Nvidia(NASDAQ: NVDA), the titan of chip stocks, has set the market ablaze with its scorching performance over the past five years. Initially renowned for crafting gaming GPUs, Nvidia’s trajectory changed with the explosive growth of the artificial intelligence (AI) realm. This evolution compelled companies to flock to Nvidia for its elite data center GPUs, tailored for navigating intricate AI operations.

A thrilling ascent of over 2,000% catapulted Nvidia’s market capitalization to a staggering $2.4 trillion, minting an array of millionaires along the way. However, this incredible momentum has sparked a fervent hunt among investors, scanning the horizon for the next prodigious chip powerhouse poised to mirror Nvidia’s triumphant journey.

Image source: Micron.

Could that sought-after contender be Micron (NASDAQ: MU), a global powerhouse revered for its DRAM and NAND memory chips? Let’s dissect the contrasting realms of Micron and Nvidia to discern if Micron stands a chance in tracing Nvidia’s illustrious trail.

Deciphering Micron and Nvidia’s Divergence

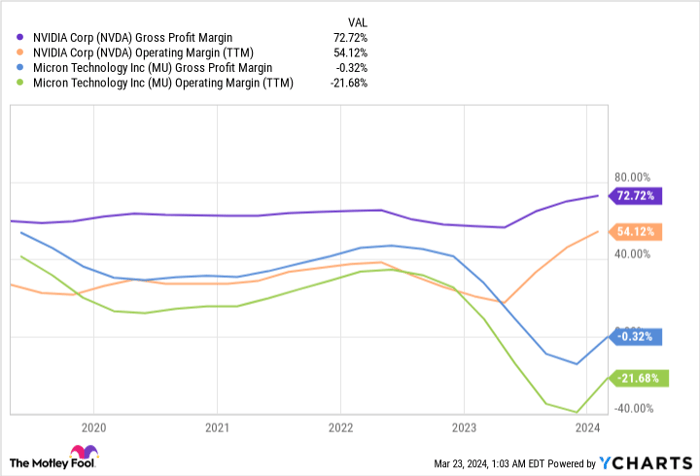

Micron adopts a strategy where it not only designs its memory chips but also manufactures them in-house at its foundries. This stands in stark contrast to Nvidia, which designs its chips but entrusts their production to third-party foundries like Samsung and Taiwan Semiconductor Manufacturing Company. Micron navigates this capital-intensive model at significantly tamer margins than Nvidia.

Data source: YCharts

Micron’s memory chips are priced more affordably compared to Nvidia’s GPUs and lack the dominant foothold that Nvidia commands within its core markets. While Micron ranks as the globe’s third-largest provider of DRAM chips and the fifth-largest purveyor of NAND chips, Nvidia reigns supreme as the premier producer of discrete GPUs by a substantial margin. According to JPR, Nvidia wielded an 80% market share by the conclusion of 2023, while AMD trailed with a mere 19% slice.

In contrast to Nvidia’s more specialized domain, Micron operates amid a more standardized landscape, possessing lesser pricing leverage against rivals and enduring heightened vulnerability to cyclical ebbs as the memory chip sector grapples with its cyclical swings. Notwithstanding, Micron boasts a technological edge in crafting denser and more energy-efficient DRAM and NAND chips than its primary competitors, Samsung and SK Hynix. This advancement equips Micron to snag contracts with manufacturers of upscale PCs, mobile devices, and servers.

Forecasting the Duration of Micron’s Upcoming Growth Cycle

A turbulent spell shadowed Micron in recent years as dwindling personal computer (PC) sales post-pandemic, the conclusion of the 5G upgrade era, and macroscopic headwinds impeded chip sales to enterprise and industrial sectors. Additionally, the Chinese administration barred key infrastructure entities from procuring Micron’s memory chips. These obstacles counterbalanced Micron’s robust growth in the automotive and AI landscapes.

Micron observed a 29% revenue spike in fiscal 2021 (culminating in September 2020), followed by an 11% uptick in fiscal 2022, and a subsequent 49% nosedive in fiscal 2023. Encouragingly, analysts project a 56% revenue surge in fiscal 2024 and a further 43% climb in fiscal 2025, propelled by three integral tailwinds. Firstly, equilibrium should gradually settle in the PC and smartphone markets. Secondly, heightened chip demands from the enterprise, industrial, and automotive sectors are anticipated as the macro setting reawakens.

Ultimately, the burgeoning expansion of the generative AI domain shall impel more data centers to upgrade their memory chips alongside Nvidia’s GPUs. Elucidating this trend during Micron’s recent conference call, CEO Sanjay Mehrotra likened the memory chip market to being “at the very early innings of a multiyear growth phase spearheaded by AI.” He surmised that these technologies would revolutionize “every facet of business and society,” predicting AI-enhanced phones to sport “50% to 100% greater DRAM content than contemporary non-AI flagship phones.”

Contemplating the Inescapable Cycle of Downturns

This glowing outlook notwithstanding, Micron’s anticipated growth cycle is destined to wane in a few years. When particular sectors such as smartphones, cloud data centers, and AI experience vibrant surges, companies amplify memory chip acquisitions, subsequently spurring a matching surge in chip prices.

Subsequently, Micron and its industry peers ramp up chip production to meet the escalating demand. However, once the fervor in these sectors cools down, the chip scarcity rapidly morphs into a glut as companies grapple with a surplus chip inventory. This cyclical rhythm has precipitated Micron’s chip sales slump in 2019 and 2022 – portending a similar trajectory as the AI sector matures.

While this upcoming growth cycle might endure longer than its precursors, its eventual downturn remains inevitable. Similarly, Nvidia will grapple with its share of slowdowns; however, the choppiness in its performance tends to be milder compared to Micron’s protracted undulations over the past decade. Nvidia’s dominance in the discrete GPU realm affords it increased price elasticity during market contractions, while Micron remains ensnared in the volatile price upheavals from its colossal adversaries.

Picturing Micron’s Ascent to Nvidia’s Pinnacle

Currently trading at less than 4 times next year’s sales, Micron could chart an upward trajectory as its forthcoming growth cycle kicks off. Should its valuations remain stable and its revenue burgeon at a compounded annual growth rate (CAGR) of 30% in the ensuing five years, its stock might nearly quadruple. This prospective achievement is nothing short of remarkable, yet it possibly culminates in a cyclical contraction and pales in comparison to Nvidia’s meteoric rise in recent times.

Should you invest $1,000 in Micron Technology right now?

Prior to embarking on a Micron Technology investment, ponder this:

The Motley Fool Stock Advisor analyst squadron has identified what they deem as the 10 best stocks for investors to snap up at this juncture… and Micron Technology did not make the cut. The chosen 10 stocks hold the potential to yield substantial returns in the impending years.

Stock Advisor extends a foolproof template for investors to thrive, offering counsel on portfolio construction, routine insights from analysts, and a pair of fresh stock recommendations monthly. Since 2002, the Stock Advisor service has tripled the returns of the S&P 500*.

*Stock Advisor returns as of March 25, 2024

Leo Sun has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.