For most of the AI cycle, investors debated technology: the best model, the best chip, the best architecture. The question for the next phase is different. It’s about who can afford to build and who gets paid while they wait. This week’s TechEdge covers:

|

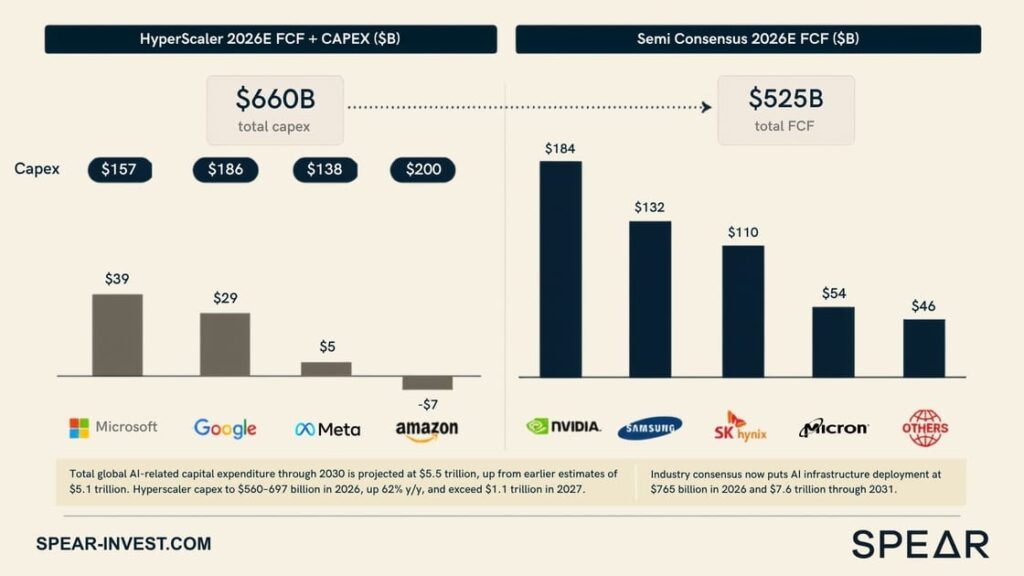

The $5.5T Capex SupercycleThe numbers are getting harder to ignore. Based on our research, total global AI-related capital expenditure through 2030 is now projected at $5.5 trillion, up from earlier estimates of $5.1 trillion, reflecting higher capacity expansion and a shift in how the buildout is being financed. Hyperscaler capex alone is expected to reach $650–$697 billion in 2026, up from $342 billion in 2025 – a 62% year-over-year increase. By 2027, that figure is projected to exceed $1.1 trillion. This is not a forecast driven by optimism. It is driven by commitments already made. Industry consensus now puts AI infrastructure deployment at $765 billion in 2026 alone, and $7.6 trillion through 2031. As of mid-2025, data center construction was running at a $40 billion annualized rate, up 30% year-over-year. 122 gigawatts of new data center capacity is planned for development between 2026 and 2030. The AI trade isn’t over. It’s just entering the phase where the capital requirements get serious. |

|

From Cash Flow to Credit MarketsFor years, hyperscalers funded infrastructure growth largely through operating cash flow. That is changing. As the buildout accelerates, projected capital expenditures are beginning to outpace organic cash generation. Based on our research, debt financing tied to AI and data centers is now estimated to reach $4.1 trillion through 2030. A significant revision upward. Loan-to-cost ratios are averaging above 85%, with some projects exceeding 90%. In 2026 alone, expect roughly $150 billion in U.S. hyperscaler bond issuance, with another $100 billion equivalent issued abroad. High-grade corporate debt is expected to account for more than $2.1 trillion in data center financing over five years. A useful analogy: think less like software, more like commercial real estate. A $15 million-per-megawatt investment can translate into a $25 million increase in market capitalization. Not because the returns are immediate, but because the market assigns outsized value to the optionality of owning critical infrastructure. What’s particularly interesting is that hyperscalers aren’t just building, they’re also helping finance. Long-term capacity commitments from , , and de-risk infrastructure projects, lower financing costs for third-party operators, and accelerate deployment. The largest AI companies aren’t just consumers of infrastructure. They’re becoming part of the capital structure. Access to capital is becoming a competitive moat. Not because it improves margins, but because it determines who gets to build. |

|

ROI by Layer: Who’s Getting Paid and Who’s Still WaitingAt our latest webinar, our Founder and CIO Ivana Delevska was asked the question that’s been nagging at every investor: at what point does the industry see ROI? Her answer was precise. The hyperscalers are seeing ROI today, they just have to front-run the investment. Cloud revenue growth would not be possible without the hardware investment, and that investment is compounding. Earnings are growing. The ROI just isn’t as dramatic as the capital going in, because you have to build before you can monetize. The numbers back this up: operating cash flow across the major hyperscalers is projected to surpass $900 billion by 2027. These are not companies betting on an uncertain future. They are extracting returns at scale while simultaneously funding the next layer. One layer down, NeoClouds and data center operators are locking in long-term contracts that deliver solid, predictable returns. The infrastructure itself is financeable because the credit quality of the offtaker (usually a hyperscaler) is exceptional. The real ROI question belongs to the model layer: , , and their peers. These companies are generating real revenue, but they haven’t yet demonstrated that returns will materialize at a scale that justifies the upfront compute investment. This mirrors the position hyperscalers were in at the beginning of the prior tech cycle. The model companies are today’s early-stage cloud players: burning capital, building infrastructure, and betting that the economics improve as the platform matures. Our research points to a similar conclusion: the AI ecosystem is not fully end-user revenue-backed yet, but it is not entirely speculative either. Expected 2030 revenues make the math look significantly better, but only if AI revenues continue to scale and compute efficiency improves. |

|

The Three Bottlenecks That Cap the Machine

The capital exists. The commitments are signed, but the agentic AI transition is creating a new set of supply constraints that most investors are still underweighting, and they’re not the ones dominating the headlines.

CPUs, memory, and networking are the three hardware categories seeing the most outsized incremental demand as AI shifts from model training to the agentic era. Each bottleneck has its own supply-demand dynamics, cycle position, and investment implications, including a more nuanced take on power and energy than the market currently reflects.

The Bottom Line: What This Means for Investors

The market has spent the week debating whether the AI buildout is a bubble. The Nasdaq has pulled back roughly 3% as investors question whether demand can ever justify the investment. The concern is legitimate. Recent research found that businesses replacing workers with AI agents often fail to generate a return on investment, and surveys show only 16% of Americans believe AI will be a positive societal force.

But the debate misses the structural point. The hyperscalers are not building on hope. They are building because their core businesses: cloud, search, enterprise software, cannot grow at current rates without it. The infrastructure is not discretionary. It is load-bearing.

What the market is actually pricing is timing risk: will the model-layer revenue ramp fast enough to validate the capital already committed?

The answer is that it doesn’t need to validate it immediately. The infrastructure itself has value. Data centers are long-lived assets. HBM supply is constrained. The companies that have locked in those resources today (at yesterday’s prices) have a durable advantage regardless of which AI model wins next year.

The winners aren’t the companies with the best technology. They’re the ones with the cheapest path to funding the next wave.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.