propels uncertainty into the online search landscape, with Google’s enduring supremacy at stake. Though Alphabet has stepped up its AI initiatives post-initial missteps, its premier position remains precariously exposed. The tumultuous race lies firmly within Alphabet’s realm to either seize or forfeit.

The Virtue of Greed: Acquiring Alphabet Shares

Facing formidable risks notwithstanding, Alphabet’s quandaries warrant a nuanced assessment. Currently trading at a forward price-to-earnings (P/E) ratio of 20.4x – the most modest among the Magnificent 7 ensemble – Alphabet’s valuation trails the average S&P 500 constituent.

Unlike the prevailing trend of inflated tech valuations, Alphabet represents an outlier, flaunting a discounted stance in relation to its historical valuation thresholds. This divergence should not be understated, offering a potential harbinger of favorable prospects amidst a sea of profligate tech assessments.

Add to this the underappreciated assets nestled within Alphabet’s inventory – like the perennially popular YouTube platform. Unceasingly the dominant force in the U.S. streaming domain as per Nielsen data, YouTube holds untapped potential for monetization, particularly through premium subscriptions.

Further, the Waymo autonomous driving unit, recently joining forces with Uber to introduce driverless ride-hailing services in Atlanta and Austin, conceals a reservoir of promising growth. The burgeoning Cloud division stands as another bastion of expansion, notably clocking quarterly revenues of $10 billion in Q2, along with an inaugural operating profit of $1 billion.

Cognizant of the palpable regulatory specter, the calculated risk-inclined investor may discern an alluring opportunity in Alphabet’s current offering. While the immediate volatility from regulatory debates will persist, the panoramic horizon portends fruitful returns for the discerning investor embracing Alphabet’s latent potential.