Alibaba (NYSE:BABA) stands tall amongst the revered trio of Chinese e-commerce giants, including PDD and JD, trading at a comparable and modest forward PE ratio of around 11x.

Shining Star Amongst the Giants

Alex Yao from J.P. Morgan distinctly favors Alibaba, foreseeing it as a more promising choice over its counterparts. The analyst points to two crucial factors driving this conviction: the anticipation of numerous significant catalysts in the upcoming quarters and the potential for a transformative narrative shift in the domestic e-commerce market, potentially leading to a re-evaluation of its worth.

However, Yao advises investors to adopt a long-term vision. He cautions that Alibaba’s forthcoming September quarter results might bear the brunt of a subdued consumer environment, exerting pressure on both its top and bottom lines.

Yao notes the challenging macro landscape that could impact China’s GMV. The National Bureau of Statistics reported a dip in China’s online physical goods sales growth in August, from +8% year-over-year in July to +4%.

Weathering the Storm

Yao’s projections foresee a modest 6% year-over-year revenue upturn for Alibaba in the coming quarter, falling marginally short of market consensus. Despite predicting a 2% dip in non-GAAP EPS compared to the previous year, Yao’s forecast surpasses Wall Street expectations by 5%.

Despite the near-term challenges, Yao encourages investors to hold firm and anticipate positive catalysts over the next quarters. These may include an uptick in overall consumption fueled by government stimuli, accelerated core-core revenue growth post the implementation of new monetization policies in September, and a surge in active buyer count triggered by the integration of Weixin Payment (WeChat Pay) and growing Southbound capital inflow following the recent inclusion in the HK Stock Connect.

Looking Ahead

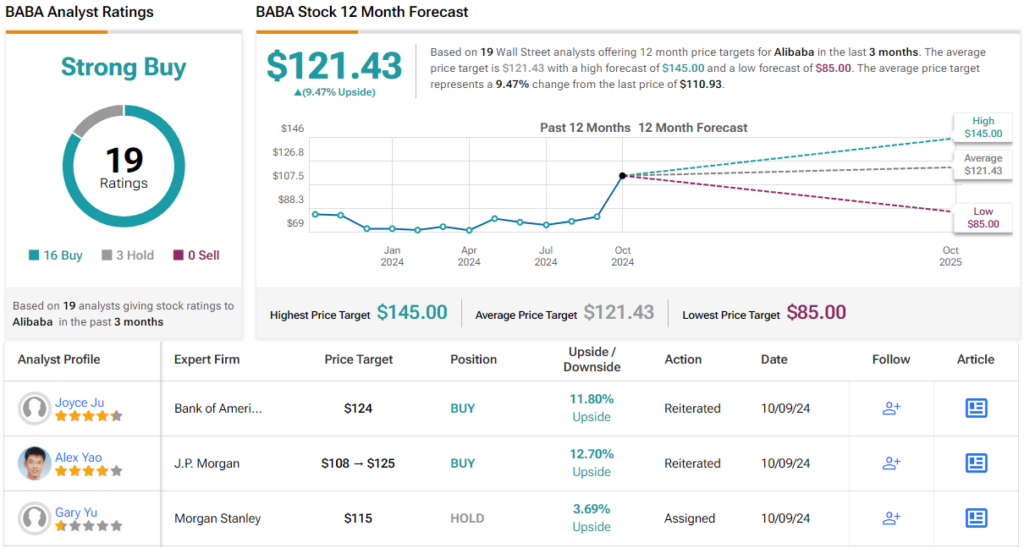

With an Overweight (Buy) rating on BABA shares and a price target of $125 (hinting at approximately a 13% upside from current levels), Yao’s stance reflects confidence in Alibaba’s future prospects. Wall Street analysts echo Yao’s optimism, with 15 Buy ratings overshadowing 3 Holds for a Strong Buy consensus. The average target price of $121.43 forecasts a potential uptick of 9.5%, slightly below Yao’s target.

For investors seeking undervalued stocks, TipRanks’ Best Stocks to Buy tool amalgamates investment insights.

Disclaimer: The opinions expressed embody the featured analyst’s views. This content serves for informational purposes and emphasizes the importance of conducting individual research prior to investment decisions.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.