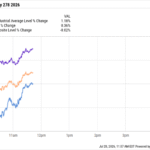

National Research Corporation NRC shares have surged 61.8% in the past year against the industry’s 19.8% decline. The company has outperformed other industry players, including Iron Mountain Incorporated IRM and Recruit Holdings Co., Ltd. RCRUY. Shares of Iron Mountain have rallied 38%, while Recruit Holdings stock has declined 15.5% in the same time frame. NRC benefits from strong recurring revenues, high retention, expanding AI-enabled platform adoption and cross-selling opportunities.

Image Source: Zacks Investment Research

A Key Look Into NRC’s Business Operations

NRC Health is a healthcare experience management company that focuses on helping healthcare organizations understand and improve the experiences of patients, consumers, clinicians, and employees through its Human Understanding approach. Over nearly 45 years, it has developed a comprehensive, AI-enabled platform that collects, analyzes and delivers real-time feedback from millions of healthcare consumers and professionals, enabling providers to strengthen relationships, improve outcomes and enhance loyalty. Its subscription-based solutions cover patient, consumer, employee and market experience, along with governance services that support healthcare leadership and strategy. By leveraging advanced data insights and continuous engagement across the care continuum, NRC Health helps organizations optimize operations, drive service improvements and deliver more personalized, human-centered care.

NRC Health’s Key Tailwinds

NRC Health benefits from a strong structural shift in the healthcare industry toward value-based care and patient-centric delivery models. As reimbursement increasingly depends on patient outcomes, satisfaction scores and engagement metrics, providers are prioritizing solutions that improve experience and loyalty. NRC’s platform directly addresses these needs by capturing and analyzing patient, consumer, and employee feedback in real time, enabling healthcare systems to enhance outcomes and reimbursement potential.

Another important driver is the company’s highly visible and recurring revenue model, built on subscription-based contracts. A significant portion of revenue is derived from renewable agreements, providing stability and predictability in cash flows. This is reinforced by strong retention levels and rising Total Recurring Contract Value, which has reached record highs and serves as a leading indicator of future revenues. Additionally, the ability to expand relationships through cross-selling and increased solution adoption within existing clients enables efficient organic growth with limited incremental acquisition costs.

The company is also gaining momentum from the increasing adoption of its integrated, AI-enabled platform. By combining patient experience, consumer insights, employee engagement, and governance solutions into a unified system, NRC delivers a differentiated and scalable offering. Continued investments in artificial intelligence — such as sentiment analysis, automated insights, and workflow tools — enhance decision-making and operational efficiency for healthcare providers.

Strong customer relationships and expanding partnerships with leading healthcare systems further support growth. NRC serves a large share of top U.S. health systems and continues to deepen engagement through broader solution adoption. Recent partnership expansions with Ann & Robert H. Lurie Children’s Hospital of Chicago and Piedmont highlight growing demand for integrated experience, reputation and market intelligence offerings. This established customer base not only strengthens retention but also creates opportunities for upselling and network-driven growth.

Lastly, improvements in execution and go-to-market strategy are contributing to better business momentum. The company has restructured its sales organization, enhanced customer success initiatives, and strengthened leadership to improve engagement and retention.

Challenges Persist for NRC’s Business

The company faces several headwinds, primarily stemming from its heavy reliance on renewable customer contracts, where non-renewals, pricing pressures, or reduced service scope could materially impact revenues. Intense competition from larger, better-resourced players and low barriers to entry increase pricing pressure and customer churn risks. Operational risks include dependence on high-quality data collection, third-party vendors and technology platforms, exposing the firm to disruptions, cybersecurity threats and system failures. Additionally, rapid technological shifts, including AI advancements, may erode competitive positioning, while talent retention challenges and rising costs could pressure margins.

NRC Health’s Valuation

The company is cheaply priced compared with the industry average. Currently, NRC is trading at 3.34X trailing 12-month EV/sales value, below the industry’s average of 6.27X. The metric remains lower than that of one of the company’s peers, Iron Mountain (7.24X), but is higher than that of Recruit Holdings (2.73X).

Image Source: Zacks Investment Research

Conclusion

Despite competitive pressures, contract renewal risks, and operational challenges, NRC Health remains poised for growth on the back of strong recurring revenues, growing AI-driven capabilities, and favorable industry shifts toward value-based, patient-centric care.

Strong fundamentals, coupled with NRC’s undervaluation, present a lucrative opportunity for investors to add the stock to their portfolio.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in the coming year. While not all picks can be winners, previous recommendations have soared +112%, +171%, +209% and +232%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>

Iron Mountain Incorporated (IRM) : Free Stock Analysis Report

National Research Corporation (NRC) : Free Stock Analysis Report

Recruit Holdings Co., Ltd. (RCRUY) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.