Tech juggernaut Microsoft (NASDAQ: MSFT) recently wrapped up its fiscal year 2024 with robust fourth-quarter earnings. It’s astounding how a corporate giant, boasting over $200 billion in annual revenue and the world’s second-largest market capitalization, continues to exhibit growth. While Microsoft’s Q4 financials surpassed analysts’ forecasts in revenue and profit, the stock saw a minor decline following the announcement.

Are there lurking concerns within Microsoft’s quarterly results? An analysis of the earnings aims to uncover what went right, what went awry, and whether now is an opportune moment to consider buying the stock.

Resilience Across Diversified Operations

Microsoft’s reach is ubiquitous in society, as evidenced by a recent IT outage that impacted millions of computers globally, affecting critical sectors such as airlines and banking. The company pervades nearly all realms of modern technology. Its software underpins both personal and corporate computing environments. Azure, its cloud service, serves as an internet backbone. Additionally, Microsoft boasts renowned gaming titles, the professional network LinkedIn, and more.

Remarkably diverse, Microsoft continues to deliver robust growth across its spectrum. Commercial Office 365 software sales surged by 12% year over year, with personal 365 subscriptions climbing to 82.5 million from 80.8 million three months earlier. LinkedIn revenue saw a 10% year-over-year increase. The Azure cloud and related services achieved a 29% revenue growth, propelled by artificial intelligence trends. Even the long-standing Windows platform recorded a 7% sales uptick. Overall, Microsoft’s Q4 revenue soared by 15% year over year to $64.7 billion, with earnings per share at $2.95, up by 10% from the previous year.

Investors might not fully grasp the magnitude of the feat of a sprawling and multifaceted corporation like Microsoft maintaining double-digit growth across its vast portfolio.

The AI Opportunity for Microsoft

Azure’s 29% growth in Q4 missed the 30% to 31% target set by management in the preceding quarter if one thing could be pinpointed as a blemish. While the stock did not plummet, the slight downturn appears attributable to this perceived deficiency in Azure growth. However, during the Q4 earnings call, management provided crucial context.

Management highlighted that Azure AI is presently constrained by inadequate capacity to meet demand. AI alone accounted for eight percentage points of Azure’s growth. The customer base for Microsoft’s Azure AI expanded to over 60,000 in Q4, marking a 60% surge from a year earlier, with a notable uptick in expenditure per customer. Microsoft directed $19 billion towards capital expenditures in Q4, nearly all of which was earmarked for cloud and AI investments. Forecasts indicate escalated spending in 2025 to cater to robust AI demand.

Azure AI likely would have displayed more growth in Q4 had there been sufficient capacity. This “good” issue indicates long-term growth potential with expanded data center capabilities.

Opining on Microsoft’s Investment Appeal

The cloud division constitutes Microsoft’s largest and most rapidly advancing segment, expected to continue propelling overall growth as AI capacity becomes operational.

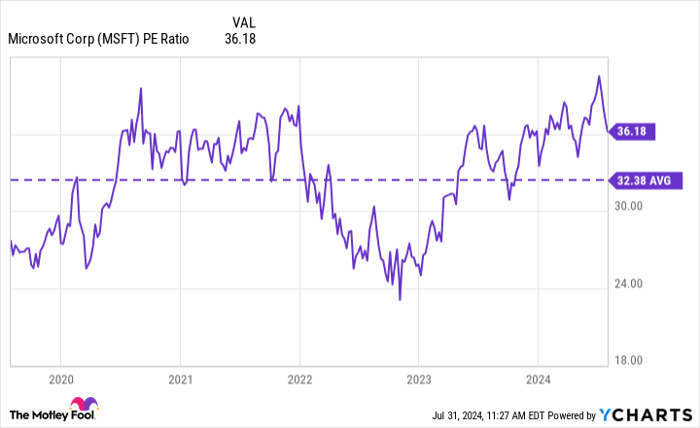

Industry analysts predict a 16% average annual earnings growth for Microsoft over the next three to five years. This projection seems reasonable given the current revenue growth trajectory. Capital investments are also anticipated to taper over time, leading to increased earnings. Despite promising growth prospects, Microsoft’s shares trade at a price-to-earnings (P/E) ratio of 35 times the company’s 2024 earnings, translating to a resulting price/earnings-to-growth (PEG) ratio of 2.2, considered steep even for a company demonstrating earnings growth like Microsoft. Over the past five years, Microsoft has maintained an average P/E ratio of 32.

It appears that Microsoft may be slightly overvalued at present, potentially elucidating why the market reacted to the minutest flaw in its earnings report by shedding the stock. Therefore, investors are advised against hastily plunging into acquiring Microsoft shares. Market fluctuations are inevitable, offering investors additional opportunities to consider investing in high-flying equities like Microsoft.

Exercising patience might reap rewards in Microsoft’s case.

Considering an Investment in Microsoft

Before contemplating a Microsoft share purchase, it’s prudent to reflect on the following:

The Motley Fool Stock Advisor analyst team recently released their compilation of what they deem the 10 best stocks for investors to currently consider, with Microsoft surprisingly being omitted. The chosen 10 stocks hold the potential to yield substantial returns in the forthcoming years.

Reflecting on past instances, such as when Nvidia made it to the same list on April 15, 2005 – an investment of $1,000 at the recommendation time would have burgeoned to $657,306!*

Stock Advisor offers investors a streamlined blueprint for success, encompassing guidance on portfolio construction, periodic updates from analysts, and two fresh stock picks monthly. The Stock Advisor service has surpassed the S&P 500’s returns more than fourfold since 2002*.

Justin Pope has no position in any stocks mentioned. The Motley Fool holds positions in and recommends Microsoft. The Motley Fool suggests options including long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft.