Implied Volatility and Earnings Anticipation

Earnings season brings a flurry of excitement and anticipation as investors eagerly await the financial performance of big-name companies, ranging from banks to tech giants. This week, the spotlight shines on Taiwan Semiconductor (TSM), Bank of America (BAC), United Airlines (UAL), Netflix (NFLX), Goldman Sachs (GS), Johnson & Johnson (JNJ), and Morgan Stanley (MS), among others.

Implied Volatility Dynamics

Before a company releases its earnings report, implied volatility tends to soar, reflecting the uncertainty surrounding the impending financial disclosure. Speculators and hedgers drive up demand for the company’s options, leading to an increase in implied volatility and subsequently, option prices.

Post-earnings announcement, implied volatility typically recedes back to normal levels, marking a return to relative stability in the options market.

To gauge the expected movement of these stocks, traders can calculate the anticipated range by summing up the prices of the at-the-money put and call options following the earnings date. While this method offers a rough estimate, it provides a reasonable guide for market behavior.

Weekly Earnings Volatility Estimates

Monday

GS – 3.8%

BLK – 3.3%

Tuesday

UNH – 4.7%

BAC – 3.9%

MS – 3.8%

SCHW – 5.1%

PNC – 4.4%

Option Trading Strategies

Option traders can leverage these anticipated moves to create strategic positions. Bearish traders may consider bear call spreads beyond the anticipated range, while bullish traders can explore bull put spreads outside the expected range or opt for naked puts for a higher risk tolerance.

Neutral traders might find iron condors appealing, with a recommendation to place short strikes outside the predicted range for earnings plays.

When engaging in options trading during earnings season, it is prudent to adhere to risk-defined strategies and maintain modest position sizes. It is advisable that any full loss on a trade should not exceed 1-3% of an investor’s overall portfolio.

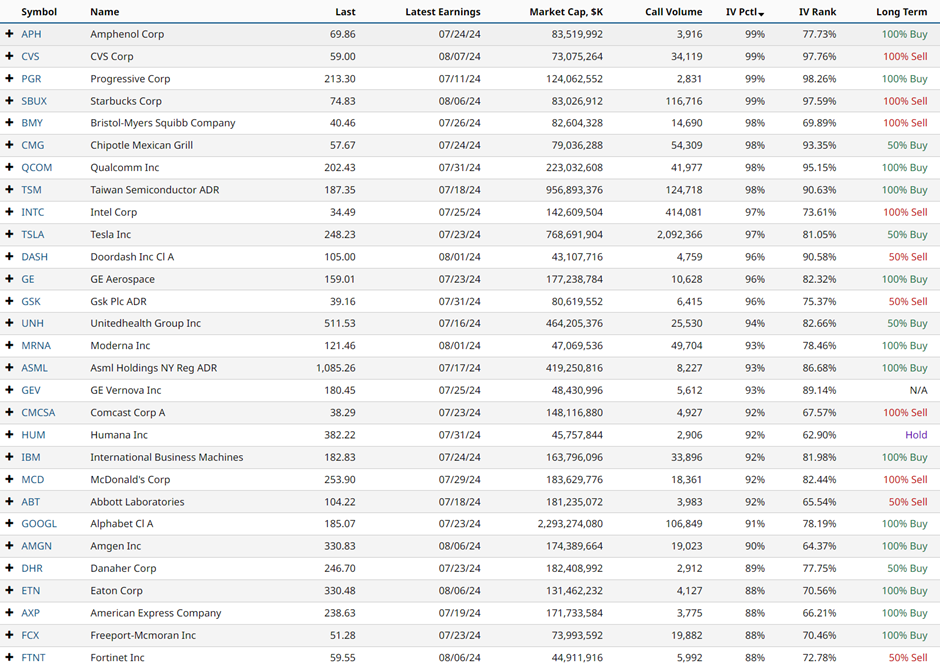

Understanding High Implied Volatility Stocks

Investors seeking stocks with elevated implied volatility can utilize screening tools like Barchart’s Stock Screener. Setting filters for total call volume, market capitalization, and IV percentile enables traders to identify stocks with significant implied volatility levels, aiding in decision-making.

Previous Week’s Earnings Performance

Recapping the prior week, actual versus anticipated stock movements illustrate the dynamic nature of the market:

CAG -1.5% vs 4.5% expected

DAL -4.0% vs 6.3% expected

Unusual Options Activity

Unusual options activity in stocks like RIVN, RKT, KMI, AA, PFE, and TSLA captured attention last week within the investment community. This unique activity highlights potential opportunities and risks in the market.

It is crucial to acknowledge the inherent risks associated with options trading, emphasizing the possibility of a complete loss of investment. This information serves an educational purpose and should not be construed as a trading recommendation. Always conduct thorough due diligence and seek advice from a financial advisor before making investment decisions.