Quintessentially known for steering the NFL’s Carolina Panthers and MLS’s Charlotte FC, David Tepper crafted his monetary empire through the inception of Appaloosa Management, a sweeping hedge fund under his watchful eye. With a net worth hovering around $20 billion, Tepper commands a spot among the world’s top 100 wealthiest individuals. It goes without saying that he has sculpted a niche for himself in the realm of investments.

Given Tepper’s triumphant journey, it is hardly surprising that both seasoned and amateur investors seek solace in his strategical investments to glean insights. Although the risk appetites and investment objectives of the ordinary investor may diverge from those at billionaire hedge funds, there’s no harm in drawing inspiration from such financial maestros.

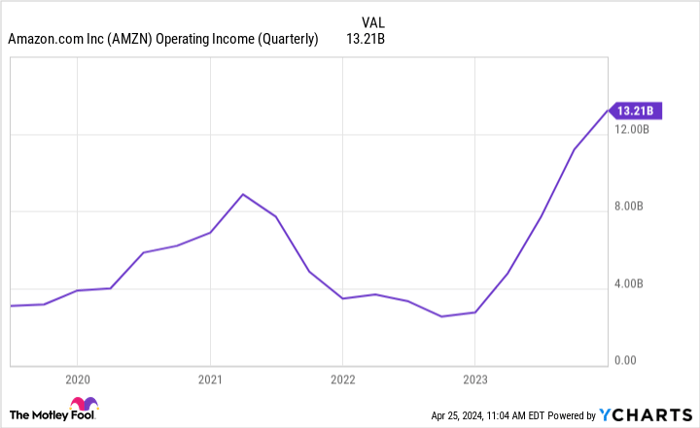

Amazon – The E-Commerce Behemoth

Amazon (NASDAQ: AMZN) surged into the limelight anchored by its e-commerce arm, swiftly branching out to dominate various sectors. Initially operating at a loss, Amazon’s e-commerce unit has transitioned into a fertile ground for revenue generation, muffling critics with delightful operating profits. During the fourth quarter, Amazon’s North American division boasted approximately $6.5 billion in operational profits, representing a remarkable shift from the $240 million plunge in Q4 2022. Albeit the international segment’s $419 million loss, Amazon remains a profitable entity outside of its Amazon Web Services (AWS) domain.

Intriguingly, Amazon’s growth narrative hinges significantly on its cloud service, AWS. Despite a recent deceleration in AWS growth, a 13% year-over-year (YOY) uptick asserts its position as Amazon’s primary profit engine. Bundling a substantial chunk of the global cloud services market share at 31%, AWS overshadows Microsoft‘s (NASDAQ: MSFT) Azure at 24% and Alphabet’s Google Cloud at 11%.

Ambitiously spearheading into uncharted territories, Amazon’s $13.7 billion rendezvous with Whole Foods and profound strides in healthcare delineate a corporate essence unwilling to settle for the status quo.

Microsoft – Diversified Tech Royalty

Within the realm of tech enterprises, an expansive empire reigns supreme — Microsoft (NASDAQ: MSFT). Famed for its diversified portfolio, Microsoft’s well-orchestrated growth saga, supplemented by a surge in AI fervor, pitches a compelling narrative.

Embracing a strategic alliance with OpenAI and wielding exclusive rights to large language models (LLMs), Microsoft carves a path to fortify its dominance in the software realm. Ranging from Office Suite (Excel, Word, PowerPoint) to Azure and Teams, Microsoft’s omnipresence in the corporate universe is undeniable.

The abundance of corporate adherents imparts a longevity shield, insulating Microsoft from market upheavals. In the face of fiscal turmoil, consumers may dispense with new gadgets or online splurges, but severing ties with Office Suite, migrating data from the cloud, or switching from entrenched communication platforms like Teams proves a Herculean task.

Meta Platforms – The Cash Cow Connoisseur

Originating from the minds behind Facebook, Meta Platforms (NASDAQ: META) retains its stature as a cash cow craftsman, recording a lofty $36.5 billion in Q1 revenue, marking a 27% year-over-year upswing.

Boasting an average of 3.24 billion family daily active members in March 2024, Facebook’s allure to premier advertisers globally remains unwavering. Capitalizing on this appeal, Meta subtly elevated its family average revenue per individual from $9.47 in Q1 2023 to $11.20 in Q1 2024.

Despite a triumphant march in critical metrics, Meta’s stock journeyed south post its recent earnings release, nosediving up to 15% on that dreaded day. The impending surge in planned expenses, predominantly directed towards amping up its AI infrastructure, unveiled Meta’s blueprints to splurge between $35 billion and $40 billion this year — an upshift from the erstwhile $30 billion to $37 billion projection.

The Intriguing Case of Meta Platforms for Investors

Reassessing Meta Platforms’ Financial Strategy

A recent uptick in META’s capital expenditures has raised eyebrows among investors, with some expressing apprehension over the company’s spending plan. However, the reaction seems exaggerated, hinting at a potential overreaction in the market. Nonetheless, the silver lining shines through as META’s lower valuation presents a more enticing entry point for discerning investors seeking value.

A Glimpse into Meta’s Investment Appeal

Adding to the intrigue, investors are urged to take note of Meta’s newfound dividend offering, set at $0.50 per share. While the dividend yield may not be sufficient to entice income-focused investors, it acts as a sweetener that could foster patience among stakeholders as Meta juggles its ambitious AI endeavors.

Exploring the Amazon Investment Conundrum

On a different note, the question of whether to invest in Amazon looms large. Before diving into Amazon stock, one must weigh various considerations.