U.S. legacy automaker General Motors GM recently hosted its much-anticipated Investor Day, shedding light on its ongoing transformation and future prospects. The company showcased significant advancements in electric vehicle (EV) technology and cost efficiencies, laying a strong foundation for the long term. However, while GM rides the waves of progress, it faces short-term challenges such as slow EV adoption rates and mounting costs, keeping investors on their toes. As shareholders mull over their next move with GM stock, dissecting the insights from the Investor Day becomes paramount.

Insights Unveiled at GM Investor Day

Farewell Ultium: A Branding Evolution

One of the pivotal announcements during the Investor Day was GM’s decision to bid goodbye to the “Ultium” branding for its EV batteries and associated technology. The move came as a surprise, considering GM’s extensive marketing efforts in promoting the Ultium brand as the linchpin of its EV transformation. However, GM’s CEO Mary Barra emphasized that while the name switch took place, the core technology and battery advancements would remain integral to GM’s trajectory.

This strategic shift signifies a pivot in GM’s EV strategy, amplifying its focus on product performance and cost efficiency over flashy branding gimmicks.

Charging Ahead: Investing in Battery Innovation

Highlighting its commitment to EVs, GM unveiled plans to establish a battery cell development center at its Global Technical Center in Warren, MI. Although the project is projected to commence before 2027, this move underscores GM’s unwavering dedication to cementing its position as a frontrunner in battery technology.

The development center is poised to play a pivotal role in GM’s quest to drive down battery costs, a critical component in enhancing the affordability and profitability of EVs. Executives underscored GM’s favorable trajectory in reducing battery costs, especially with the ramping up of production at its Ultium Cells plants.

Shifting Gears: Anticipating EV Profitability

GM provided an optimistic forecast, suggesting that its EV losses have likely reached their peak. While stopping short of declaring its EV business profitable by 2025, GM anticipates slashing EV losses by $2 billion to $4 billion by 2025. The surge will be primarily driven by enhancements in battery production efficiency and economies of scale. GM sets its sights on attaining positive variable profit on its EVs by the conclusion of 2024, sans fixed costs – a notable achievement for the automotive titan.

Nevertheless, GM adopted a cautious stance on its long-term profitability targets for EVs, including its earlier aim of achieving mid-single-digit EV margins by 2025. Investors are advised to monitor GM’s progress while staying alert to the hurdles entailed in securing profitability across its broader EV portfolio.

Speed Bumps Ahead: Variable EV Production Targets

GM revised its EV production forecasts downwards from previous estimates. In June, the company scaled back its North American EV output objective from a range of up to 300,000 units to a span of 200,000 to 250,000 by 2023. GM affirmed that it remains on track to meet the lower end of this spectrum, reflecting a tepid consumer uptake of EVs.

This decelerated ramp-up, coupled with GM’s decision to postpone the reopening of its Orion Assembly plant until mid-2026, underscores the persisting challenges in the EV market. GM, akin to numerous automakers, grapples with subdued demand for EVs, cost concerns, and amplified competition, particularly from Chinese automakers.

Powerful Performer: Thriving in Gas-Driven Terrain

GM continues to excel in its traditional gas and diesel-powered vehicle domains. CEO Mary Barra divulged plans to introduce eight new or revamped gasoline-fueled SUVs in North America over the next year. These vehicles hold paramount importance in GM’s playbook, furnishing a steady influx of cash as the company charts its course towards electrification.

With U.S. consumers heavily relying on gasoline-powered trucks and SUVs, GM stands well-positioned to harness the demand in this segment while navigating its transition to electrification.

Challenges on the Horizon: Tackling the Chinese Conundrum

GM’s fortunes in China, once a profit powerhouse, have dwindled in recent times. The automaker reported a $210 million loss in the region during the initial two quarters of the year, primarily attributable to fierce competition from local and international players. During the latest earnings call, Barra cautioned that the remainder of the year might prove arduous, with prevailing headwinds showing no signs of abating.

While the CEO assured investors of GM’s initiatives to restructure its operations in China, details regarding the revamping efforts remain scant. While the focus lies on depleting inventories and amplifying sales, hurdles persist, especially with local rivals intensifying the production of more economical EVs.

GM Stock Performance and Valuation Synopsis

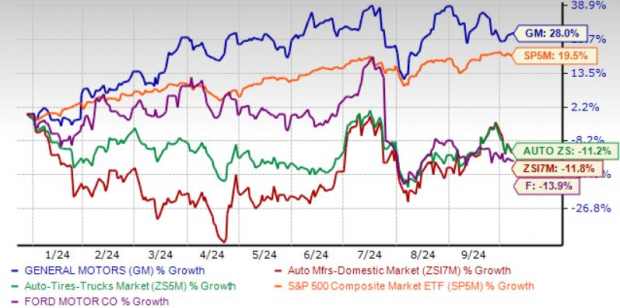

Year to date, GM stock has surged by an impressive 28%, outshining both the broader market and industry counterparts like Ford F, which witnessed a 14% decline over the equivalent period. Currently hovering near its 52-week pinnacle of $50.50, GM’s stock trades in the vicinity of $46.

Year-to-Date Price Trends

Image Source: Zacks Investment Research

From a valuation perspective, GM appears marginally pricier compared to Ford. GM trades at a forward sales multiple of 0.29X, while F’s forward sales multiple rests at 0.25X.

Image Source: Zacks Investment Research

GM’s Immediate Hurdles Amidst Long-Term Potential

GM has been delivering robust financial results, surpassing earnings projections in each of the past four quarters.

Image Source: Zacks Investment Research

Find the latest earnings estimates and surprises on Zacks Earnings Calendar.

While GM holds promising potentials in the long run, the near term presents several hurdles. GM foresees a pricing headwind of 1-1.5% year over year in the latter half of 2024, which could pose challenges to profitability. Additionally, GM projects around $1 billion in costs for the remaining period.

The Road Ahead: General Motors Navigating Challenges

Drops in Revenue and Rising Costs

General Motors (GM) faces a bumpy road ahead as its revenue takes a hit and costs soar, fueled by aggressive marketing spending and surging commodity prices, notably copper and aluminum. The self-driving division, Cruise, is also bleeding money, with projections indicating potential losses of up to $2 billion by 2025, according to GM’s chief financial officer, Paul Jacobson. The confluence of these factors, accompanied by hurdles in the Chinese market, might cast a shadow over GM’s stock performance in the near term.

Opportunity Amid Volatility

For investors eyeing short-term gains, the current scenario presents a window to capitalize on profits, particularly as GM’s stock approaches recent highs. However, prospective shareholders must tread cautiously, considering the looming challenges that could sway the stock price.

Long-Term Prospects Look Promising

Despite the short-term headwinds, GM stands tall as a reliable choice for long-term investors. Bolstered by a robust portfolio of traditional vehicles and an evolving electric vehicle (EV) strategy, the company is well-positioned for sustained expansion. GM’s concerted efforts to slash costs and ramp up EV production are indicative of its commitment to delivering enduring value over an extended period.

Nevertheless, the path may not be without hurdles for short-term investors, with GM’s stock having already witnessed substantial growth this year. As challenges like escalating expenses, pricing pressures, and delayed EV proliferation loom on the horizon, those seeking quick returns might contemplate seizing gains ahead of GM’s third-quarter earnings announcement on October 22.

Current Zacks data peg General Motors at a Rank #4 (Sell), accentuating the caution investors should exercise in the current landscape.