Anyone who’s priced a Walt Disney (NYSE: DIS) vacation within the past few days might be suffering from a bit of sticker shock. A trip to any of its theme parks has never been cheap. But following price increases imposed earlier this month, it’ll cost you on the order of 6% more just to set foot in California’s Disneyland; Florida’s Disney World ticket prices are still slated for similar increases next year.

And even beyond entry ticket prices, visitors have seen stunning growth in the cost of in-park amenities. A slice of gourmet chocolate cake can set you back as much as $26, for instance. Disney’s cruises are nickel-and-diming passengers at least a little more now than they were just a few weeks ago as well, with increased corkage fees and higher suggested gratuities.

The decisions raise reasonable concern from shareholders of The Walt Disney Company. Although its parks and cruises obviously offer a premium experience, there are limits to how much visitors are willing — or even able — to pay. Might these price increases ultimately work against the entertainment giant?

They might. But there’s also not much choice in the matter other than to take this risk.

It’s no small risk either. See, Disney’s theme parks, resorts, and related “experiences” are its biggest business in terms of revenue and profits. If it’s wrong about what consumers are ready to shell out, it could hurt … badly.

A business Disney absolutely must get right

In its defense, the Walt Disney company isn’t doing anything most other companies aren’t. Its own operating costs are rising. It must respond, one way or another.

Except, the situation may be even more dire, as well as more complicated than it seems to be on the surface.

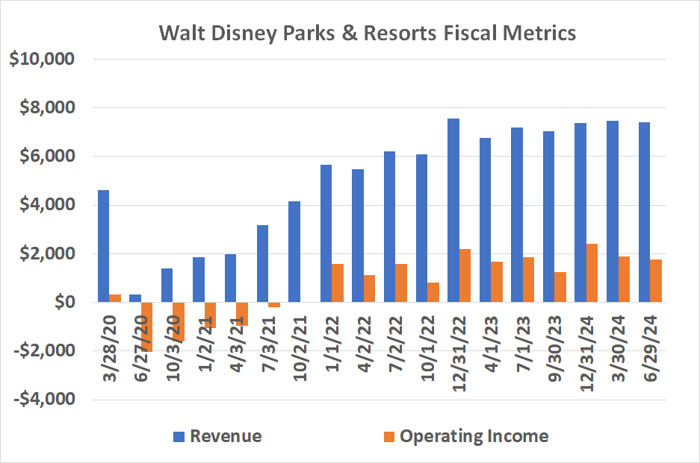

Simply put, Walt Disney’s theme parks, resorts, and other vacation-type businesses aren’t growing. At best they’re stagnant, and from some vantage points they’re even contracting. This is true of their top, as well as their bottom lines.

Data source: The Walt Disney Company. Chart by author. Numbers are in millions.

It’s not terribly surprising. Although most consumers still seemingly have a bit of discretionary income left to spend after paying for their basic goods and services, it’s difficult to deny that budgets are strained right now. An expensive vacation isn’t a particularly prudent choice for most households at this time.

This is an especially pronounced problem for current and prospective Walt Disney investors. See, the entertainment giant’s single biggest profit center is its parks, resorts, and cruise “experiences” arm, accounting for roughly half (or more) of its operating income.

Data source: The Walt Disney Company. Chart by author. Numbers are in millions.

If Disney’s theme park and other experiences business isn’t growing, the company as a whole’s not likely growing either, as measured by earnings, or by revenue.

Sure, overall profits have been improving since late 2022. That’s mostly the result of the recent rebound of its television business and streaming‘s progress toward profitability though. This revival has likely already run most of its course. Future growth is largely going to depend on other business lines.

The headwinds are very real

Recent ticket price increases — along with higher prices for in-park amenities — are of course meant to combat this stagnation. And perhaps they’ll be successful.

Realistically speaking though, the strategy may end up doing more harm than good.

Don’t misunderstand. There are still plenty of people who can afford to take a Walt Disney vacation. There are also still lots of people that arguably can’t afford to do so, yet will shell out the money for an increasingly expensive visit anyway.

By and large, however, the average consumer who’s already balking at Disney’s higher ticket prices will become even more hesitant to visit a park or stay at one of its resorts now. That’s already happening, in fact.

Albeit with less uproar than its most recent round of price increases, Walt Disney upped its theme park prices in October of last year by an even bigger margin than this month’s price hike. While one could sense it in the meantime (and as the charts above illustrate), in August of this year Disney CFO Hugh Johnston conceded it was taking a toll on strained consumers. In his words, “we saw a slight moderation in demand [for experiences]” during the third fiscal quarter ending in June. He added:

We expect to see a flattish revenue number in Q4 coming out of the parks. And as we mentioned in — earlier in the letter, really just a few quarters. So I don’t think I’d refer to it as protracted [weakness], but just a couple of quarters of likely similar results.

There are certainly other red flags indicating the average consumer is still feeling financially pinched, too. Retailer Walmart reported again in August that higher-earning households accounted for the bulk of its fiscal second-quarter sales growth, suggesting that even the affluent are feeling enough financial strain to be bargain-minded. Similarly, snacks and beverage giant PepsiCo lamented in July that its second-quarter volume sales were down 3% primarily because consumers are “price conscious” right now, and searching for value.

If folks are second-guessing the purchase of a soda and a bag of chips, it’s certainly a challenging environment for theme parks — even the premier ones that typically enjoy pricing power.

Management is missing the point, and an opportunity

It’s not a permanent condition. The domestic and global economy will improve at some point in the future, allowing consumers to pay the higher prices now being charged by Disney’s theme parks and related resorts. Ditto for its cruises.

Given how important the company’s experiences business is to its top and bottom lines, however, any measure that makes them less marketable right now arguably creates more problems than benefit for The Walt Disney Company. The time to raise prices is when the economy is firing on all cylinders and more consumers can afford these price hikes. When the economy is in a slump, the right move is figuring out ways to deliver lower-cost value.

In other words, this most recent round of price increases doesn’t improve the bullish argument for Disney stock. It weakens it.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,154!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,777!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $406,992!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 21, 2024

James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Walmart and Walt Disney. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.