Alibaba presently trades at valuation levels akin to steadfast businesses with limited growth horizons, reminiscent of AT&T and Verizon in the telecom sector. With a forward P/E ratio of 9.4x, notably below the industry norm of around 15x and a historical average of 17x, the Chinese behemoth has peeled back the layers of traditionally lofty metrics.

Delving into cash generation metrics, Alibaba boasts a price-to-cash flow ratio of 7.4x, standing approximately 18% below the industry benchmark. These figures paint a picture of a highly de-risked proposition for discerning long-term investors, particularly in light of Alibaba’s resilience amidst a challenging economic landscape in China.

Nevertheless, it is imperative to grasp the underlying rationale for this markdown. The landscape brims with significant perils tied to the investment thesis. Navigating through regulatory and political minefields remains a formidable task, especially grappling with the amplified regulatory oversight by the Chinese authorities concerning tech industry giants, including Alibaba. The label of ‘uninvestable’ has even been bandied about by certain market quarters towards Chinese firms.

Despite the weight of these risks, at existing valuation multiples, investors seem to be handsomely compensated for these ambiguities, particularly those equipped with the lens of longevity.

Analysts’ View on BABA Stock

The trajectory painted by Wall Street for Alibaba appears to be in sync with the current narrative. Over the past three months, the stock has captured 12 Buy ratings and one Hold, culminating in a resounding Strong Buy verdict. Notably, Joyce Ju of Bank of America has significantly upped the ante, elevating the price target from $103 to $106 just ahead of the June quarter announcement. Aggregate prognosis for BABA stock stands at $109.45, hinting at a potential upside of 30.8% from its present trading price.

More insights on BABA analyst ratings here

Crucial Insights

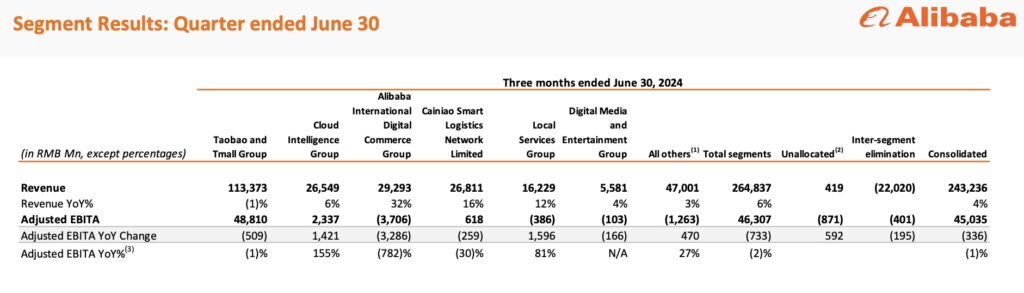

Alibaba’s latest quarterly performance shines a spotlight on its robust show in the international sphere and cloud domain, coupled with GMV expansion in e-commerce, weathering a turbulent economic backdrop. The company’s multifaceted business model, rosy growth outlook, sturdy cash reserves, and appealing valuation render it an enticing proposition for investors oriented towards a long-drawn journey. While the specter of macro risks looms large, the current stock price juxtaposed with optimistic analyst projections hints at a sagacious investment choice.