In the fast-paced world of the automotive market, trends can shift with the suddenness of a gusty wind. The meteoric rise of battery-powered electric vehicles (EVs) seemed unassailable until recently. Just a year ago, new unit sales for EVs were soaring at a staggering rate of 51% year over year. However, in a surprising turn of events, this growth momentum halted abruptly in the first quarter of 2024, with sales figures stagnating at previous year’s levels.

Emerging as a formidable protagonist in this narrative is plug-in hybrid technology. With a growth rate exceeding 50% year over year, plug-in hybrids have become the torchbearers of growth in the automotive sector. Sensing the shifting tides, Ford (NYSE: F) has made a decisive move by shelving plans for an all-electric SUV, opting instead for a plug-in hybrid model.

This strategic pivot by Ford raises a pertinent question – what does this mean for disruptive players like Rivian Automotive (NASDAQ: RIVN) that have pinned their hopes on the surge of all-electric pick-up trucks and SUVs? Let’s delve deeper into this unfolding saga.

The Evolution of Ford’s Product Strategy

A few years back, Ford embarked on an ambitious journey into the realm of battery power and EV technologies. Initiatives like the Mustang Mach-E and F-150 Lightning heralded Ford’s foray into the electric vehicle domain. In 2021, Ford unveiled plans for an $11.4 billion investment in American factories, earmarked for churning out batteries and electric cars. However, the script has taken a different turn.

Contrary to the all-electric trajectory, Ford’s upcoming SUV lineup will pivot towards plug-in hybrids. This shift doesn’t render Ford’s multi-billion-dollar investment redundant; instead, it repurposes it towards hybrid vehicles that necessitate substantial lithium-ion batteries, albeit in lesser quantities. Consumers are gravitating towards the versatility offered by plug-in hybrids, evident from the 59% year-over-year surge in Q1 2024 sales.

Currently, the consumer sentiment favors the flexibility accorded by plug-in hybrids over the fully electric offerings put forth by Rivian and Tesla. The pulse of the market seems to resonate with this newfound preference for versatile mobility.

A Conundrum for Rivian

From one angle, supporters of Rivian could argue that the company stands on the right side of history. Rivian’s production lineup exclusively features all-electric SUVs and pick-up trucks, aligning with the growing demand for environmentally conscious vehicles. Yet, a critical challenge surfaces as Rivian deliberately sidesteps the plug-in hybrid segment, which currently commands the lion’s share of market growth.

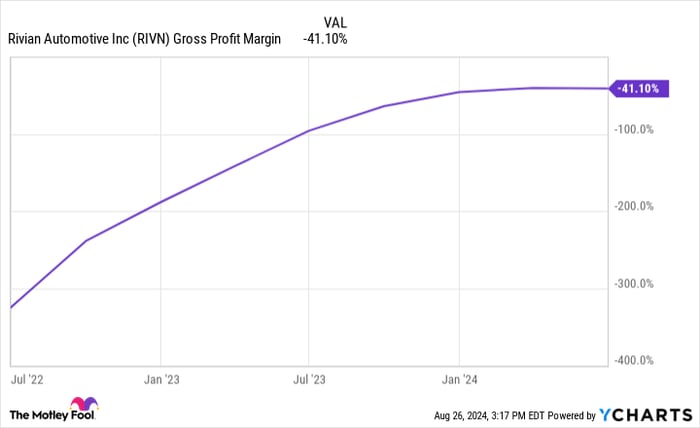

Reflecting on Rivian’s performance metrics reveals a stark reality. While production figures have plateaued around 60,000 vehicles per year, deliveries have seen a marginal uptick, primarily driven by depleting 2023 inventory. The troubling truth lies in Rivian’s negative 41% gross margin, despite the hefty $75,000 price tag on its average pick-up truck.

The Thorny Path Ahead for Rivian Stock

The paradigm shift towards plug-in hybrids spells trouble for Rivian’s future trajectory. To navigate these tumultuous waters, Rivian must secure a customer base willing to pay a premium for EVs and scale up production to propel its gross margins from negative to positive. Such a transformation mirrors Tesla’s journey when it ramped up Model 3 production.

Launching a new car model demands a hefty investment, encompassing design, supply chain logistics, and hefty capital outlays for manufacturing facilities. Rivian’s annual cash burn of $5 billion juxtaposed with an $8 billion cash reserve paints a stark picture of financial vulnerability. The road to profitability for Rivian seems fraught with hurdles, especially in light of the company’s stymied gross margin progression and stagnant production rates amid the ascendancy of plug-in hybrids in the U.S. market.

Final Verdict: Should Investors Bet on Rivian?

The burgeoning ascendancy of plug-in hybrids cast a looming shadow over Rivian’s prospects. The exigencies dictate a swift pivot towards aligning with market trends, securing financing, and galvanizing production to remain afloat in this dynamic landscape. As things stand, prudence dictates a cautious approach towards investing in the vulnerable and unprofitable Rivian stock at this juncture.

Before plunging into Rivian Automotive stocks, consider the insightful analysis from the Motley Fool Stock Advisor team. They’ve cherry-picked the top 10 stocks poised for substantial growth opportunities, with Rivian Automotive conspicuously missing from this exclusive list. The cited stocks hold the promise of significant returns in the foreseeable future, echoing the historic successes witnessed with earlier recommendations like Nvidia back in 2005.

*Stock Advisor returns as of August 26, 2024