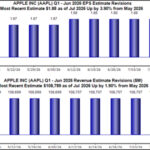

Key Points

The turnaround in Intel’s foundry business appears to be working, including a reported chipmaking agreement with Apple.

Taiwan Semiconductor still produces more than 90% of the world’s most advanced chips.

Demand for leading-edge manufacturing capacity is running well ahead of supply.

- 10 stocks we like better than Intel ›

Intel (NASDAQ: INTC) is having a moment. The stock spiked to an all-time high on Thursday after President Donald Trump said on social media that Apple had agreed to work with the company to design and build chips in the U.S. It was the latest in a run of high-profile interest that includes an announced collaboration with Nvidia.

After years of being written off, Intel’s foundry comeback suddenly looks convincing — and the stock is up more than 500% over the past year.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

This raises a fair question about the longtime foundry leader, Taiwan Semiconductor Manufacturing (NYSE: TSM): Is its grip on advanced chip manufacturing finally loosening?

Imag source: Getty Images.

Intel’s foundry moment

After falling behind on manufacturing technology for the better part of a decade, Intel has bet its future on becoming a contract chipmaker that builds silicon for outside customers, not just for itself.

Its 18A process, which entered high-volume production last October, is the centerpiece. Intel’s first 18A laptop chip, Panther Lake, started selling early this year, and a server chip followed in the spring. The list of would-be customers has grown, too. Beyond the reported Apple arrangement, which neither company has confirmed, Intel has pointed to a collaboration with Nvidia and a multibillion-dollar deal to make custom artificial intelligence (AI) chips for Amazon.

The momentum is hard to argue with.

But don’t get too excited just yet. Intel’s foundry segment generated $5.4 billion in revenue in the first quarter, up 16% year over year — yet just $174 million of that came from outside customers. The rest was Intel building chips for Intel. The segment also posted a $2.4 billion operating loss for the period.

With that said, CEO Lip-Bu Tan has said he expects early design commitments from external customers in the second half of 2026.

Why TSMC still runs the industry

Taiwan Semiconductor builds chips for much of the industry, including Nvidia and Apple, at a scale no rival can match. It controls about 70% of the pure-play foundry market and more than 90% of the world’s leading-edge production — the cutting-edge nodes that the most advanced AI and smartphone chips require. That’s exactly the part of the business Intel is trying to break into, and the hardest part to crack.

TSMC’s first-quarter revenue rose about 41% year over year to $35.9 billion, with a gross margin of 66.2% and an operating margin of about 58%.

Demand, meanwhile, keeps outrunning what TSMC can build. Management raised its full-year outlook and now expects 2026 revenue to grow more than 30% in U.S. dollar terms, and it plans to spend toward the high end of a $52 billion to $56 billion budget to add capacity.

The demand is “very robust, especially from the HPC and AI applications,” said TSMC Chairman and CEO C.C. Wei during the company’s first-quarterearnings call noting that supply remained very tight even as the company rushed to pull in equipment. But it’s going to take time for supply to ramp up to meet this demand. Building a new plant, he added, takes two to three years.

The better bet

So which stock deserves the benefit of the doubt?

There’s a fair case to be made that both can win. The AI build-out is generating so much demand that TSMC can’t keep up, and a sold-out leader leaves room for a credible second source. Additionally, Intel’s manufacturing is finally improving, and it has Washington’s backing. And a marquee customer like Apple — if the reported deal holds — would validate years of heavy spending.

But TSMC is probably the one I’d want to own if I had to choose between the two. Its lead at the leading edge is measured in years, not quarters, and customers keep signing up because no one else can match its scale and yields at the cutting edge. Indeed, even Intel still relies on TSMC to manufacture many of its own newest products.

Trading at about 40 times earnings, TSMC’s stock isn’t cheap, and it notably trades near its 52-week high. Yet that valuation multiple reflects a business growing quickly and posting some of the widest margins in the industry.

Intel, by contrast, is still losing money in the foundry business central to its comeback. Buyers today are paying an all-time high price for a turnaround that hasn’t fully arrived.

Should you buy stock in Intel right now?

Before you buy stock in Intel, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Intel wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $417,305!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,293,148!*

Now, it’s worth noting Stock Advisor’s total average return is 936% — a market-crushing outperformance compared to 209% for the S&P 500. Don’t miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of June 21, 2026.

Daniel Sparks and his clients have positions in Apple. The Motley Fool has positions in and recommends Amazon, Apple, Intel, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.