Home Depot’s Performance Under Scrutiny

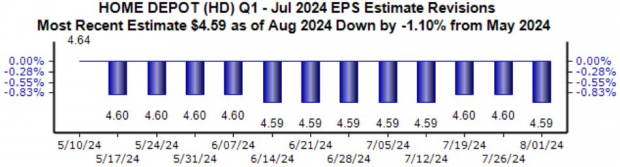

Amidst market volatility in 2024, Home Depot has shown a modest 2% growth, trailing the S&P 500. Expectations for the upcoming quarter have dipped, with anticipated earnings per share of $4.59 signaling a 1.3% decrease year-over-year.

The company’s comparable sales fell by 2.8%, resulting in lukewarm market reception. Despite this, Home Depot remains bullish on its product range, confident in the benefits it will offer.

Notably, a recurring trend of soft sales in big-ticket discretionary items persists, hinting at consumer behavior changes post-pandemic.

Revenue projections remain steady, with an expected 0.8% decline. Valuation multiples are slightly elevated, standing at a forward 12-month earnings multiple of 22.8X, above the five-year median.

Walmart’s Winning Streak Continues

In contrast, Walmart has seen a stellar 2024 performance, bolstered by robust quarterly results. Earnings grew by 22% year-over-year, with sales climbing 6%.

Analysts hold a positive outlook for the impending quarter, with a Zacks Consensus EPS estimate of $0.65, up 1.6% and implying 6.5% growth compared to the previous year. Expected revenue stands at $168.4 billion.

Walmart’s eCommerce segment has been a major growth driver, showcasing a 21% year-over-year rise, underscoring the company’s digital success.

Deere & Co Facing Headwinds

In stark contrast, Deere & Co has struggled in 2024, witnessing an 11% decline and trailing the S&P 500. Back-to-back poor results have weighed on its stock performance.

The latest sales figures show a 12% drop due to softening global agricultural and turf demand. However, a stable construction sector offers a glimmer of hope amidst the challenging landscape.

Analysts anticipate a bearish outcome for the upcoming release, with an expected $5.85 per share, reflecting a more than 15% decrease since mid-May.

The CEO remains optimistic about the company’s resilience, citing, “Thanks to the dedication and hard work of our team, we continue to demonstrate structurally higher performance levels across business cycles and are benefitting from stability in construction end markets amid declining agricultural and turf demand.”

Currently, the stock holds a Zacks Rank #4 (Sell) ahead of the earnings announcement.

Tying It All Together

As the critical Q2 earnings season unfolds, early results have been encouraging. The upcoming reports from key industry players like Home Depot, Walmart, and Deere & Co will shed further light on sectoral performances.