As the stock price of Advanced Micro Devices (NASDAQ: AMD) took a dip from its lofty heights in early March, plunging by almost 15%, investors are now faced with a tantalizing opportunity. The allure of AMD as an AI stock has been on the rise, propelling its valuation to lofty levels. However, the recent market correction has cast a shadow over its price tag, creating uncertainty among investors — should they jump in or exercise caution?

An Overview of AMD’s Current Position

Despite the recent retreat, AMD’s stock price has witnessed an impressive 85% surge over the last year. This spike can largely be attributed to the heightened interest in its AI chip lineup, particularly the Instinct MI300 Series Accelerators. Although Nvidia (NASDAQ: NVDA) dominates a significant chunk of this market, industry projections suggest a robust compound annual growth rate of 38% until 2030 for AI chips, allowing AMD to thrive despite holding a modest market share.

The financials stand as a testament to this resurgence. Revenue in the fourth quarter of 2023 experienced a 10% year-over-year boost, reaching $6.2 billion. Notably, the data center division, inclusive of AI chips and contributing $2.3 billion to the revenue stream, witnessed a substantial 38% uptick from the prior year.

Undeniably, AMD’s other business segments have not lagged behind. The client-side business marked the highest growth, with a 62% surge in fourth-quarter revenue to $1.5 billion. While sectors like gaming and embedded segments faced declines, they did not manage to derail AMD’s recovery in the fourth quarter.

Looking forward, AMD refrained from offering a full-year guidance for 2024. Nevertheless, industry analysts foresee a 23% revenue escalation this year, followed by a 26% surge in 2025. These projections are poised to propel net income to lofty heights, painting a bullish trajectory for the stock’s price over the long haul.

The Challenges Plaguing AMD

Amid the triumph, AMD has not emerged unscathed from challenges. The results for full-year 2023 mirror the cyclic downturn in the overall industry, witnessing a 4% decline in revenue to $23 billion compared to the previous year. During this period, data center and embedded segments emerged as the lone bright spots amid the gloom.

This decline significantly dented the operating income, with a mere $4.3 million net income leading to a sobering 22% dip in adjusted net income.

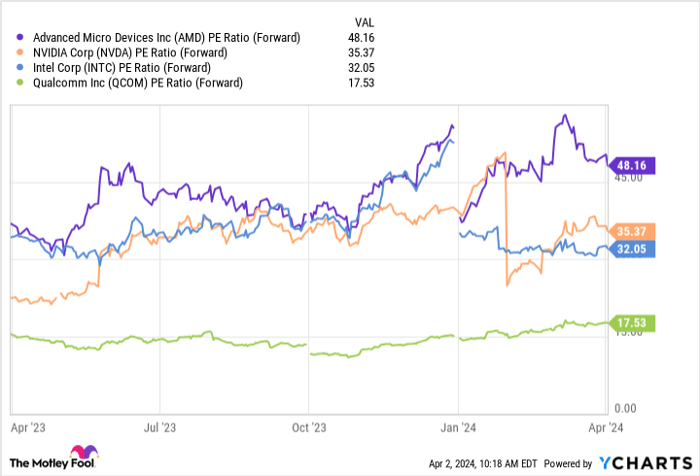

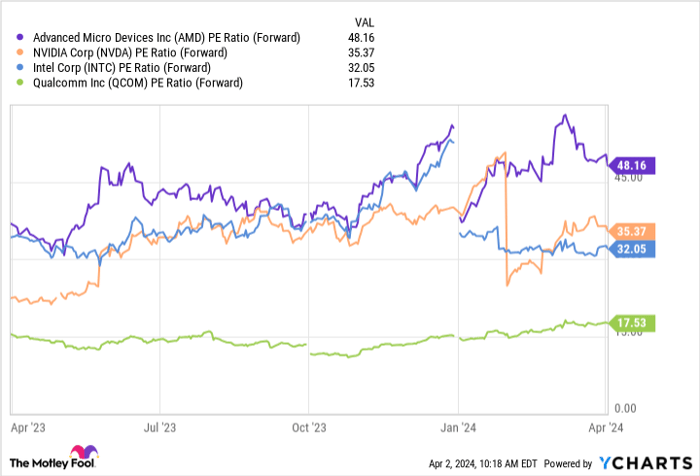

Delving deeper into its financial metrics, the price-to-earnings (P/E) ratio stands at an eye-watering approximately 350, largely reflective of the profit slump rather than a genuine valuation metric. Despite a more palatable forward P/E ratio of 48, the stock still appears pricey when juxtaposed against competitors like Intel (NASDAQ: INTC) and Qualcomm (NASDAQ: QCOM), both of which have made strides in developing AI-ready chips. This valuation dissonance, compounded by a forward P/E ratio significantly higher than Nvidia’s, might exert pressure, tempering gains or potentially reversing the same over time.

AMD PE ratio (forward) data by YCharts.

Evaluating the Correction: To Buy or Not to Buy?

Despite the staggering growth in the AI chip domain, AMD emerges as an enticing buy. With the burgeoning demand for these chips, it is poised to witness a substantial uptick in revenue and income over time, a trend that is already in motion as evidenced by the fourth-quarter surge.

While the stock may seem steeply priced, especially in comparison to Nvidia and other emerging AI competitors, the expected explosion in the AI chip market indicates a rising tide that could lift all firms. Given this market boon coupled with AMD’s diverse business portfolio, the stock’s recent pullback appears more as a buying opportunity than a red flag warning investors away from this semiconductor giant.