Delving into a stock that has spiraled down by a staggering 70%, one treads cautiously—a seasoned investor knows too well the perils of catching falling knives. The unassuming adage in investing lore preaches that winners tend to keep winning, urging investors to prune the weeds and nourish the flowers in their portfolio. Yet, in the realm of exceptions lies Paycom

and its unparalleled human capital management (HCM) software-as-a-service (SaaS) solutions. Picture this – the stock languishes at 70% below its zenith. Back in 2019, this budding behemoth boasted sales topping $600 million with shares valiantly perched around $170. Today, the stock price echoes its past, but the revenue register sings a different tune – having nearly tripled since its glory days.

This twist of fate, coupled with Paycom’s robust free cash flow resonance, projects a valuation that emerges as a rare gem, an opportunity that surfaces once in a blue moon. The market may still harbor doubts about Paycom’s growth trajectory, but let’s take a closer look at why embracing Paycom for the long haul might just be the stroke of genius investors have been waiting for.

Image source: Getty Images.

Unpacking Paycom’s Growth Deceleration – A Blessing in Disguise?

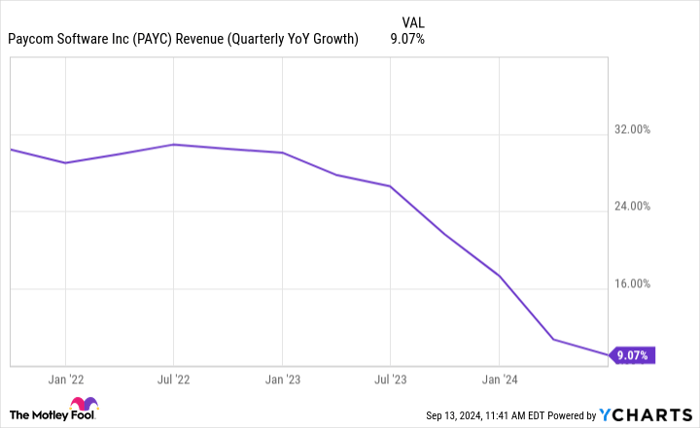

The crux of Paycom’s current plight resides in its dwindling sales growth velocity. A quick glance at the revenue graph unveils the tale of a diminishing growth narrative.

PAYC Revenue (Quarterly YoY Growth) data by YCharts.

While the downturn raises eyebrows, the management’s rationale posits that a substantial chunk of the slump is traceable to the rollout of Beti, its payroll processing marvel, in late 2021. Delegating payroll power to employees, Beti mends common gaffes before payments are processed, curtailing the need for reruns.

This boon to Paycom’s clientele led to one customer slashing their payroll unit by half, thanks to Beti’s clock-saving efficacy. Preceding Beti, Paycom raked sales through payroll reruns triggered by errors. In essence, the recent slowdown stems from one of Paycom’s triumphs – Beti cannibalizing its existing sales roster, thereby stalling growth.

For the steadfast investor who casts their gaze across decades, this trade-off between rejuvenating sales and customer contentment warrants applause. The Net Promoter Score (NPS) of 67 that Paycom flaunts outshines its competitors Paychex, Workday, and ADP, whose respective scores of -14, 31, and -10 pale in comparison. The NPS scale, ranging from -100 to 100, accentuates Paycom’s product popularity – a testament to its customer-centric ethos.

Euphoria strikes for investors as whispers during the second-quarter earnings call hint at a potential turnaround in the sales waning saga. Founder and maestro Chad Richison shares a 24% surge in units sold year-over-year in Q2, hinting at a brighter future than the modest 9% sales uptick implies. Beyond the accolades, Richison’s proclamation of a 40% surge in July begins spells hope for a robust third quarter embarkment. The recent Beti launch in Canada, Mexico, the U.K., and Ireland portends a global upswing, painting a vibrant future on Paycom’s horizon.

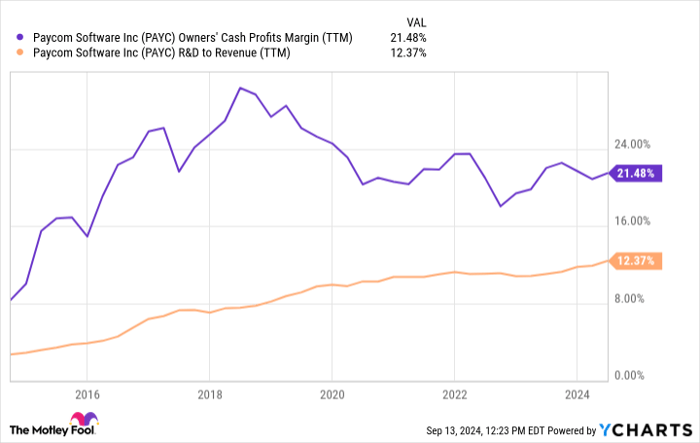

The Growth Conundrum Unpacked: Cash Flow vs. R&D Splurge

Paycom’s captivating allure lies in its unwavering commitment to innovation and customer welfare. As the vortex of research and development (R&D) expenditure widens, Paycom metamorphoses its product spectrum, enriching it with automation prowess. Miraculously, as R&D funds swell, Paycom’s free cash flow (FCF) pedigree retains its resilience.

PAYC Owners’ Cash Profits Margin (TTM) data by YCharts.

Through innovative features such as GONE, Paycom parlays its new leave management tool into generating ample value to offset the R&D financial outlay. GONE’s intrinsic worth resonates profoundly, as Paycom elucidates: “Each manual time-off review or approval can cost a company an average of $30.92, according to a November 2023 Ernst & Young study commissioned by Paycom.”

Remaining a cash cow amid escalated R&D spending elevates Paycom to the vanguard of sustained compounding.

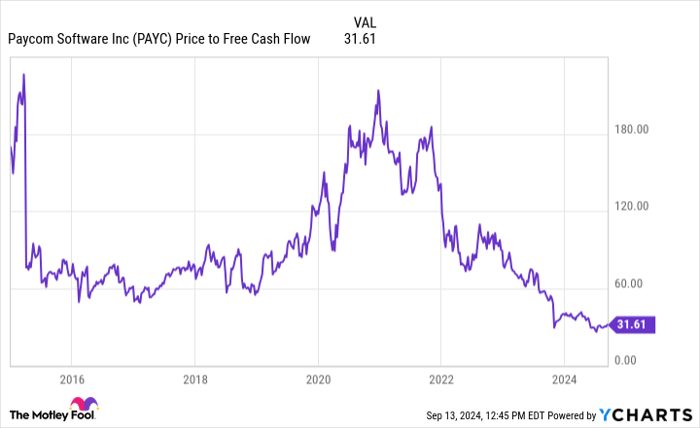

A Potential Decade-Defining Valuation

Beneath Paycom’s prospect-laden tapestry and automation gemstones, the present affords a striking revelation – Paycom twirls at a price-to-free cash flow ratio that whispers once-in-a-decade enchantment.

Enduring silence speaks with a loud whisper.

The Renaissance of Paycom Software on the Horizon

Anchored by a substantial cash balance of $346 million and a debt-free status, Paycom Software’s management has taken bold steps to revitalize its stock with a strategic share buyback program. With a $1.5 billion buyback plan in place, this move could potentially work wonders for the company, especially when considering its $9.7 billion market capitalization.

In addition to the buyback initiative, Paycom also offers a modest 0.9% dividend, albeit without a recent increase. While a higher dividend might entice investors, management’s current focus seems to be on capitalizing on the advantageous pricing for share repurchases.

Looking ahead, there is optimism that Paycom’s sales growth may experience a resurgence in the coming years. Alongside its history of profitable innovation, the company’s current valuation presents an attractive opportunity for long-term investors.

Investment Considerations for Paycom Software

Before deciding to invest in Paycom Software, it’s essential to take note of the following:

The analysts at the renowned Motley Fool Stock Advisor have recently highlighted the 10 best stocks for investors to consider. Interestingly, Paycom Software did not make it to this exclusive list. The selected stocks are expected to yield substantial returns over the upcoming years.

Reflecting on historical successes, such as Nvidia’s inclusion in a similar list on April 15, 2005, we can’t help but wonder about the potential gains. Imagine investing $1,000 based on a recommendation – it could have grown to a staggering $729,857.*

The Stock Advisor service from The Motley Fool has significantly outperformed the S&P 500 since its inception in 2002, amassing returns that are more than four times the S&P 500’s return.*

Explore the top 10 stock picks

*Stock Advisor returns as of September 9, 2024

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.