Traversing the wild tempests of the stock market, it’s evident that technology stocks, especially those in the software realm, are currently soaring to unprecedented heights. The recent surges that catapulted them to these lofty summits have accelerated in mere weeks, making them seemingly unattainable for most investors.

But within this frenzied landscape, not every software stock is basking in the limelight. A select few are on the back foot, despite harboring promising potential for an upward trajectory.

Uncovering Hidden Gems

Seize the moment without hesitation. Dive into the realms of these underdogs before they surge ahead and potentially skyrocket. Here’s a peek at the top three contenders awaiting your keen eye.

Data Delights: Datadog

Enter the domain of Datadog (NASDAQ: DDOG), a titan that might have eluded your radar until now. Despite its market cap of $40 billion, the company stays nestled between the realms of modest and grandeur, offering no consumer-facing allure that might attract the average investor.

However, do not be misled by its unassuming stature. Datadog boasts significant potential, with its stock still trailing 37% behind its late-2021 zenith, languishing in a state of stagnation since the dawn of this year.

In essence, Datadog specializes in observability products tailored for enterprises overseeing vast networks of servers, applications, and cloud-computing platforms. This software enables IT professionals to monitor and enhance the flow of digital data within intricate computer networks. Recognized by technology research entity Gartner as a top performer, particularly in its observability tools, Datadog’s platform plays a pivotal role in bolstering cybersecurity measures, empowering IT teams to swiftly detect and counter cyber threats in real-time.

The company’s robust figures attest to its prowess. Revenue is set to surge by nearly 24% year over year, with an additional 22% growth forecasted for the following year. This surge in top-line growth is anticipated to reinvigorate earnings from this year’s projected $1.65 per share to $1.95 per share next year, with a semblance of similar growth anticipated for 2026 and possibly beyond.

Though the stock comes with a hefty price tag, potentially justifying its struggles in 2022, the company’s promising fiscal trajectory appears to overshadow any valuation concerns.

HubSpot: Your CRM Maverick

Initially, the notion of any customer-relationship management (CRM) software entity competing against the behemoth Salesforce seemed improbable. Salesforce’s dominance appeared insurmountable.

However, the broader the spectrum of features, options, and services a provider offers to cater to a wide array of customers, the more diluted, less enticing, and costlier the platform tends to become. This vacuum paves the way for emerging challengers willing to pioneer innovation, even if the differentiating factor is merely pricing.

Herein lies the essence of CRM trailblazer HubSpot (NYSE: HUBS). Despite emerging on the scene in 2006, trailing Salesforce’s 1999 inception (alongside a myriad of other CRM platforms), HubSpot has swiftly ascended to the runner-up position behind Salesforce, amassing nearly 25% fewer paying customers.

While Salesforce reigns supreme in revenue generation compared to HubSpot, implying a larger corporate clientele or enhanced revenue extraction capabilities, research from Gartner designates Salesforce as the more comprehensive platform. Nonetheless, according to Gartner, HubSpot shines as the world’s preeminent CRM entity in delivering on its promises to customers.

Acknowledging that rankings do not unequivocally translate to investor interests, a stock’s potential fundamentally hinges on the underlying company’s fiscal capacity for growth. HubSpot exudes ample potential, notwithstanding its tepid stock performance since April. This year’s expected near-19% revenue growth aligns with historical and projected trends, with earnings showcasing even more accelerated growth.

Microsoft: Unleashing the Sleeping Giant

Adding industry stalwart Microsoft (NASDAQ: MSFT) to your roster of prospective software stocks poised for exponential growth in the foreseeable future is a prudent maneuver.

An embodiment of ageless brilliance, Microsoft has oddly lagged behind its counterparts since July, failing to ride the surge to record highs that crowned most of its tech compatriots during this period.

The rationale behind this decline is no enigma. While Microsoft initially held a leading edge in the AI revolution’s dawn, its sheen seems to have dulled. Recent downgrades from D.A. Davidson and Oppenheimer emphasize the software magnate’s waning competitive strength in AI. As Davidson analyst Gil Luria succinctly posits, “Competition in the AI domain has finally caught up with Microsoft, diminishing the rationale for its current premium valuation.”

Valid concerns indeed. The low-hanging fruits of the AI realm have been plucked, with key players refining their offerings to near perfection. In the forthcoming landscape, sustaining competitiveness within the AI domain portends substantial challenges.

Yet, amidst these apprehensions, pivotal bullish realities underpin Microsoft. Firstly, AI represents but a fraction of the company’s revenue sources. Secondly, Microsoft wields its formidable brand cachet to efficaciously market products to consumers and corporations alike.

Additionally, the realm of cloud computing stands as a cornerstone of Microsoft’s operations. Research insights from Synergy Research Group highlight that Microsoft’s cloud endeavors outpace all others, including giants like Amazon.

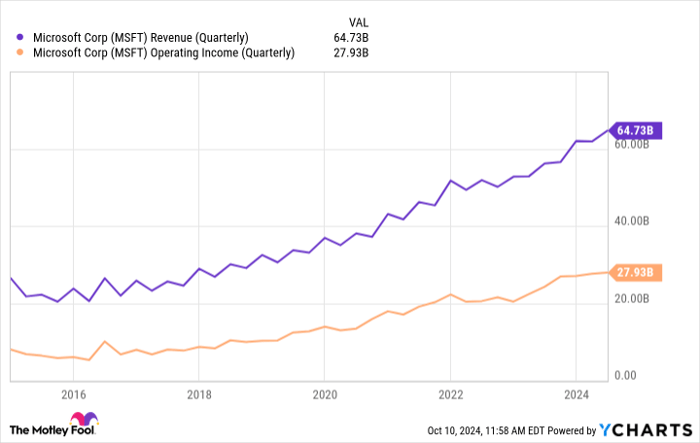

Rest assured, this venerable software luminary’s revenue and earnings exhibit consistent mid-teen growth, poised to persist in this trajectory.

The Unstoppable Force of Microsoft: An Investor’s Insight

A Bright Outlook Amidst Lackluster Performance

A glance at Microsoft’s revenue over the years might paint a picture of stagnation, but analysts remain resolutely optimistic. Despite the stock’s underperformance, more than three-fourths of them maintain a strong buy rating, with a consensus price target that stands nearly 20% above the current value.

Is Microsoft Worth Your Investment?

Before you dive into Microsoft stock, pause for a moment to consider this:

The analysts at Motley Fool Stock Advisor have curated a list of the 10 best stocks primed for substantial growth. Surprisingly, Microsoft did not make the cut. The selected stocks are projected to yield significant returns in the near future.

Cast your mind back to the year Nvidia entered this exclusive list back in 2005. Had you invested $1,000 then based on the recommendation, your initial capital would have ballooned to a jaw-dropping $826,069!

Stock Advisor equips investors with a roadmap to success, offering insights on constructing a diverse portfolio, regular analyst updates, and two fresh stock suggestions every month. Since its inception in 2002, the Stock Advisor service has outperformed the S&P 500 index by more than fourfold.

Curious to know more? Take a peek at the 10 stocks identified by the Stock Advisor team and discover potential avenues for your investment strategy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.