Throughout its journey this year, NVIDIA Corporation NVDA has been a rollercoaster ride for investors, with shares skyrocketing over 100%. However, recent market turbulence stemming from reduced spending in the realm of artificial intelligence and NVIDIA’s quarterly results falling short of lofty expectations rattled the stock price.

Amidst these fluctuations, NVIDIA has unveiled a $50 billion stock buyback plan, designed to cater to investors seeking income. The question beckons – is this the opportune moment to engage in NVIDIA stock? Let’s delve into the details.

The Strategic Move: NVIDIA’s Share Repurchase Endeavor

While NVIDIA has maintained its quarterly dividends intact, the company has recently greenlit a fresh $50 billion share repurchase program. Not a stranger to stock buybacks, NVIDIA initiated a $25 billion repurchase plan in August 2023, subsequently reclaiming around $15.4 billion in stocks during the first half of fiscal 2025.

Having amassed significant cash flows, NVIDIA’s board of directors is in a comfortable position to engage in share repurchases. The new $50 billion stock buyback scheme stands as the third largest across the S&P 500 index. Apple Inc. AAPL and Alphabet Inc. GOOGL have also partaken in significant share repurchases, signaling a trend within the technology sector.

Decoding the Impact: NVIDIA’s Optimism and Market Dynamics

Share repurchases often indicate a robust and well-grounded corporate framework. By reducing the number of outstanding shares, this move augments the value of the remaining shares, thereby benefiting shareholders in the process.

Even though NVIDIA’s $50 billion stock buyback stands as a proportionally modest figure relative to its market capitalization, this strategic initiative underscores management’s optimism for NVIDIA’s future business endeavors.

Historical data also attests to the positive correlation between share buybacks and subsequent rises in share prices. Therefore, an upturn in NVIDIA shares in the long run is a plausible outcome.

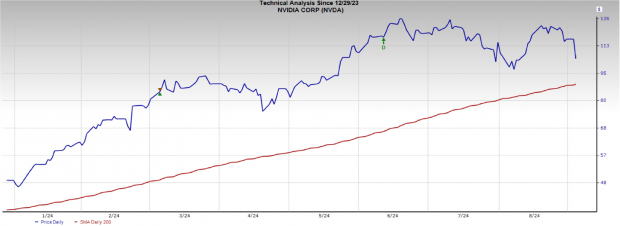

Fluctuations in NVIDIA’s market capitalization should not be viewed in isolation but rather as part of the broader tech sector’s landscape. The recent dip was influenced by discouraging economic data impacting the sector at large. NVIDIA’s resilience is evidenced by its consistent trading above the 200-day moving average (DMA) this year, a testament to its enduring uptrend.

Image Source: Zacks Investment Research

Strategic Imperatives: Factors Favoring NVIDIA’s Long-Term Growth

As the global leader in graphic processing units (GPUs), NVIDIA is primed for success. CEO Jensen Huang’s bullish stance on the migration of data centers from central processing units (CPUs) to GPUs, with a projected GPU market size of $1.4 trillion by 2034, underscores NVIDIA’s advantageous market positioning.

Further bolstered by its strong foothold in the burgeoning AI industry, anticipated to reach $1.3 trillion by 2030, NVIDIA’s trajectory appears promising. The imminent launch of the cutting-edge Blackwell AI chips, offering enhanced AI throughput compared to existing platforms, is set to dispel any lingering doubts.

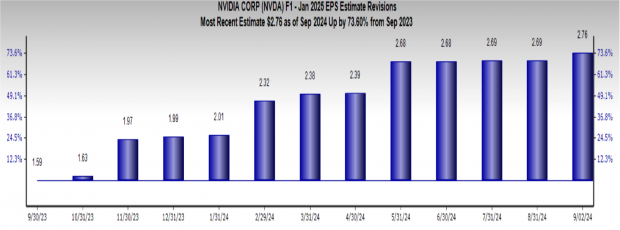

Focusing on diversification, NVIDIA’s foray into the expanding gaming and industrial metaverse segments adds another dimension to its growth narrative. The Zacks Consensus Estimate for NVIDIA’s earnings per share stands at $2.76, marking a substantial 73.6% increase compared to the previous year.

Image Source: Zacks Investment Research

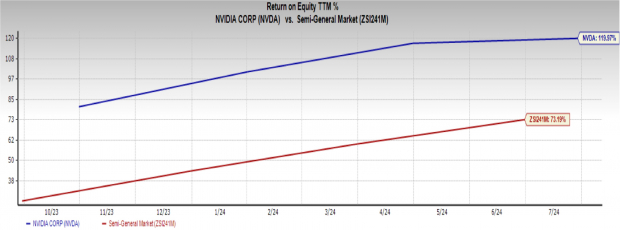

From a fundamental standpoint, NVIDIA’s robust profitability is evident through its exceptional return on equity (ROE), standing at nearly 120%, well above the industry average of 73.2%. An ROE exceeding 100% indicates a company’s vigorous performance and an optimal balance between net income and equity.

Image Source: Zacks Investment Research

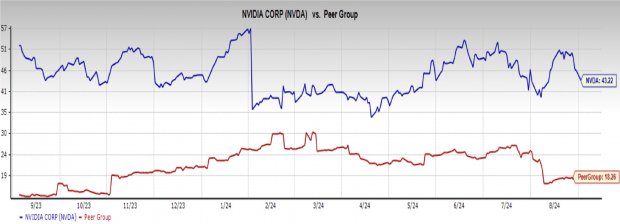

Striking a Balance: Evaluating NVIDIA’s Market Valuation

As investors navigate the proposition of investing in NVIDIA, the elevated pricing of NVIDIA stock warrants caution. The burgeoning demand for AI applications and NVIDIA’s dominance in the GPU market have contributed to the stock’s premium valuation.

With NVIDIA’s price/earnings ratio currently standing at 43.2X forward earnings, compared to a peer average of 18.2X, prospective investors should exercise prudence and wait for opportune entry points, capitalizing on market dips.

Image Source: Zacks Investment Research

For existing NVIDIA investors, maintaining their position is advisable given the company’s forward-looking vision in the AI sphere and its potential to spearhead technological advancements.