“Tokenization,” particularly of “real world assets,” or RWAs, has recently been touted as the next big thing in crypto. Most people do not make the connection that this trend is just another form of security tokens, a term you may not have heard since 2018 (for good reason).

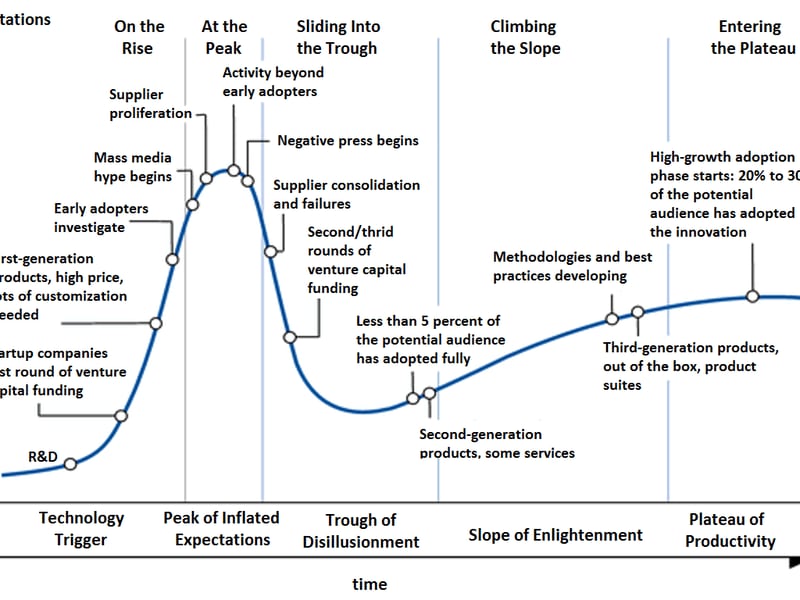

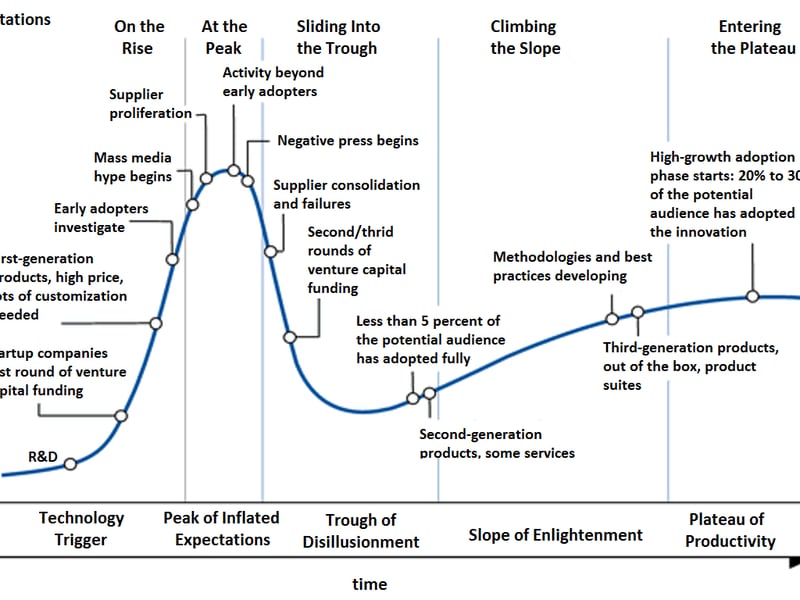

The people hyping tokenization are mostly wrong. But their heart is in the right place. It’s no one’s fault that something becomes trendy, but if “security tokens,” “tokenization” and RWAs are all part of the same technological continuum, and if the Gartner “Hype Cycle” is right, there will likely be another bust soon enough.

Many of the current promoters of tokenization are refugees from the former hype-cycle champion, decentralized finance, otherwise known as DeFi.

While influential TradFi influencers and CEOs see tokenization as a natural evolution in finance — (for instance, BlackRock CEO Larry Fink said the recent launch of bitcoin ETFs were the “first step” towards everything going on-chain) — the tokenization of “every financial asset” is much more complicated, and largely misunderstood by both proponents and detractors.

The Tokenization of the RWA assets industry is beginning its eighth year, having started in late 2017. My firm, Vertalo, launched one of the first fully compliant, Reg D/S equity tokenizations in March 2018. The challenges that we encountered — too many to recount here — led us to pivot from our original role as an issuer of tokenized equity to a “picks and shovels” enterprise software company with an aim to “connect and enable the digital asset ecosystem.”

Since that time, we saw the expansion, and subsequent massive contraction, of non-fungible tokens (NFT) and DeFi. NFTs and DeFi were easier and more end-user friendly applications of tokenization technology. In the case of NFTs, you could buy computer-generated art that would be represented by a tradeable token on easily-accessible marketplaces like OpenSea.

If you asked me to map the progress of NFTs to Gartner’s Hype Cycle, I would place them post-peak and sliding fast through the “trough of disillusionment.” For instance, OpenSea investor Coatue marked down of their $120 million investment to $13 million, based on the exchange’s diminishing fortunes.

Likewise, the formerly red-hot DeFi market has demonstrated its own cooling — with many projects now seemingly rebranding and refocusing on real-world assets. This includes DeFi titans MakerDAO and Aave.

Teams touting their RWA cred now point to large, traditional financial institutions as clients or partners, which makes sense since many DeFi founders cut their teeth at Stanford or Wharton Business School before working at Wall Street banks.

Bored by quant jobs supporting bond salesmen and equity traders, but enamored with the volatility and work-life balance that came with decentralization, the DeFi movement is well-acquainted with the world (and money) of global finance, but less enamored with its rules, regulations and rigor.

As astute observers of trends, smart DeFi founders and their engineer-mathematicians saw the writing on the wall and exited the governance token-airdrop game in 2022 and started re-tooling their marketing and strategy to create the “new, new thing,” i.e. tokenization. The result? A mass migration and adoption of the moniker RWA and a swift flight from anything that looked like a copy-paste rug pull, a signature move and risk in the anon-loving DeFi world of 2020-22.

The fact that the assets and collateral typically under management in most of these RWA projects are largely stablecoins, and not actual hard assets, doesn’t appear to be a problem.

Tokenization is not a quiet riot. If you map the current RWA market to the hype cycle, it probably would land right at “Supplier Proliferation” today. Everyone wants to be in the RWA business now, and they want to get into it as fast as they can.

Tokenization of RWA is actually a great idea. Today the ownership of most private assets — the target asset class for RWA — is tracked on spreadsheets and centralized databases. If an asset is restricted from being sold — like a public stock, bearer bond, or cryptocurrency — there is little reason to invest in technology that makes it easier to sell. The antiquated data management infrastructure found in private markets is a function of inertia.

And according to RWA proponents, tokenization fixes this.

The Unvarnished Truth

There’s some truth to this little white lie, but the absolute truth is while tokenization, by itself, does not solve liquidity or legality problems when it comes to private assets, it also introduces new challenges. RWA tokenization advocates conveniently side-step this issue, and it’s easy for them to do so since most of the so-called real world assets being tokenized are simple debt or collateral instruments that are not held to the same compliance and reporting standards as regulated securities.

In reality, most RWA projects are engaging in an old process called “rehypothecation,” where the collateral is itself lightly regulated cryptocurrency and the product is a form of a loan. That’s why almost all RWA projects tout money-market type yield as their drawing card. Just don’t look at the quality of the collateral too closely.

Borrowing and lending is a big business, and so I would not count out the future and long term success of tokenization. But saying you are bringing real world assets on-chain is not accurate. It is simply the collateralization of crypto assets, represented by a token. And tokenization is just one piece, an important one, of the puzzle.

When Larry Fink and Jamie Dimon talk about the tokenization of “every financial asset,” they are not talking about crypto-collateral RWAs, they are actually talking about tokenizing real estate and private equity, and eventually public equities. This will not be accomplished merely with smart contracts.

A Insider’s Perspective

After spending more than seven years building a digital transfer agent and tokenization platform that has tokenized almost four billion units representing interests in almost 100 companies, the reality of mass financial asset tokenization is much more complicated.

First of all, tokenization is a relatively simple and minor part of the process. Tokenization is a commodity business and hundreds of companies can tokenize assets. Tokenization by itself is not a very profitable business, and as a business model, tokenization is a competitive race to the bottom when it comes to fees. With so many suppliers offering the same thing, it’s going to become a commodity really fast.

Secondly, but far more important, there are fiduciary responsibilities when it comes to tokenizing and transferring RWAs. That’s where the hard part, the ledger, comes in.

Distributed ledgers offer real benefits for tokenizing financial assets by offering immutability, auditability and trustability. This creates the basis for provable ownership, and enables an error-free record of all transactions, instantly. Without this, there will be revolution in finance using tokens.

The ledger creates the trust that will enable finance professionals and their clients to get behind the words of Larry Fink and Jamie Dimon, but do so in a way that engenders more adoption than the tricky and technical world of DeFi and crypto.

So before you start riding the hype-cycle, look at what’s come before, and what has to happen next. Don’t end up riding the wrong part of the cycle, or else you’ll land on NFT version two.