A Closer Look Ahead

As it stands, BRF S.A. (NYSE: BRFS) is gearing up to unveil its second-quarter 2024 earnings come August 14. Expectations are ripe for a bottom-line expansion compared to the previous year’s showing. The estimated earnings per share of 7 cents mark a significant uptick from a loss of 10 cents in the corresponding period.

On the revenue front, a marginal retreat is on the cards. Analysts foresee quarterly revenues around $2.6 billion, indicating a slight dip of 2.6% year-over-year. It’s worth noting that BRF, a global powerhouse in the food industry, had surprised with a remarkable 50% earnings beat in the last quarter.

Understanding the Milestones

Driving BRF’s recent success is the ongoing traction of the BRF+ initiative. This strategic endeavor is designed to elevate commercial agility, operational efficacy, and cost rationalization. The company’s steadfast focus on premium and innovative products has not only fortified its pricing strategy but also fortified its market resilience.

The stability anticipated in feed costs in the short run is another boon, ensuring efficient cost control and thereby, enhancing profitability. The fusion of these elements likely served as the bedrock for the company’s performance in the upcoming quarter.

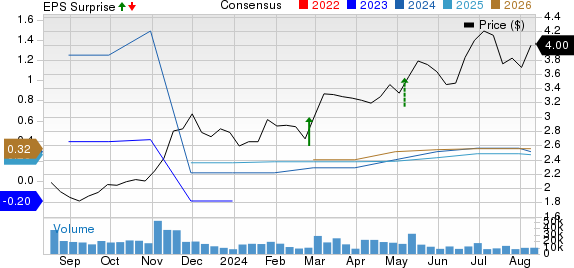

A Financial Compass: BRF S.A. Price, Consensus and EPS Projection

BRF S.A. price-consensus-eps-projection | BRF S.A. Quote

On the flip side, the Brazilian consumer landscape, albeit on a path to revival, is still grappling with issues like inflation and wavering employment rates. These factors have inevitably curtailed consumer expenditure and thereby, market demand. It is a well-known quirk that the first half of the year often ushers in seasonal frailties, which could construe as a dampener on the company’s to-be-disclosed quarter.

Unveiling the Zacks Perception

However, Zacks’ predictive model isn’t all sunshine and roses for BRF this time. The model blends an Earnings ESP with a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) to foresee an earnings triumph, a synergy that seems elusive here.

As things stand, BRF holds a Zacks Rank #3 and an Earnings ESP of 0.00%.

Spotlight on Promising Stocks

If you are in the hunt for promising contenders, here are a few prospects on the radar. Our model has signaled these companies as potential victors in the upcoming earnings tussle:

Ollie’s Bargain boasts an Earnings ESP of +2.38% alongside a Zacks Rank of 3. The firm is poised to notch up its bottom-line figures as it readies to decode the second-quarter fiscal 2024 results. Anticipated quarterly earnings per share of 78 cents envisage a solid upswing of 16.4% from the previous year.

Turning to Costco Wholesale Corporation, the conglomerate wields an Earnings ESP of +0.67% and a Zacks Rank of 3. Projections suggest an upward trajectory on both revenue and earnings fronts for the fourth quarter of fiscal 2024. Forecasts peg quarterly revenues at $80.1 billion, reflecting a 1.4% upsurge from the prior-year counterpart.

Looking over to Coty (NYSE: COTY), the beauty powerhouse clocks in with an Earnings ESP of +22.73% and a Zacks Rank of 3. The company is all set to unveil its fourth-quarter fiscal 2024 scorecard, with the Zacks Consensus Estimate pointing to earnings of 5 cents, a staggering 400% leap from the year-ago quarter.

The foreseen quarterly revenue estimate stands at $1.38 billion, outlining a promising 1.8% progression from the previous year. However, Coty has navigated through a rough patch, sporting a negative earnings surprise of 22.2% on a trailing four-quarter basis.