Artificial Intelligence (AI) prodigy Nvidia (NVDA), once a soaring star in the financial skies, faced a turbulent descent in market capitalization post the Q2 earnings stumble in late August. Nevertheless, NVDA has once again flexed its muscles, recording a 5% surge in the past week. Surpassing the $3 trillion milestone earlier this year, the future of this tech giant remains under scrutiny. My stance remains unwavering – NVDA’s shares are a beacon of hope due to its unquestionable AI dominance and the promise of exponential growth ahead.

NVDA’s Long-Term AI-Driven Growth Trajectory Remains Intact

Positioned for a prolonged period of expansion, NVDA boasts a star-studded clientele featuring the likes of Microsoft (MSFT), Alphabet (GOOGL), Meta (META), and Amazon (AMZN), each ramping up their AI capabilities. Beyond these industry leaders, Nvidia’s AI influence continues to proliferate across sectors, bolstering my optimism for NVDA shares. As enterprises globally clamor to integrate AI perks into their operations, Nvidia further solidifies its foothold through collaborations with industry luminaries.

Besides being the AI GPU processor kingpin, Nvidia offers a comprehensive end-to-end AI infrastructure that redefines productivity, a feat matched by few, if any, of its global AI counterparts.

NVDA Remains a One-Stop AI Powerhouse with Margin Growth

Driving my optimism is CEO Jensen Huang’s unwavering dedication to sculpting NVDA into an all-encompassing AI-driven data center juggernaut, enveloping hardware and software under the NVDA umbrella. This stratagem underpins NVDA’s ability to command premium prices, fueling consistent expansion in profit margins. Despite apprehensions surrounding NVDA’s remarkable revenue and margin proliferation, the expected moderation in growth from 217% in FY2024 to around 130% in 2025 still presents an impressive triple-digit figure.

Forecasts of robust chip demand spell future revenue upswings for NVDA, abating investor jitters and fortifying NVDA’s AI supremacy with an impenetrable competitive edge and unrivaled AI products and services.

A Discussion of Nvidia’s Impressive Quarterly Earnings

Augmenting its record, Nvidia unveiled another sterling Q2 performance on August 28, 2024, propelled by accelerated computing and the sustained allure of generative AI. Adjusted earnings per share of $0.68 eclipsed analysts’ predictions, showcasing a 152% surge from the prior year. The company registered a 122% year-over-year revenue spike, scaling $30.04 billion for the quarter ending July 31, outclassing market forecasts. Data Center revenues, NVDA’s crown jewel, soared 154% to $26.3 billion, while adjusted gross margins expanded by 5 percentage points to 75.1%.

Despite the stellar results, cautious guidance for the 3rd quarter led to a minor stock dip, with revenue forecasts slightly below expectations. Adjusted gross margins are anticipated to stabilize around 75%, a marginal decline from the Q2 figures.

NVDA’s Insider Selling Concerns are Over

Recent months witnessed insider selling casting a shadow on NVDA shares. CEO Jensen Huang’s sell-off in NVDA shares over multiple transactions from June to September raised eyebrows. However, it’s crucial to note that these sales were part of a pre-planned trading strategy formulated in March. Despite the substantial exits, Huang remains NVDA’s largest individual shareholder, with a stake of approximately 3.5% in the company.

NVDA Valuation Isn’t Expensive, Given Its Earnings Growth Prowess

Amid concerns of NVDA’s exorbitant run and slowing growth, the stock’s valuation may appear prohibitive to some investors. Contrarily, NVDA’s forward P/E ratio of about 43x (based on FY2025 earnings expectations) is comparably reasonable. This valuation stands at a slight discount to some industry peers, emphasizing NVDA’s overarching growth narrative and lucrative prospects in the burgeoning AI domain.

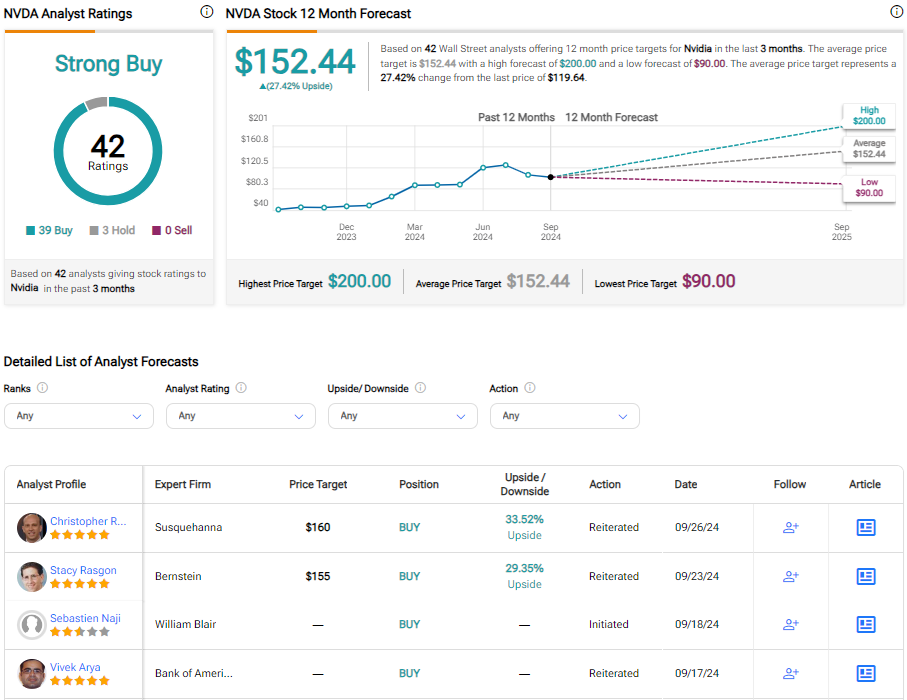

The consensus among analysts underscores NVDA’s potential, with a Strong Buy rating garnered from 39 Buys and three Holds, hinting at a significant upside potential based on the average stock target price of $152.44.

Conclusion: Consider NVDA Stock for Its Long-Term AI Potential

Despite recent wobbles, NVDA shares have soared nearly threefold over the past year compared to the Nasdaq 100’s modest 37% uptick. The post-earnings jitter for NVDA stock was predominantly fueled by profit-taking. Post hitting a slump near $100, NVDA appears poised for a rebound.

Though short-term market uncertainties may tether NVDA, prospective downticks should be viewed as lucrative entry points. NVDA’s enduring value is bolstered by the burgeoning AI sector, holding key promises for the discerning long-term investor.