Delving into the upper echelon of the corporate world, where only giants tread, we find Nvidia standing as one of the privileged few with a market value exceeding $3 trillion. In this exclusive club, alongside Microsoft and Apple, Nvidia’s ascent to this peak is not merely a tale of past glories but a projection of future triumphs.

Nvidia’s Unwavering Dominance in the Market

Powered by the fervent demand for artificial intelligence (AI), Nvidia has claimed its throne. The prowess of its graphics processing units (GPUs) has become indispensable for the development and sustenance of AI-based business models. The parallel computing capability of GPUs, coupled with the agility to form clusters for amplified processing power, has been the linchpin behind Nvidia’s meteoric surge in recent times.

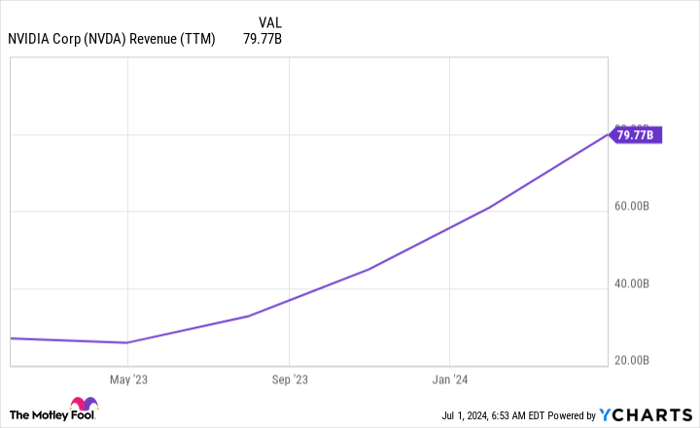

Surpassing its closest competitor, Advanced Micro Devices, Nvidia’s revenue numbers have skyrocketed, leaping from $30 billion to a staggering $80 billion within a span of just over a year.

Growth in Stock Reflects High Expectations

Yet, amidst this meteoric rise, lies a conundrum. While surging sales are the heartbeat of any company’s future, investors’ attention inevitably shifts to earnings. Herein lies the tale of two metrics, the price-to-earnings (P/E) ratio and the forward P/E ratio, juxtaposed against each other in Nvidia’s narrative.

At 72 times trailing earnings and 46 times forward earnings, Nvidia’s stock price encapsulates an anticipation of 59% earnings growth. A formidable figure indeed, but one that Nvidia has consistently outpaced in recent reports.

Nonetheless, as the wheel of time turns, straddling the line between maintaining the $3 trillion market valuation and a potential dip becomes paramount.

Meeting Profit & Revenue Heights Amidst Intense Competition

Sharing the rarefied air of a $3 trillion valuation with corporate stalwarts like Microsoft and Apple sets a high bar of expectation. Historically trading at around 30 times trailing earnings, Nvidia now grapples with the challenge of fulfilling this prophecy.

With current profit levels at $42.6 billion over the past year, the road to $100 billion in annual profit – a prerequisite for sustaining the valuation – appears daunting.

A shift in profit margins amidst rising competition poses a looming challenge. As top tech conglomerates strategize chip design autonomy to potentially sideline Nvidia’s GPUs, a potential market shift threatens to unsettle Nvidia’s dominion.

To preserve its position in the upper echelons of market capitalization, Nvidia must guard its revenue streams and profit margins with unyielding resilience amid encroaching threats. While the prospect of a business collapse remains unlikely, pressures may mount as investors recalibrate their expectations commensurate with the stock’s inflated valuations.

Contemplating Investment Amidst Uncertainty

As the narrative unfolds, the question looms – should prospective investors venture into the Nvidia landscape fraught with uncertainties and competitive pressures?

Charting a course amidst the undulating tides of market turbulence requires a blend of caution and foresight. Nvidia’s trajectory, steeped in rapid advancements and formidable competition, beckons investors to tread with calculated steps.

The allure of a $3 trillion valuation is accompanied by the shadow of intense scrutiny, as Nvidia navigates a landscape brimming with rivalries and expectations. As the saga unfolds, the captivating tale of Nvidia’s destiny awaits its next chapter.