Interest rates can have a profound effect on companies, influencing both their expenses and revenue streams, particularly within industries heavily reliant on debt financing. For instance, in sectors like airplane leasing, companies often borrow capital to acquire high-cost assets such as aircraft, subsequently entering into long-term leases with airlines at a favorable spread relative to their cost of debt.

One such company feeling the ripples of interest rates is Willis Lease Finance (WLFC), as per analysis from Zacks. WLFC boasts a diverse portfolio comprising 337 engines, 12 aircraft, a marine vessel, and various leased parts and equipment, serving 74 lessees across 42 countries. The firm carries a substantial debt load of $1.95 billion, with $483.8 million maturing in 2025. Should interest rates continue on a downward trend, there may be an opportunity for WLFC to refinance at more attractive rates, consequently slashing interest expenses and potentially boosting its EPS.

In a bid for enhanced sustainability, WLFC recently acquired 15 environmentally friendly engines that operate at a 17% lower fuel consumption rate. This $363.9 million investment is anticipated to significantly enhance lease revenue in the future.

Assessing the company’s valuation, WLFC is currently trading at 1.44 times its trailing 12-month price/book value. This stands in contrast to the Zacks sub-industry at 1.7X, the Zacks sector at 4.01X, and the S&P 500 index at 8.52X. Over the past half-decade, WLFC has seen its stock price fluctuate between 0.25X and 1.44X, with a median of 0.68X.

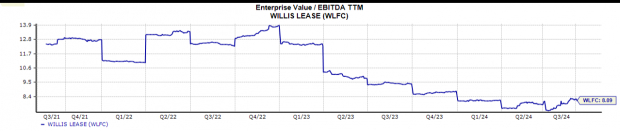

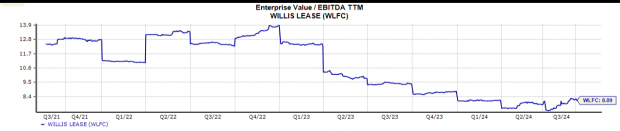

Furthermore, with an EV/EBITDA TTM ratio of 8.2X, WLFC’s valuation appears relatively favorable compared to the Zacks sub-industry (9.62X), the Zacks sector (10.91X), and the S&P 500 index (18.82X). Over the last five years, the stock has swung between 5.35X and 13.88X, with a median of 9.5X.

Image Source: Zacks Investment Research

Conversely, the impact of interest rates on revenue generation is notably significant for industries like real estate that heavily rely on financial transactions. Investors Title Company (ITIC), for instance, specializes in offering title insurance to mitigate losses arising from title defects. This segment comprises approximately 90% of the company’s revenue, with the remainder stemming from tax-deferred real property exchange services.

ITIC has strategically focused on key residential real estate markets in the US, including North Carolina, South Carolina, Texas, Georgia, and a more recent foray into the growing Florida market. By concentrating on the vibrant Sun Belt region, ITIC aims to shield itself from market volatility.

Highlighting the company’s financial robustness, ITIC flaunts a healthy balance sheet featuring $26.7 million in cash reserves and minimal liabilities, positioning itself well for potential growth avenues such as acquisitions.

With its revenue closely tied to mortgage financings and housing prices, ITIC’s fortunes are intertwined with interest rate movements. Higher mortgage rates have been known to deter both potential buyers and sellers from engaging in real estate transactions, underscoring the pivotal role of interest rates in the company’s performance.

A gradual easing of interest rates could potentially unlock this market impasse, leading to an uptick in financing activities that could bode well for ITIC’s prospects. Enthusiastic about this potential, Zacks recently upgraded Investors Title Company (ITIC) to an Outperform rating.

Valuation-wise, ITIC is currently trading at 9.67X its trailing 12-month EV/EBITDA TTM ratio – a favorable metric compared to the Zacks sub-industry (13.08X), the Zacks sector (3.41X), and the S&P 500 index (18.52X). Over the past five years, ITIC’s valuation has fluctuated between 2.29X and 9.74X, with a median of 4.67X.

Image Source: Zacks Investment Research

Identifying the Elite Stock Pick for Potentially Doubling in Value

Per insight from Zacks research, identifying stocks with robust potential amidst interest rate dynamics is critical. One standout contender hails as a company targeting millennial and Gen Z demographics, clocking nearly $1 billion in revenue in the latest quarter alone. A recent market correction renders this moment opportune for savvy investors to hop aboard this promising venture. While not all thrilling rides guarantee a win, this particular stock shows promise to outshine previous Zacks stock picks, akin to the soaring success of Nano-X Imaging that yielded impressive returns of +129.6% in just over nine months.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.