Netflix NFLX is gearing up to unveil its third-quarter results for 2024 on Oct. 17.

Expectations are high, with a projected 14% increase in revenues for the quarter, translating to a solid 19% growth sans currency fluctuations, powered by pricing modifications in Argentina and currency devaluation against the U.S. dollar.

The company foresees total revenues hitting $9.77 billion, marking 13.9% growth from the previous year. Analysts’ consensus estimate meets Netflix’s outlook, pegging revenues at $9.77 billion.

Netflix has its sights set on earnings of $5.10 per share, reflecting a 36.7% year-over-year growth. While analysts’ estimate aligns closely at $5.07 per share, it remains just shy of the company’s projection.

Explore the latest earnings predictions and surprises on Zacks Earnings Calendar.

The upcoming quarterly results are expected to benefit from Netflix’s diverse content roster, marked by substantial investments in localized and foreign-language content production and distribution.

Image Source: Zacks Investment Research

Historical Earnings Performance

In the previous quarter, Netflix outperformed expectations with an earnings surprise of 3.83%. The company exceeded the Zacks Consensus Estimate in three of the last four quarters, with an average negative surprise of 6.15% in one instance.

Image Source: Zacks Investment Research

Forecasting the Future

Netflix is poised for an earnings beat based on our predictive model, combining a positive Earnings ESP and a favorable Zacks Rank placement of #1 (Strong Buy), 2 (Buy), or 3 (Hold).

With an Earnings ESP of +1.37% and a current Zacks Rank #2, Netflix seems positioned for success. You can view a full list of Zacks #1 Rank stocks here.

Key Drivers for the Upcoming Results

Netflix expects a decline in paid net additions compared to the third quarter of 2023 due to the initial full-quarter impact of paid sharing. The company also projects a flat year-over-year global ARM for the third quarter.

The company’s strategic moves, including the successful introduction of ad-supported low-priced plans, have attracted cost-conscious consumers and created new revenue streams, expanding its subscriber base and revenue channels.

By cracking down on password-sharing through paid sharing alternatives, implemented in over 100 countries and representing a significant portion of Netflix’s revenue, the company aims to convert shared accounts into paid subscriptions, potentially boosting subscribers and revenues.

Furthermore, Netflix’s foray into gaming with titles like Grand Theft Auto: The Trilogy and its focus on enhancing user engagement through additions like Virgin River and Perfect Match indicate a commitment to delivering a holistic entertainment experience.

Despite these positive moves, Netflix faces stiff competition in the streaming arena from rivals like Disney’s Disney+, HBO Max, Peacock, Paramount+, Apple’s Apple TV+, and Amazon’s Prime Video, as well as traditional TV, YouTube, TikTok, and the gaming industry.

Growth Projections for Q3

The consensus anticipates about 4.75 million total streaming net membership additions for the quarter.

Revenue projections for Asia-Pacific, Latin America, EMEA, and the United States and Canada indicate promising growth rates, affirming Netflix’s position in various regions.

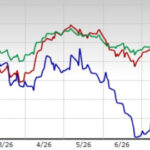

Stock Performance and Market Standing

Netflix shares have surged by 48.5% year-to-date, outperforming peers like Apple, Amazon, and Disney, as well as the broader Consumer Discretionary sector.

Netflix: Leading the Pack

Image Source: Zacks Investment Research

As investors consider their options, the current valuation of Netflix, trading at 7.32X forward 12-month sales, surpasses its five-year median of 6.4X, and notably exceeds the Broadcast Radio and Television industry’s forward earnings multiple of 2.84X. This suggests Netflix’s valuation may be somewhat inflated compared to historical levels and industry norms.

Evaluation of Price-to-Sales (Forward 12 Months)

Image Source: Zacks Investment Research

Exploring Investment Prospects: Delicate Equilibrium between Risk and Reward

Netflix, a colossus in the global streaming realm, boasts unmatched content production capabilities that enforce its position as an enticing investment opportunity. The company’s knack for delivering chart-topping series and films steers robust growth in subscribers and retention. Introducing ad-supported tiers and venturing into gaming signals strategic diversification to broaden revenue sources and extend market outreach. The crackdown on password sharing anticipates unlocking substantial untapped revenue channels. With a robust international presence and a data-centric content creation strategy, Netflix is strategically positioned to seize on the surging global appetite for streaming entertainment. Its commanding brand, innovative technology, and adeptness at adapting to market trends solidify its dominion in the ever-evolving digital media sector.

As the bedrock of global entertainment shifts towards streaming, Netflix is poised to reap significant rewards, granting investors a stake in this high-growth domain. However, cautious investors are advised to remain vigilant, keeping a close eye on content expenses, subscriber growth patterns, and the transforming competitive milieu within the streaming industry.

Parting Reflections

Despite a lofty valuation and intense competition in the streaming landscape, Netflix stands tall as an alluring investment avenue. Its status as a pioneer, expansive global reach, and history of producing culturally impactful content set it a class apart. These facets, coupled with Netflix’s capacity to evolve and innovate, suggest a well-fortified position to uphold market supremacy and leverage the burgeoning digital entertainment sphere, rendering the stock a prudent buy prior to its third-quarter earnings announcement.

7 Primo Stocks for the Next 30 Days

Just unleashed: Connoisseurs sift out 7 top-tier stocks from the existing lineup of 220 Zacks Rank #1 Strong Buys. They tag these stocks as “Most Likely for Early Price Surges.”

Since 1988, this complete slate has outperformed the market by over two-fold, showcasing an average annual gain of +23.7%. Hence, cast your keen eye on these handpicked 7 selections promptly.

To read this article on Zacks.com click here.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.