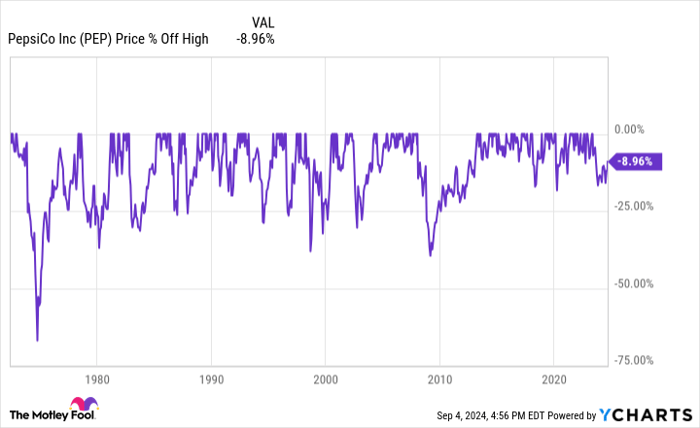

The allure of discounted stock from esteemed companies seldom beckons. A fair price is usually the best one could hope for, which brings us to PepsiCo (NASDAQ: PEP) today. The stock, down about 9% from its 2023 highs, offers a tantalizing proposition for investors eyeing dividend yield and valuation metrics.

A Glimpse into PepsiCo

When you think of PepsiCo, the soda giant Pepsi likely comes to mind – a notable player in the global beverage arena. While soda remains a core business, the company’s beverage arm sprawls across sports drinks, teas, and even protein drinks. But the dominion of this $230 billion market cap colossus doesn’t end there.

Aside from Pepsi, Frito-Lay, under PepsiCo’s wing, reigns in the snacking realm. Known for its potato chips, Frito-Lay’s realm extends beyond to include corn chips, multi-grain chips, popcorn, and pretzels. PepsiCo may trail Coca-Cola in sodas, but in the realm of savory snacks, it secures the top spot.

But that’s not all – PepsiCo boasts a suite of food brands, with Quaker Oats leading the charge. From Quaker Oats to Pasta Roni, these brands adorn its portfolio. Cementing its place in grocery stores, PepsiCo leverages its robust marketing and distribution network to emerge as a pivotal force in the food industry, welcoming new brands into its dynamic ecosystem.

Is PepsiCo a Diamond in the Rough?

With its stock hovering approximately 9% below peak levels, PepsiCo’s current standing flirts with ‘correction territory’. However, a 25% downturn, as evidenced by historical trends, is not unprecedented. Now stands as an opportune moment to consider PepsiCo, with potential to augment holdings should the sell-off deepen.

The current dividend yield sits at 2.9%, nearing the upper echelons of its historical range. With dividends consecutively enhanced for 52 years, PepsiCo proudly wears the crown of a distinguished Dividend King.

Looking at traditional valuation measures, PepsiCo’s price-to-sales, price-to-earnings, price-to-book value, and price-to-cash flow ratios linger below their five-year averages. PepsiCo appears not simply fairly valued, but seemingly a bargain at present.

A Fair Trade for a Premier Player

PepsiCo may not be an irresistible steal today, but its current valuation warrants attention, particularly for a company holding a robust portfolio of consumer staple businesses. Coupled with an appealing dividend yield, notably surpassing the S&P 500’s, the allure of PepsiCo multiplies. A further market slump could well be an open invitation to fortify your position in this well-managed enterprise.

Should You Grasp the Opportunity?

Contemplate this before investing in PepsiCo:

The analyst squad at Motley Fool Stock Advisor has unveiled their selection of the 10 best stocks to buy now, with PepsiCo not making the cut. However, these chosen tenets may usher in substantial returns in the years ahead.

Reflect on the Nvidia inclusion back on April 15, 2005 – an investment of $1,000 then would have burgeoned into $661,779.*

Stock Advisor equips investors with a user-friendly roadmap for success, complete with portfolio construction guidance, analyst updates, and two fresh stock picks monthly. Since 2002, the service has surpassed S&P 500 returns manifold.*

*Stock Advisor returns as of September 3, 2024