Following the announcement of exceeding both top and bottom line projections for its fiscal second quarter, Deere & Company’s DEstock witnessed a 5% decline during Thursday’s trading session. The drop ensued after the company revised its fiscal 2024 net income guidance downwards.

However, as a trailblazer and the leading player in the manufactured agricultural equipment sector, investors find themselves pondering whether it’s opportune to seize the moment and buy the dip in Deere’s stock, given its robust historical track record.

Deep Dive into Q2 Financial Performance

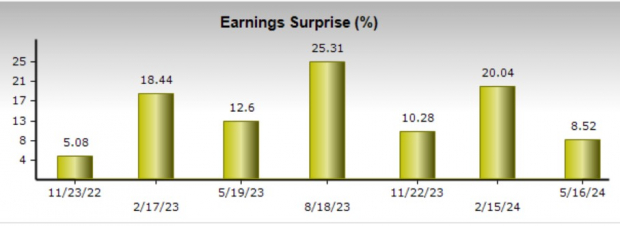

Deere’s Q2 posted a net income of $2.37 billion or $8.53 per share, outperforming the Zacks Consensus of $7.86 a share by 8%. On the revenue front, Q2 sales of $13.61 billion exceeded estimates of $13.25 billion by 2%.

Comparing year over year, Q2 earnings witnessed an 11% decrease from $9.65 per share in the corresponding quarter, attributed to higher operating costs, while sales saw a 15% drop due to reduced volumes. Despite this, Deere has surpassed earnings expectations for seven consecutive quarters and exceeded sales estimates for eight straight quarters.

Image Source: Zacks Investment Research

Guidance & Outlook

The momentum from Deere’s consistent outperformance was slightly dampened by its reduced target for fiscal 2024 net income, now anticipated at $7 billion, down from the previously provided guidance ranging between $7.5-$7.75 billion in February.

This decrease is primarily due to an expected 15% decline in the large agriculture segment in the U.S. and Canada, with projections indicating a 20% downturn in the small agriculture market and turf sales.

As per Zacks estimates, Deere’s FY24 EPS is forecasted to decrease by 21% to $27.39 compared to $34.63 per share last year. Total sales are now predicted to witness a 15% decline to $47.19 billion.

Analyzing Deere’s Past Performance & Market Value

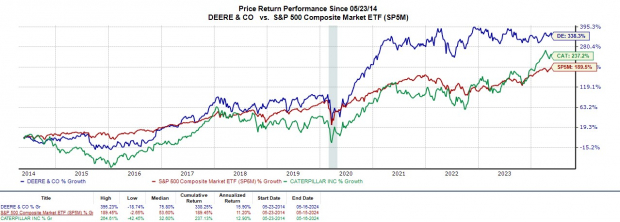

Deere’s stock is currently down 1% year to date but has enjoyed a 7% increase over the last year, albeit trailing the S&P 500’s 28% rise and notably lagging behind construction equipment behemoth Caterpillar’s CAT 65% surge. Nevertheless, over the past five years, Deere’s 192% rise has slightly outperformed Caterpillar’s 186% growth and significantly surpassed the S&P 500’s 89% increase.

Furthermore, over the last decade, Deere’s stock has skyrocketed by 338%, impressively eclipsing Caterpillar’s 237% increase and the benchmark index’s 189% climb.

Image Source: Zacks Investment Research

Currently priced at $394, Deere’s stock is trading at 15.1 times forward earnings, slightly below its five-year median of 16.1 times and well under the high of 33.1 times. It also presents a substantial discount compared to the S&P 500’s 22.2 times and is closely aligned with Caterpillar’s 16.5 times.

Image Source: Zacks Investment Research

Wrapping it Up

Maintaining a Zacks Rank #3 (Hold), Deere’s stock might present promising buying opportunities amidst the slowdown in agricultural-linked activities. The company’s reasonable valuation and strong historical performance hint that long-term investors may still find value at current levels.

We’re not kidding.

Several years ago, we shocked our members by offering them 30-day access to all our picks for the total sum of only $1. No obligation to spend another cent.

Thousands have taken advantage of this opportunity. Thousands did not – they thought there must be a catch. Yes, we do have a reason. We want you to get acquainted with our portfolio services like Surprise Trader, Stocks Under $10, Technology Innovators, and more, that closed 228 positions with double- and triple-digit gains in 2023 alone.

Deere & Company (DE) : Free Stock Analysis Report

Caterpillar Inc. (CAT) : Free Stock Analysis Report