Just a year ago, the markets were recuperating from bearish conditions, and the speculative vibe around growth stocks was palpable. And now, here we stand in 2024, amidst a freshly minted bull market. The iconic S&P 500 recently achieved a record high, signaling the onset of a much-awaited era of optimism and prosperity.

Historically, bull markets have held sway longer than bear markets, offering extended periods of portfolio growth. To leverage this bullish temperament, investing in growth stocks stands to be a prudent move. These stocks tend to flourish during bull markets and times of economic resurgence. Here are the top growth stocks that warrant attention in 2024.

Image source: Getty Images.

1. Amazon’s Dominance in Growth Markets

Amazon (NASDAQ: AMZN) continues to reign as an ideal growth stock, straddling two high-growth domains: e-commerce and cloud computing. Amazon is also heavily investing in the burgeoning field of artificial intelligence (AI), a move that is bolstering its earnings trajectory.

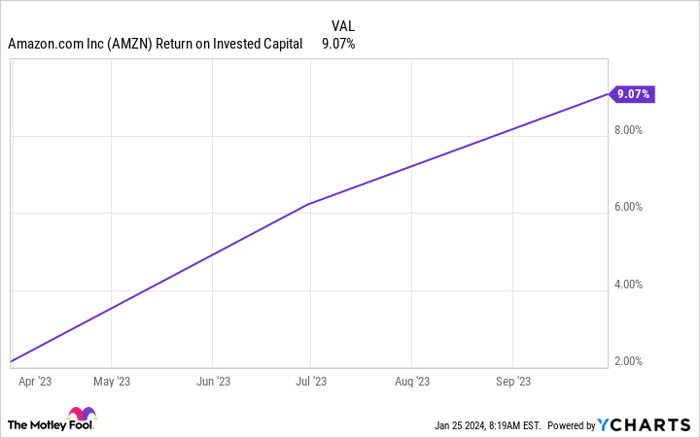

AI has not only amped up efficiency in Amazon’s operations, leading to cost reduction, but also provides AI tools to clients through its cloud computing arm, Amazon Web Services (AWS). The escalating demand in this domain augurs well for AWS’ revenue, a factor vital to Amazon’s profitability, as historically AWS has been a key profit driver. Amazon’s recent endeavors to revamp its cost structure are yielding results. In 2022, the company reported its first annual loss in about a decade. However, by early last year, Amazon was churning out quarterly net income gains and witnessing a turnaround in cash flow. The most recent quarter saw the company’s net income tripling and a significant increase in free cash flow to over $21 billion. Return on invested capital has also been on an upward trajectory over the past year.

AMZN Return on Invested Capital data by YCharts

Amazon’s efficiency enhancements across its fulfillment network are noteworthy, transitioning to a regional model from a national one in the U.S. The decreased delivery distances have improved Amazon’s “cost to serve,” with further potential for enhancements.

Despite Amazon’s stock surge last year, the scope for further growth is far from exhausted, making it poised to excel in this bullish market.

2. Carnival’s Spectacular Cruise Comeback

Carnival (NYSE: CCL) faced tumultuous times earlier in the pandemic when cruise operations came to a standstill. Nevertheless, the globe’s largest cruise operator has orchestrated a remarkable recovery. The surge in demand for cruise vacations is evidenced by Carnival’s robust revenue and bookings. Carnival reported record revenue in the most recent quarter, with bookings in the two weeks around Black Friday hitting an all-time high.

For the fiscal year ending in November, Carnival reported record revenue exceeding $21 billion and embarked on the new year with its strongest booked position to date, factoring in occupancy and price. This has significantly contributed to earnings growth, such as reporting a narrower-than-expected U.S. GAAP net loss of $74 million and positive adjusted net income of $1 million for the year.

The prevailing concern among investors about Carnival’s debt levels is receding. While the pandemic-induced hiatus weighed heavily on Carnival, resulting in substantial accrued debt, the company has made significant headway by trimming debt by $4.6 billion from its peak. Carnival anticipates continued growth in adjusted free cash flow to further pare down its debt.

Carnival’s record booking volumes and customer deposits fuel optimism about earnings, with the company’s operational streamlining and fuel cost reduction efforts adding to its earnings growth potential.

Therefore, as Carnival powers through its revival and growth narrative, there couldn’t be a more opportune time to embrace this stock.

3. Apple’s Unyielding Brand Magnetism

Apple (NASDAQ: AAPL) stands tall in the market, spearheading with iconic products like the iPhone and Mac computers. However, this doesn’t signify a growth plateau for the company. Three key factors are poised to prop up Apple’s earnings trajectory in the foreseeable future.

Image source: Getty Images.

Firstly, Apple’s brand allure ensures customer loyalty, deterring users from veering towards rival products and instead enticing them to acquire the latest iPhone or Apple Watch. This brand sway is integral to Apple’s competitive advantage or economic moat, a pivotal element that can perpetuate the company’s leadership over time.

Apple’s Market Momentum: Sailing the Waters of Growth

Apple’s most recent quarter has witnessed a surge in its services business. The loyal fanbase of Apple has wholeheartedly embraced various subscription-based services offered through their devices, propelling the segment to report record revenue. These services range from digital content to cloud storage, creating a robust recurring revenue stream for the tech giant.

The Potent Source of Recurrent Revenue

The installed base of active Apple devices has now surpassed 2 billion, underscoring the vast user base that the company has cultivated since its inception. This colossal user base has now evolved into a potent source of recurrent revenue, driving Apple’s growth trajectory.

Profitable Margins and Market Share Expansion

Furthermore, the gross margins on Apple’s services have outstripped those on products, with a notable 70% compared to 36% in the most recent quarter. This considerable margin differential serves as a testament to the profitability of Apple’s services business.

Apple is also continuing to allure new customers, indicating that the company has not yet reached its zenith in gaining market share. In the recent quarter, a striking 50% of Mac and iPad purchasers were newcomers to these products, showcasing the untapped potential in expanding Apple’s consumer base.

An Alluring Growth Trajectory

Considering these compelling factors, Apple’s growth narrative appears primed for an enduring journey. The new bull market heralds one of the most exhilarating chapters for both the company and its shareholders, fostering a promising outlook for the future.

Should you invest $1,000 in Amazon right now?

Before contemplating an investment in Amazon, it is crucial to ponder the following:

The Motley Fool Stock Advisor analyst team has recently identified what they believe are the 10 best stocks for investors to buy at present, and Amazon did not make the cut. The selected stocks hold the potential to deliver substantial returns in the ensuing years.

Stock Advisor furnishes investors with a straightforward blueprint for success by offering guidance on portfolio construction, regular updates from analysts, and two fresh stock picks per month. Since 2002, the service has yielded returns more than three times the S&P 500*.

*Stock Advisor returns as of January 22, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Adria Cimino has positions in Amazon. The Motley Fool has positions in and recommends Amazon and Apple. The Motley Fool recommends Carnival Corp. The Motley Fool has a disclosure policy.