The digital advertising market has been growing at a robust pace. It is expected to generate almost $668 billion in revenue in 2024, up from last year’s size of $600 billion. The good part is that the industry is expected to sustain its impressive growth in the future as well.

According to Oberlo.com, global spending on digital ads is forecast to hit almost $871 billion in 2027. The Trade Desk (NASDAQ: TTD) has been making the most of this fast-growing opportunity, with the company’s growth rate improving this year thanks to the rising demand for its programmatic advertising platform.

Shares of the company have jumped 73% so far this year (as of this writing). However, The Trade Desk’s rally came to a halt following the release of its third-quarter 2024 results on Nov. 7. More specifically, The Trade Desk stock dipped more than 5% following its quarterly report, despite better-than-expected numbers and solid guidance.

Let’s see why that was the case, and check whether investors should consider buying The Trade Desk following its latest dip to capitalize on the digital ad market’s growth.

The Trade Desk’s growth continues to accelerate

The Trade Desk delivered Q3 revenue of $628 million, an increase of 27% from the same period last year, when its top line jumped 25%. The company’s non-GAAP earnings jumped 24% to $0.41 per share, while adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) increased 28% to $257 million. The numbers were well ahead of The Trade Desk’s guidance of $618 million in revenue and $248 million in adjusted EBITDA.

The company attributed its robust growth to the growing demand for connected TV (CTV) advertising, which is its fastest-growing business channel. CEO Jeff Green said on the latest earnings conference call that CTV partners such as Disney, NBCUniversal, Roku, Netflix, and LG “are deepening their relationships with us around the growing CTV opportunity.”

CTV advertising refers to the delivery of ads through TVs connected to the internet. This advertising channel is gaining popularity because of better audience targeting that helps advertisers improve their return on investment. Not surprisingly, spending on CTV advertising is expected to grow from an estimated $29.6 billion this year to $42.5 billion in 2028.

The Trade Desk is well-placed to benefit from this multi-billion-dollar market. The company claims to have access to more than 120 million CTV devices through its programmatic ad platform, which allows advertisers to reach more than 90 million households. So, fast-growing niches such as CTV and the fact that the overall spending on programmatic advertising is forecast to increase at an annual rate of 23% through 2030 should help The Trade Desk maintain its healthy growth rate over the next three years.

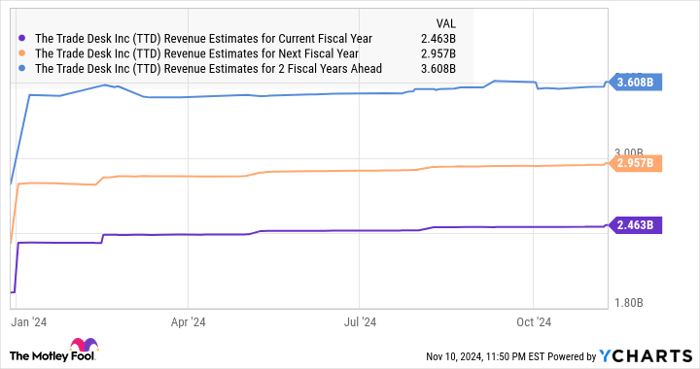

That’s the reason analysts have increased their growth expectations for the next couple of years, expecting the company to clock at least 20% top-line growth in 2025 and 2026.

TTD Revenue Estimates for Current Fiscal Year data by YCharts.

Strong bottom-line growth is in the cards, but there is one problem

The improvement in The Trade Desk’s top-line growth is set to filter down to the bottom line as well, which is evident in the chart below.

TTD EPS Estimates for Current Fiscal Year data by YCharts.

More importantly, the chart indicates that analysts are expecting the company’s earnings growth to accelerate in 2026. Consensus estimates are projecting a 25% annual increase in the company’s earnings for the next five years. It’s expected to finish 2024 with $1.64 per share in adjusted earnings, as seen in the above chart. Assuming its bottom line increases at a 25% annual rate for the next three years, its earnings could jump to $3.20 per share in 2027 (using 2024’s estimated earnings as the base).

If the Trade Desk trades at 30 times earnings at that time, in line with the tech-laden Nasdaq-100 index’s forward earnings multiple (using the index as a proxy for tech stocks), its stock price could hit $96. However, that represents a downside from current levels thanks to the stock’s rich valuation.

The Trade Desk is trading at 202 times trailing earnings and 97 times forward earnings. This expensive valuation is most likely the reason why the stock fell following its latest quarterly report. Again, that’s not surprising. The Trade Desk’s growth, while healthy, is nowhere near the eye-popping growth that some other, attractively valued technology stocks are delivering.

Investors looking to buy more shares of The Trade Desk would do well to adopt a wait-and-watch approach, considering its sky-high valuation, and look for further acceleration in its bottom line so that it can justify its rich multiples.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $23,446!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $42,982!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $428,758!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of November 11, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Netflix, Roku, The Trade Desk, and Walt Disney. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.