Current Landscape of Debt Issuance in the Cannabis Sector

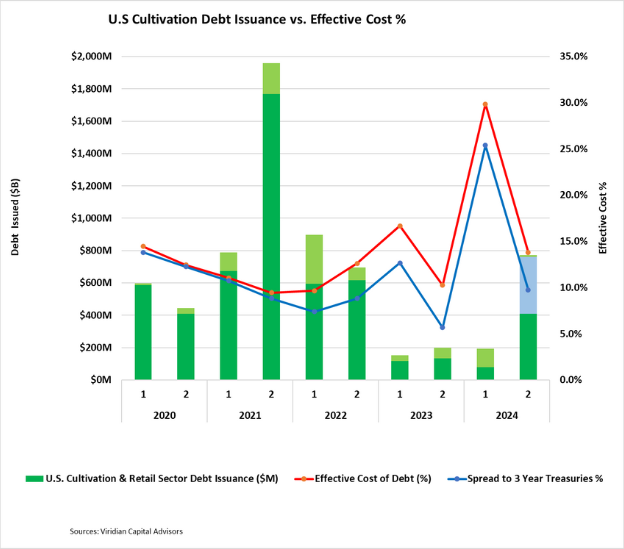

Debt issuance within the U.S. Cultivation & Retail sector during the second half of 2024 has surpassed all previous periods since the second half of 2022. With ongoing financial support expected for the remainder of the year, debt volumes are projected to outperform all periods except for the second half of 2021 and the first half of 2022.

The bulk of the debt issuance in the latter part of 2024 has primarily been driven by refinancing activities, involving key players such as Ascend, Jushi, and Terrascend. Despite their tax-adjusted net debt exceeding 3x Debt/EBITDA, the consistent attraction of these entities has led debt investors to be optimistic about the likelihood of 280e relief.

Distinctly colored bars on the graph delineate the dollar value of debt issuance where sufficient data enables effective cost calculation. Additional refinancing activities anticipated in the latter part of 2024 are expected to be dominated by Green Thumb and Curaleaf maturities. The effective costs, represented by the dollar-weighted average and yield spread to the 3-year treasury, exhibit visible trends over time.

Viridian’s assessment of all debt issuance involves a comprehensive evaluation of various factors such as coupon rates, maturity periods, OID, convertibility, and associated warrants. The meticulous approach also factors in embedded conversion options and warrants as additional original issue discounts in determining the effective cost.

Historical Context and Trends in Effective Costs

The effective costs recorded in the second half of 2023 were remarkably low due to a significant concentration of bank debt financings, with notable examples including Trulieve, Marimed, Cresco, and AYR, all showcasing comparatively nominal rates despite the prevailing market conditions.

Conversely, the initial half of 2024 saw average effective costs surge due to a couple of expensive deals. Notably, AYR’s $50 million add-on with a 13% coupon rate, substantial OID, and warrant coverage, as well as the Cannabist’s percent conversion deal, significantly contributed to the hike in effective costs.

However, the latter half of 2024 revealed a noteworthy decline in the average effective cost to 13.8%. Transactions involving Ascend, TerrAscend, and Jushi showcased remarkable cost efficiencies during this period.

While spreads to treasuries have closely retraced levels witnessed in the past, potential favorable developments on rescheduling could prompt further tightening in the range of 200-300 basis points.

The analysis provided in the Viridian Capital Chart of the Week serves as a valuable resource for investors, shedding light on critical investment, valuation, and M&A trends sourced from the Viridian Cannabis Deal Tracker.

Understanding the Viridian Cannabis Deal Tracker

The Viridian Cannabis Deal Tracker offers a comprehensive market intelligence platform catering to cannabis businesses, investors, and acquirers, enabling informed decision-making regarding capital allocation and M&A strategies. The platform’s proprietary information service monitors capital raise and M&A activities within the legal cannabis, CBD, and psychedelics industries.

This exhaustive tracker segments deals based on industry sectors, deal structures, company statuses, involved principals, key deal terms, transaction locations, and credit ratings, providing a holistic perspective on the industry’s capital flow and M&A dynamics.

Since its inception in 2015, the Viridian Cannabis Deal Tracker has meticulously tracked and analyzed over 2,500 capital raises and 1,000 M&A transactions, collectively exceeding $50 billion in total value.