As investing aficionados sway in the storm of financial markets, the pendulum of fortune often swings between tech titans, Apple and Alphabet. While historical narratives offer clues, present pandemonium often obscures the future. In the pivotal epoch of 2024, Apple seems to have reclaimed its mojo, tracing an upward trajectory embellished with a 17.6% surge over the past three months. In stark contrast, Alphabet, Google’s parent company, finds itself in the thorny thicket of a 7.1% dip during the same period.

Striding boldly into 2024, both giants flaunt their prowess, each brandishing admirable gains. Apple’s ascent registers a formidable 16.6% jump year-to-date, but Alphabet outshines with a dazzling 17.3% spike.

With both luminaries parading strengths in innovation and market dominion, prospective investors now stand at the confluence, battling to discern the superior pick among these Big Tech behemoths.

Deciphering Apple Stock: Essential Considerations

Apple’s resurgence in the market arena can be chiefly attributed to its adept exploitation of artificial intelligence (AI) technology, woven seamlessly into its product tapestry. Despite a slight wane in iPhone revenue, Apple’s forays into AI herald a burgeoning tomorrow. In Q3 of fiscal 2024, iPhone revenue saw a 1% descent year-over-year, landing at $39.3 billion. Nevertheless, the allure of Apple’s AI-infused features is forecasted to beckon device upgrades and woo novel users.

Apple’s AI escapades, ranging from the advent of Apple Intelligence to its dalliance with ChatGPT, unfurl novel channels for monetization and future revenue expansion. Prognosticators anticipate this surge to propelling the growth of its Services division, which gloried in a record $24.2 billion revenue show in Q3. The projected rise in device upgrades and product volumes is poised to broaden the active device user base, consequently fuelling Services revenue. Wedded to AI, Apple’s ecosystem envisions augmented customer engagement and richer coffers from the Services segment.

The Apple coffers overflow with capital cascading back to investors. After showering over $27 billion in Q2 of 2024 through dividends and share buybacks, Apple once again sprinkled shareholders with over $32 billion in Q3. Investors greedily anticipate further dividends and an intensified share repurchase program.

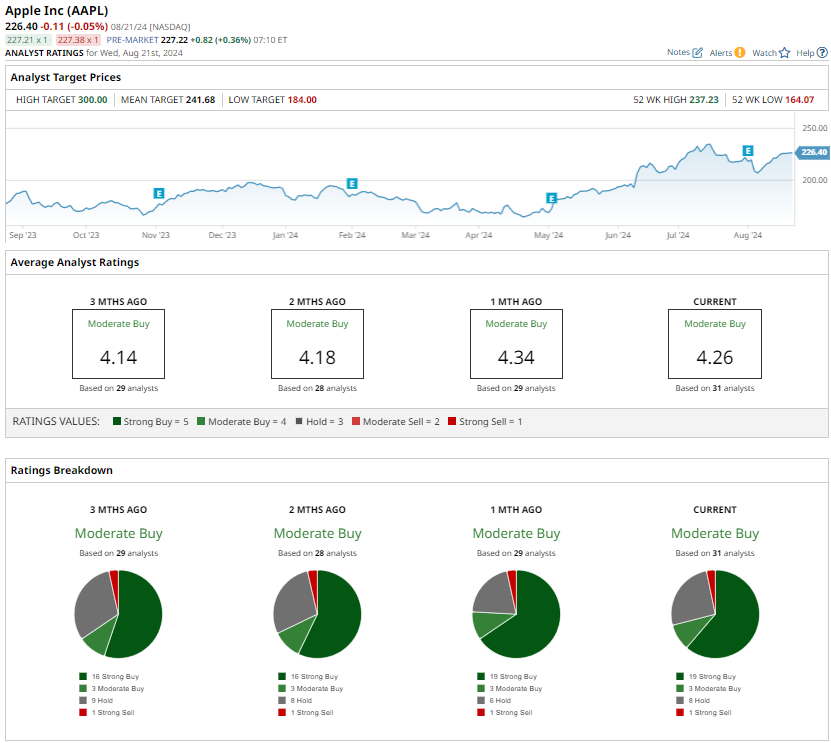

Yet, the goliath faces intensified competition in China and macro headwinds, casting dark shadows on its path towards glory. Such foreboding augurs are mirrored in analysts’ “Moderate Buy” consensus rating.

The moderate price target for Apple stock hovers at $241.68, implying a modest potential uptick of about 7.6% from recent levels.

Untangling Alphabet Stock: Core Tenets

Alphabet’s hegemony in the realm of digital advertising and cloud computing casts a long shadow, promising sturdy growth. Its resilience in the face of economic vagaries is manifest in the robust growth of its advertising revenue. Google’s advertising revenue surged by double digits over the last three quarters, driven by its supremacy in Search and unyielding fortitude on the YouTube front.

During the Q2 saga, Google’s Search revenue vaulted by a resplendent 14% year-over-year, ascending to $48.5 billion. This meteoric rise was fuelled by AI-centered search innovations enhancing user immersion. Concurrently, YouTube’s advertising revenue bloomed by 13%, reaping benefits from engrossed viewers and refined monetization endeavors, particularly through YouTube Shorts.

The canopy of Alphabet’s advertising revenue promises further growth, nurtured by imminent revenue triggers like the U.S. elections. Furthermore, the infusion of AI-driven enhancements and fresh advertising features is slated to accelerate the revenue’s growth tempo.

Beyond the advertising vista, Alphabet’s unswerving focus on cloud computing spells a chronicle of triumph. Its Cloud domain breached the $10 billion quarterly revenue mark for the first time in Q2, a testament to its prowess in harnessing AI marvels and ushering generative AI solutions, stoking a ravenous bonfire of demand from enterprise clients.

The robust Alphabet AI infrastructure and generative AI solutions for the Cloud clientele have spawned billions in revenue till date. Alphabet’s fervent investments in AI and strategic alliances foreshadow an even grander tapestry of growth for its Cloud enterprise.

Alphabet, too, sprinkles cash back into the treasure chests of shareholders, having repurchased shares worth $31.7 billion in the initial half of the year. The behemoth retains $74.9 billion in its coffers earmarked for buyback operations, a promise of sustained shareholder enrichment through buybacks.

Analysts, bedecked with optimism, regard Alphabet’s dominion in digital advertising and its AI-fueled cloud ventures as heralding significant long-term prospects. GOOGL basks in the glow of a “Strong Buy” consensus.

The average price target for Alphabet stock stands at $204.71, hinting at a potential upside of approximately 25% from recent levels.

A Final Verdict: Navigating Apple and Alphabet

The oracle of investments whispers tantalizing promises in the ears of discerning investors, torn between the allure of Apple and the enticements of Alphabet. Apple’s dalliance with AI, expanding ecosystem, and devotion to pampering shareholders hint at a solid bet for the future. Alphabet’s steadfast hold on digital advertising, burgeoning AI repertoire, and surging cloud endeavors promise sturdy growth. While both behemoths vie for favor, the scales of Wall Street gently tip towards Alphabet, shimmering with the promise of greater upside potential at current levels. The future beckons, laden with choice, riddled with potential. Investors dwell at the cusp, awaiting the next epoch of Big Tech lore.