Unveiling Netflix’s Q2 Triumph

Netflix showcased remarkable resilience in Q2, escalating revenue by 17% year-over-year to $9.55 billion, surpassing projections. Driven by hit releases like Baby Reindeer and Bridgerton, the platform attracted 8 million new subscribers, exceeding forecasts. Notably, Netflix’s operational margin surged to 27.2%, up from 22.3% last year, portraying robust financial health amidst substantial content investment.

Insights into Netflix’s Q3 Projections

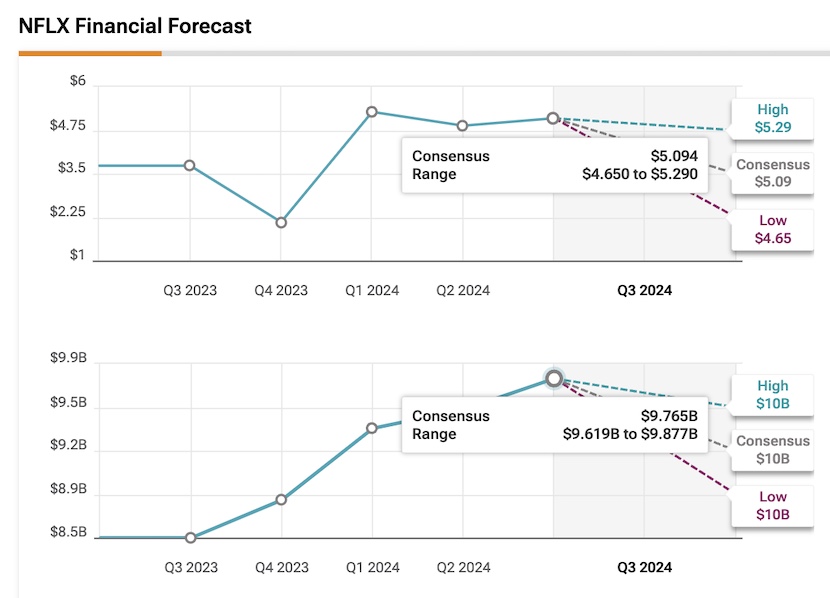

As Netflix anticipates a 14% revenue growth and an operating profit margin of 28.1% in Q3, the platform is poised for significant expansion. To outstrip market expectations, Netflix needs to outdo the $5.09 EPS target and $9.765 billion revenue projection. Despite varying analyst sentiments, with a majority revising EPS forecasts upwards, Netflix remains a promising investment target.

Netflix’s Evolution as a Growth Entity

Netflix’s resurgence as a growth stock is a testament to its strategic shift towards monetization, accentuated by the phasing out of the basic plan in favor of an ad-tier option. By prioritizing ad revenue potential, Netflix is recalibrating its revenue streams, priming itself for sustained growth. The upcoming focus on advertising efficacy may overshadow subscriber metrics in the Q3 performance evaluation.

Anticipating Post-Earnings Volatility

Post-earnings volatility has been the norm for Netflix, reflective of market discord on its value proposition. Key contributing factors include Netflix’s P/E ratio, currently at 37.7x, the highest since 2022. Despite the escalating valuation, the forecasted EPS growth suggests a de-risked growth opportunity for long-term investors.

Interrogating Netflix’s Q3 Earnings Potential

The Netflix Conundrum: Navigating Expectations and Forecasts

The Volatile Netflix Landscape

Netflix continues to dance on the market’s unpredictable stage. As we brace for Q3, the option chains foretell a stormy scenario – an expected earnings move of 8.33% in any direction. The at-the-money straddle for options expiring post the October 18th earnings announcement, anchored at the $720 strike price, reveals call options tagged at $31.25 and put options at $28.76. Brace yourself for a bumpy ride!

Insights from Wall Street Analysts

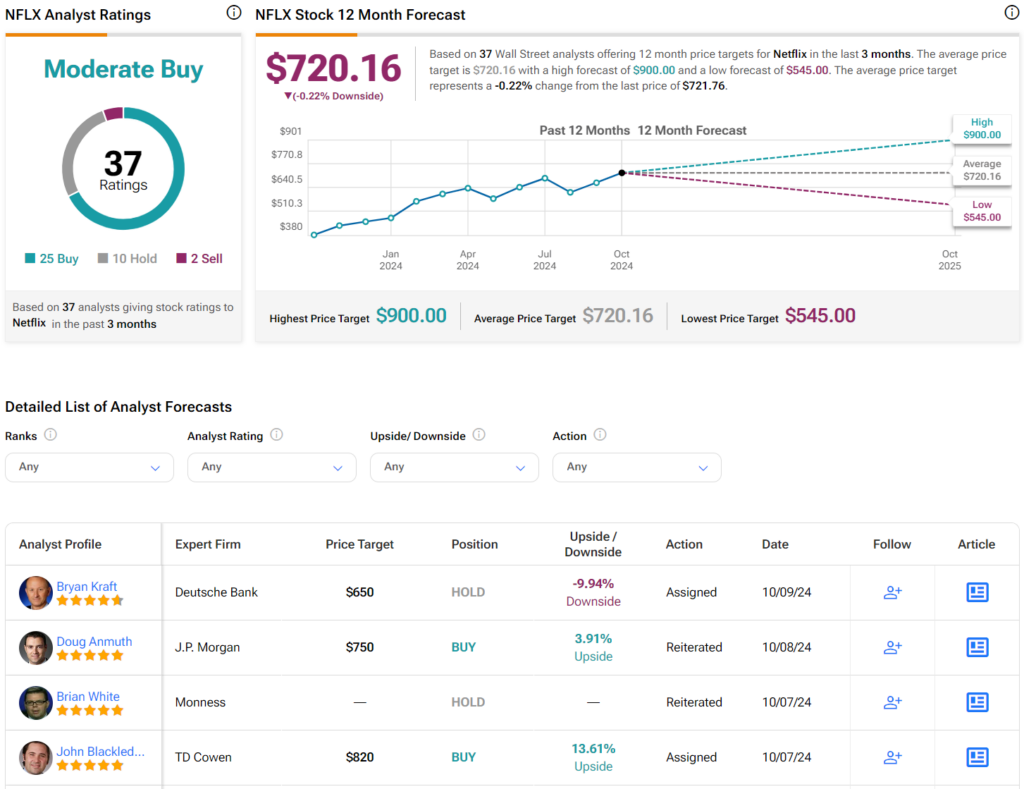

Based on TipRanks insights, the Wall Street consensus on Netflix (NFLX) indicates a Moderate Buy sentiment. Among the 37 analysts dissecting the stock, 10 suggest a Hold, two vote for a Sell, and the rest advocate a Buy. Furthermore, the average price target for NFLX stands at $720.16, hinting at limited upward momentum. Is it time to tread cautiously?

Strategic Navigation Amidst Volatility

Predicting patterns amidst the tumultuous currents of Netflix’s market performance, I find solace in the belief that the streaming giant is poised for ongoing growth in Q3. The pivot towards advertising and accentuation of monetization over customer expansion may begin to manifest in this quarter and strengthen in the forthcoming ones.

As the stock scales unprecedented heights in the lead-up to earnings, signs point to a possible short-term bearish trend. Despite this, I hold firm that those investing in NFLX shares, even at current valuations, will reap the fruits of their labor. I advocate considering Netflix as a Buy ahead of earnings and even more so in the event of a fallback. Navigate wisely through the Netflix labyrinth!

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.