Recent events have thrust CrowdStrike CRWD, a key player in innovative endpoint security, threat intelligence, and cyber incident response services, into the limelight following a widespread IT disruption that paralyzed significant sectors of the economy and impacted numerous Microsoft MSFT Windows devices.

Days of tumult have shaken the stock in response to the crisis. But the burning question remains: Is the current plunge an entry point for investors, or should they bide their time until more clarity emerges? Let’s delve deeper into the situation.

The CrowdStrike Tumble

The recent downturn has driven down valuation metrics, with shares now trading at a forward 12-month price-to-sales ratio of 14.3X, a significant drop from the lofty 23.8X peak earlier this year. Projections indicate a 30% surge in sales for the company this fiscal year, though these estimates are likely subject to revision post the recent disruption.

Further complicating matters, Guggenheim Securities, BTIG, and Scotiabank have downgraded their stock ratings from ‘Strong Buy’ to ‘Hold’, underscoring the potential adverse effects in the offing.

In the aftermath, Microsoft issued a statement declaring, ‘While software updates may occasionally disrupt operations, major incidents like the CrowdStrike event are infrequent. Our current analysis suggests that the update affected 8.5 million Windows devices, representing less than one percent of the total Windows user base.‘

Despite the tempting dip, due to the company’s established stature and sheer magnitude, it might be prudent for investors to exercise patience on the sidelines until the clouds dissipate. Moreover, its current Zacks Rank #5 (Strong Sell) signifies further downward pressure on the stock in the short term.

Rivals Eyeing Opportunities

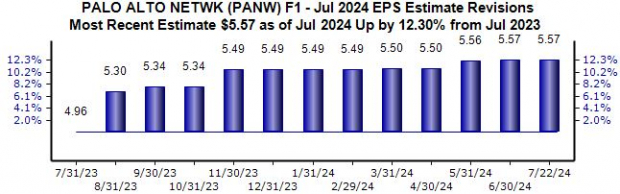

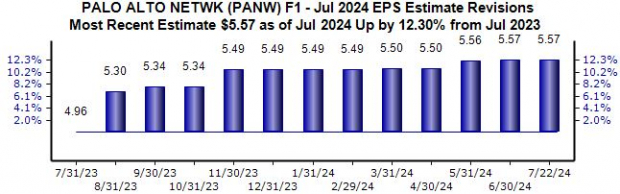

Given the recent turn of events, several cybersecurity firms could witness favorable winds, including Palo Alto Networks PANW. The company’s outlook for the current year remains optimistic, with projected earnings of $5.57 per share, a 12% increase from the previous year.

Image Source: Zacks Investment Research

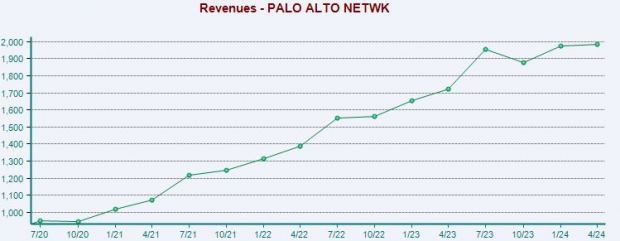

Palo Alto Networks anticipates robust revenue growth, with a forecasted 16% surge in sales for the ongoing fiscal year. The company has maintained a robust growth trajectory, consistently delivering double-digit year-over-year revenue increases in each of its past ten quarterly reports.

Displayed below is a chart illustrating the company’s quarterly sales data.

Image Source: Zacks Investment Research

Final Thoughts

The recent fiasco involving CrowdStrike CRWD, which led to the halt of Microsoft MSFT devices, has undoubtedly created headwinds for the stock, prompting a significant decline post-incident.

While some may view the sharp price movement as a chance to enter the stock, the company’s murky earnings outlook, as indicated by its Zacks Rank #5 (Strong Sell), suggests further downward pressure on its shares in the near future. Instead, investors may consider shifting focus to stocks with positive earnings forecast revisions.

Moreover, we might only be witnessing the initial repercussions of the incident, with the full extent of the impact still shrouded in uncertainty. A competitor like Palo Alto Networks PANW could experience increased investor interest given its competitive positioning vis-à-vis CrowdStrike.