MercadoLibre‘s MELI aggressive expansion of its first-party (1P) business is emerging as a key headwind to margin recovery. While the strategy is strengthening assortment, improving pricing competitiveness and helping the company gain share across key categories, the rapid scaling of inventory-led commerce is introducing structural profitability pressures that could weigh on operating leverage for longer than anticipated.

The company’s 1P gross merchandise volume grew 69% year over year on a foreign exchange-neutral basis in the first quarter of 2026, significantly outpacing overall marketplace growth. The strategy has been particularly effective in consumer electronics, where MercadoLibre has expanded its competitive position through broader selection and sharper pricing. However, unlike the higher-margin third-party marketplace model, 1P requires inventory ownership, procurement spending and greater fulfillment intensity. As the business scales, associated logistics, warehousing and inventory management costs are likely to rise alongside volume growth, creating a more capital-intensive operating profile.

Gross margin contracted 300 basis points year over year in the first quarter of 2026, with rapid 1P expansion among the key drivers of the decline. Although profitability within certain mature 1P categories has improved, the broader business continues to absorb a growing share of corporate allocations as it scales faster than the overall marketplace. This dynamic suggests margin dilution will likely persist even as scale benefits gradually emerge.

MercadoLibre appears willing to continue prioritizing market-share gains and ecosystem expansion over near-term earnings optimization. As 1P continues to outpace the broader marketplace and absorb a growing share of corporate costs, the path toward margin normalization is expected to remain challenging.

MELI Faces Stiff Competition

MELI faces stiff competition from Amazon AMZN and Alibaba BABA, both of which have expanded logistics and inventory-led commerce capabilities to strengthen user engagement and pricing competitiveness.

Amazon continues to scale its first-party retail network despite persistent fulfillment cost pressures, and its scale advantage sets a high bar for efficiency. Alibaba has likewise increased investments across direct retail and supply-chain infrastructure, navigating similar margin trade-offs as it defends its share.

Unlike Amazon and Alibaba, MELI is expanding 1P while simultaneously ramping fintech, free shipping and logistics spend, which could keep profitability under pressure for longer.

MELI’s Share Price Performance, Valuation and Estimates

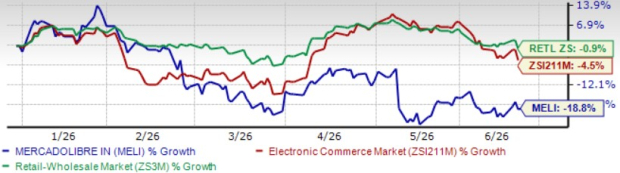

MELI shares have declined 18.8% in the year-to-date (YTD) period, and the Zacks Internet–Commerce industry and the Zacks Retail-Wholesale sector have declined 4.5% and 0.9%, respectively.

MELI’s YTD Price Performance

Image Source: Zacks Investment Research

From a valuation standpoint, MELI is currently trading at a forward 12-month Price/Sales ratio of 1.83X compared with the industry’s 1.99X. MELI has a Value Score of F.

MELI’s Valuation

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for MELI’s 2026 earnings is pegged at $40.97 per share, indicating a 3.98% year-over-year increase.

MercadoLibre, Inc. Price and Consensus

MercadoLibre, Inc. price-consensus-chart | MercadoLibre, Inc. Quote

MercadoLibre currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks’ Research Chief Names “Stock Most Likely to Double”

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company’s customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners Up

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

MercadoLibre, Inc. (MELI) : Free Stock Analysis Report

Alibaba Group Holding Limited (BABA) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.